Accounting

Orgs going full steam ahead on AI, regardless of economy

Companies seem to be going all in on AI, not only planning huge investments in it this year but making these investments central to their growth strategy, even amid other economic headwinds.

Processing Content

A number of studies and surveys has found that businesses are planning major spending on AI technology this year. For instance,

Meanwhile, finance and procurement solutions platform Coupa found in

And while economic headwinds are a reality throughout the business world, organizations do not appear to be letting that stop them. The KPMG survey said that 79% said AI will continue to be a top investment priority even if a recession occurs in the next 12 months. This is despite mixed feelings about the future of the economy, as cited by the GT survey: Optimism dropped from 52% to 46%, but pessimism also fell from 31% to 25%; overall, more have a neutral view of the economy, going from 17% to 29%.

This planned spending, however, might be because of, not despite, these perceived headwinds, as businesses seem to be placing a lot of hope in AI to carry them through these troubling economic times. The Coupa survey, for instance, asked leaders about their top profitability strategies going forward, and a clear majority, 60%, cited increasing their investment in AI. Meanwhile, asking about their top growth strategies, the most common answer, at 58%, was once again to increase AI technology investments. And finally, 85% said AI was central to their financial strategy this year, and a whopping 100% are planning AI investments over the next six to 12 months.

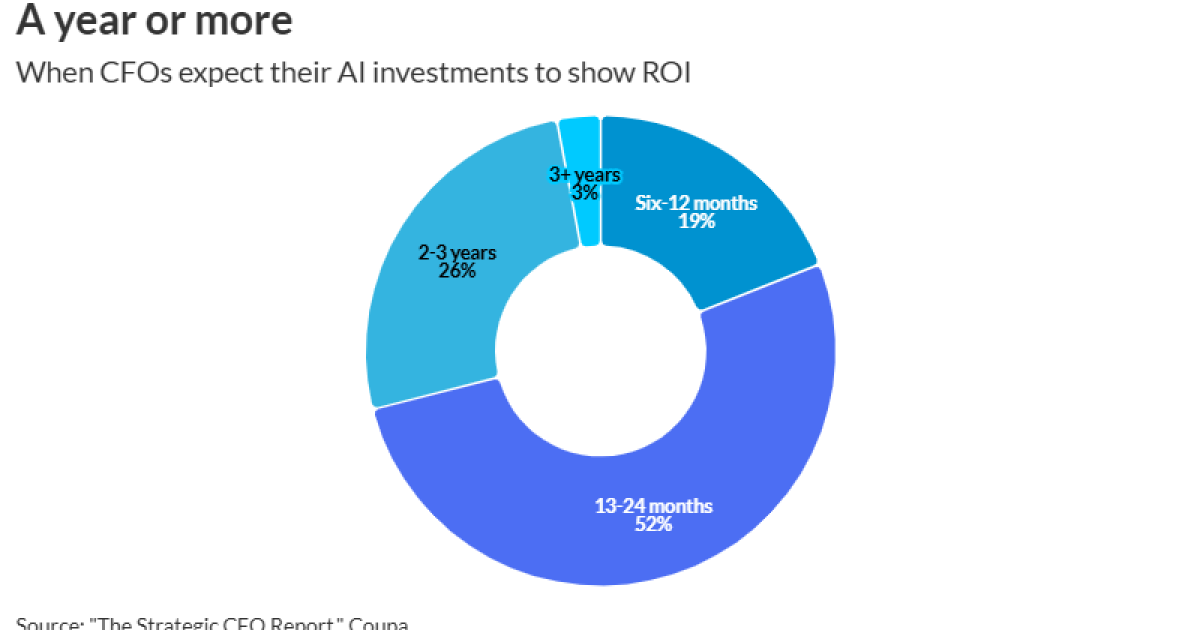

Other surveys also show confidence that organizations’ AI bets will pay off. The Coupa survey said 19% expect return on investment within six to 12 months, 52% expect it within 13-24 months, and 26% think it will take two to three years. Only 3% thought it would take longer than that. They might be getting these expectations from their peers: The KPMG survey found 62% of finance leaders saying they have either achieved measurable ROI or expect to sometime in the next year, up from 59% the last time they asked this question.

