Personal Finance

Bad credit score triggers a ‘subprime tax’: Bankrate

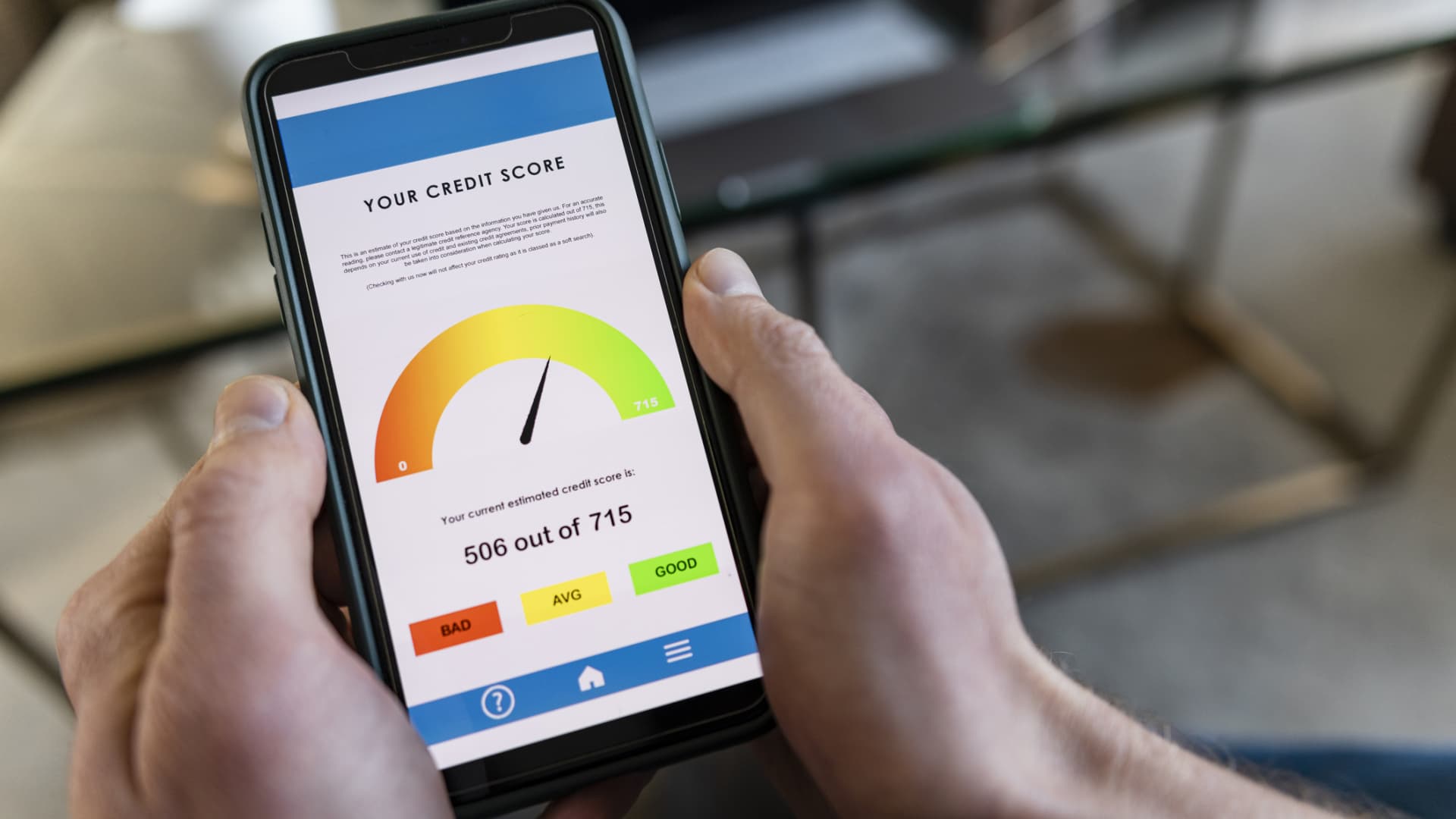

Solstock | E+ | Getty Images

Having a low credit score can come at a significant cost, according to recent data.

Americans with a credit score of 620 or below pay about $3,400 per year for essential financial products in what Bankrate, in a new report, calls a “subprime tax.”

The “subprime tax” comes in the form of higher interest rates on products such as mortgages, credit cards, auto and personal loans, and pricier premiums on auto and home insurance.

Borrowers with a score of 620 pay, on average, $1,330 more annually in mortgage loan interest than those with credit scores of 700, Bankrate found. Compared with that group, subprime borrowers also pay $745 more annually in auto loan interest, $514 more in auto insurance premiums, $398 more in home insurance premiums, $328 more in personal loan interest, and $89 more in credit card interest.

