Personal Finance

The best way to get started

When it comes to teens and money, there is often a disconnect.

Overall, teenagers are taking a greater interest in their long-term financial health — although far fewer understand basic retirement planning.

A majority, or 83%, of 13- to 18-year-olds, said they had already thought about their retirement, according to the results of a survey from Junior Achievement and MissionSquare.

But most teens mistakenly believed saving money in a bank account was the best long-term strategy. Only 45% said investing in stocks and bonds with the help of a financial advisor, which would offer a greater long-term return, was the preferred way to go.

“This research shows retirement is more top-of-mind for teens than one might think,” said Jack Kosakowski, Junior Achievement’s president and CEO. “While young people have given retirement planning some thought, it’s apparent they still need information on the best way to go about it.”

‘The greatest money-making asset you can possess’

Although retirement can seem very far away, particularly for those just starting out, teens have a unique opportunity others do not, according to Ed Slott, a certified public accountant and founder of Ed Slott and Co.

“The greatest money-making asset you can possess is time,” he said. “Someone who starts at 15 has a huge advantage even over someone who starts at 25.”

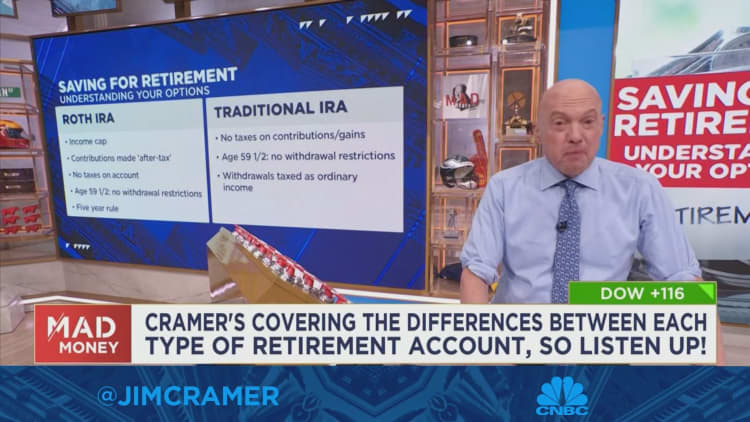

Slott recommends opening a Roth individual retirement account to get a head start.

Contributions to a Roth IRA are taxed up front and earnings grow tax-free. In retirement, withdrawals are completely free of tax and penalties (as long as the account has been open for at least five years).

Since there are no age restrictions, anyone with earned income — say, from a summer job — can contribute.

Even if a teen only puts some money away, parents can add funds on their child’s behalf, as long as the combined amount doesn’t exceed the teenager’s earned income for the year. Once contributed, the money inside a Roth IRA account can be invested appropriately to suit any type of long-term goal.

In Christopher Jackson’s 12th grade personal finance class, students open Roth IRAs with an initial grant of $100 from the community, which they then learn how to maintain on their own. Jackson, who teaches at DaVinci Communications High School in Southern California, tells his students that “this is going to be the most important class they are going to take in their life.”

“My No. 1 goal is to affect their children’s children,” he recently told CNBC.

How Roth IRAs help you start saving

While there is a maximum IRA contribution limit of $7,000 for 2024, it’s less about how much you save and more about the act of saving, Slott said. “It doesn’t have to be a lot. Time is the key asset.”

Meanwhile, both the investment and all the interest, dividends and growth on these assets will accumulate tax-free over the years.

If there are more immediate needs before hitting retirement age, account holders can withdraw their contributions at any time without taxes or penalties if, for instance, they need the money for college or a down payment on a house down the road, according to Slott.

However, Slott advises young adults to view tapping these funds as a last resort.

“Roth money is the last money you should touch because that money is growing the fastest and it will never be eroded by current or future taxes,” he said.

Personal Finance

Algorithmic Wealth Management: Balancing Automated Financial Planning with Human Oversight

Personal Finance

High-Yield Optimization: Structuring Personal Cash Reserves in a Sustained Rate Environment

UK Has a New Prime Minister Without a General Election

Adaptive Governance in Volatile Markets

Navigating Sovereign Data Residency Mandates in the Age of AI

Armanino adds Strategic Accounting Outsourced Solutions

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

Tax Strategy: Employee Retention Credit update

-

Economics5 days ago

Economics5 days agoGlobal Trade Realignment and Supply Chains in 2026

-

Economics6 days ago

Economics6 days agoThe Warsh Shift: How the New Fed Chair Is Balancing War Drags and Tech Winds

-

Economics5 days ago

Economics5 days agoLabor Market Calibration: Analyzing the Shift Toward Skill-Based Allocation in 2026

-

Finance7 days ago

Finance7 days agoSouth Korea Raises Interest Rates to 2.75% for the First Time in More Than Three Years

-

Leaders7 days ago

Leaders7 days agoBerkshire Hathaway Chairman Reshapes His Long-Term Philanthropic Strategy

-

Finance5 days ago

Finance5 days agoTokenized Real-World Assets: Institutional Ledger Adoption Achieves Scale in July 2026

-

Economics7 days ago

Economics7 days agoGlobal Stock Market Weekly Recap: Tech Sell-Off Sparks International Rout

-

Technology5 days ago

Technology5 days agoQuantum Resistance Transition: Securing Enterprise Architecture Against Post-Quantum Threats