In general, leaders appear to be counting on gains from AI, according to the GT survey. It noted that while CFOs are investing in technology at record levels, they’re not cutting elsewhere to fund it. The survey revealed that 72% expect their net profit to grow over this year, up from 68% last quarter, which the report said could indicate faith that AI will expand revenue and increase productivity.

Organizations also might be planning spending increases because their technology costs have gone up. A report from Big Four firm Deloitte

Regardless of motivation, though, companies also seem well aware of the challenges of AI implementation. The KPMG survey showed that leaders did a lot of learning over last year about them: those citing difficulty scaling use cases as an ROI barrier went from 33% in Q1 last year to 65% now; similarly, those citing skills gaps went from 25% to 62%, those naming difficulty quantifying indirect or long-term benefits went from 34% to 59%. The only thing that went down were those talking about risk considerations like data privacy and cybersecurity, going from 74% to 58%. Yet, at the same time the KPMG survey found they’re eager to address these issues, as 91% of leaders named data security, privacy and risk concerns as the top factor influencing AI strategy for the next six months.

Similarly, the Deloitte report noted that, over and over, people have named three fundamental infrastructure obstacles that prevent organizations from fully realizing the potential of agentic AI: legacy system integration, data architecture constraints and governance/control frameworks. Deloitte said that, right now, most enterprises are not set up to take advantage of the opportunities agents represent.

This is quite similar to what leaders cited in the Coupa survey. When asked about the largest constraints to integrating AI into daily workflows, 72% said data quality and readiness, 65% cited integration complexity, and 70% said data security and compliance. However, Coupa also noted another issue is that organizations may have trouble actually determining whether their AI investments were worth it in the first place, as 76% said that difficulty actually quantifying ROI was hindering further implementation.

However, Twisha Sharma, senior research principal for Gartner Finance practice, said companies may not be realizing their goals because of the way they’re viewing AI. Many talk about AI investments as a big broad category, but Sharma, in a

“AI does not follow one cost curve, and it does not produce one uniform type of value,” said Sharma. “CFOs need to stop looking for a single ROI formula and instead build a balanced portfolio that includes productivity use cases, targeted process improvements, and selective transformational bets.”

Sharma warned that CFOs risk undervaluing AI if they focus too narrowly on immediate financial returns, such as revenue growth, cost reduction or cash flow improvement alone. She said many AI initiatives create important nonfinancial value first — including better decision support, stronger business agility, wider organizational reach, innovation capacity and even a shift in finance’s role within the enterprise — long before those benefits are fully visible in the P&L.

“The value of AI is not always captured first in traditional financial metrics. In many cases, it appears earlier in better decisions, faster adaptation and stronger organizational capability. CFOs need to account for that if they want a complete picture of what AI is really delivering,” said Sharma.

UK Has a New Prime Minister Without a General Election

Adaptive Governance in Volatile Markets

Navigating Sovereign Data Residency Mandates in the Age of AI

Armanino adds Strategic Accounting Outsourced Solutions

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

Tax Strategy: Employee Retention Credit update

-

Economics4 days ago

Economics4 days agoGlobal Trade Realignment and Supply Chains in 2026

-

Economics5 days ago

Economics5 days agoThe Warsh Shift: How the New Fed Chair Is Balancing War Drags and Tech Winds

-

Economics4 days ago

Economics4 days agoLabor Market Calibration: Analyzing the Shift Toward Skill-Based Allocation in 2026

-

Finance6 days ago

Finance6 days agoSouth Korea Raises Interest Rates to 2.75% for the First Time in More Than Three Years

-

Leaders6 days ago

Leaders6 days agoBerkshire Hathaway Chairman Reshapes His Long-Term Philanthropic Strategy

-

Finance4 days ago

Finance4 days agoTokenized Real-World Assets: Institutional Ledger Adoption Achieves Scale in July 2026

-

Economics6 days ago

Economics6 days agoGlobal Stock Market Weekly Recap: Tech Sell-Off Sparks International Rout

-

Accounting4 days ago

Accounting4 days agoStandardizing Global ESG Reporting: Key Compliance Imperatives for Mid-Year 2026