If a borrower doesn’t improve their score, the subprime tax can snowball over the long run, Bankrate found. Over five years, Bankrate’s report said, the subprime tax can cost about $17,016, and over 30 years, the cost is roughly $102,094.

More from Personal Finance:

EV sales soar as Trump axes $7,500 tax credit

Student loan borrowers face ‘cliff effect’ under new payment plan

What private assets in 401(k) plans mean for investors

Bankrate said the insurance premium and debt calculations were based on national average data from Bankrate, Experian and FICO. Bankrate defined a score of 620 and lower as subprime, and a score of 700 and higher as prime.

The subprime tax affects roughly 21% of American adults, Bankrate estimated.

As of April, the average FICO credit score in the U.S. is 715. The score ranges from 300 to 850; the higher the credit score, the better.

The Bankrate report showcases the value of having a good credit score: A good score increases your likelihood of being approved for loans and of receiving better financing terms, experts say.

However, “you don’t need a perfect credit score to get the best loan terms,” said Ted Rossman, a senior industry analyst at Bankrate.

“Generally speaking, lenders stop distinguishing once you hit the mid-700s and above,” he said.

Why a low credit score can cost you

Your credit score is a “prediction of your credit behavior, such as how likely you are to pay a loan back on time, based on information from your credit reports,” according to the Consumer Financial Protection Bureau.

“It’s like a standardized test score,” said Rossman.

If your credit score is low, lenders may think you are more likely to pay late, said John Ulzheimer, a consumer credit expert. To offset that risk, banks and lenders typically charge the borrower higher interest rates.

How to improve your credit

Lenders have different definitions of what makes a good credit score, Ulzheimer said.

Even so, experts say, once your score gets to a certain point, or somewhere in the mid-700s, you are generally in a good place in terms of risk.

“The odds of you going delinquent at some point are so low that the lender is happy with taking the risk with you,” Ulzheimer said.

To improve your credit, first take a look at your credit reports, issued by the three credit reporting bureaus: Experian, TransUnion and Equifax. You can request them for free via annualcreditreport.com. Your credit scores are based on the information in those reports.

Make sure the information in each of the reports is correct, said Matt Schulz, chief credit analyst at LendingTree. If there’s a mistake, which can happen, correcting it can help improve your credit.

Otherwise, the “most actionable way” to improve your score is by working toward paying down any credit card debt, said Ulzheimer.

“If you can pay down or pay off credit card debt, your scores are going to improve,” he said.

Reducing your debt can improve your credit utilization ratio, or how much you owe relative to how much credit you have available to you.

This factor makes up 30% of your score, according to FICO. Experts typically advise keeping your credit utilization under 30%, but a 2024 LendingTree study found that consumers with the best scores had utilization ratios of around 10%.

Another easy way to boost your score is by making on-time payments. Payment history makes up 35% of your score, according to FICO.

As you increase your credit score, look for ways to benefit. For example, ask your credit card issuers if you can qualify for a lower rate, and see if your insurers will reassess your policy premiums. Gauge whether it’s worth refinancing any current loans.

Personal Finance

Algorithmic Wealth Management: Balancing Automated Financial Planning with Human Oversight

Personal Finance

High-Yield Optimization: Structuring Personal Cash Reserves in a Sustained Rate Environment

UK Has a New Prime Minister Without a General Election

Adaptive Governance in Volatile Markets

Navigating Sovereign Data Residency Mandates in the Age of AI

Armanino adds Strategic Accounting Outsourced Solutions

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

Tax Strategy: Employee Retention Credit update

-

Economics4 days ago

Economics4 days agoGlobal Trade Realignment and Supply Chains in 2026

-

Economics5 days ago

Economics5 days agoThe Warsh Shift: How the New Fed Chair Is Balancing War Drags and Tech Winds

-

Economics4 days ago

Economics4 days agoLabor Market Calibration: Analyzing the Shift Toward Skill-Based Allocation in 2026

-

Leaders6 days ago

Leaders6 days agoBerkshire Hathaway Chairman Reshapes His Long-Term Philanthropic Strategy

-

Finance6 days ago

Finance6 days agoSouth Korea Raises Interest Rates to 2.75% for the First Time in More Than Three Years

-

Finance4 days ago

Finance4 days agoTokenized Real-World Assets: Institutional Ledger Adoption Achieves Scale in July 2026

-

Economics6 days ago

Economics6 days agoGlobal Stock Market Weekly Recap: Tech Sell-Off Sparks International Rout

-

Accounting4 days ago

Accounting4 days agoStandardizing Global ESG Reporting: Key Compliance Imperatives for Mid-Year 2026