Economics

3 Facts That Help Explain a Confusing Economic Moment

The path to a “soft landing” doesn’t seem as smooth as it did four months ago. But the expectations of a year ago have been surpassed.

The economic news of the past two weeks has been enough to leave even seasoned observers feeling whipsawed. The unemployment rate fell. Inflation rose. The stock market plunged, then rebounded, then dropped again.

Take a step back, however, and the picture comes into sharper focus.

Compared with the outlook in December, when the economy seemed to be on a glide path to a surprisingly smooth “soft landing,” the recent news has been disappointing. Inflation has proved more stubborn than hoped. Interest rates are likely to stay at their current level, the highest in decades, at least into the summer, if not into next year.

Shift the comparison point back just a bit, however, to the beginning of last year, and the story changes. Back then, forecasters were widely predicting a recession, convinced that the Federal Reserve’s efforts to control inflation would inevitably result in job losses, bankruptcies and foreclosures. And yet inflation, even accounting for its recent hiccups, has cooled significantly, while the rest of the economy has so far escaped significant damage.

“It seems churlish to complain about where we are right now,” said Wendy Edelberg, director of the Hamilton Project, an economic policy arm of the Brookings Institution. “This has been a really remarkably painless slowdown given what we all worried about.”

The monthly gyrations in consumer prices, job growth and other indicators matter intensely to investors, for whom every hundredth of a percentage point in Treasury yields can affect billions of dollars in trades.

But for pretty much everyone else, what matters is the somewhat longer run. And from that perspective, the economic outlook has shifted in some subtle but important ways.

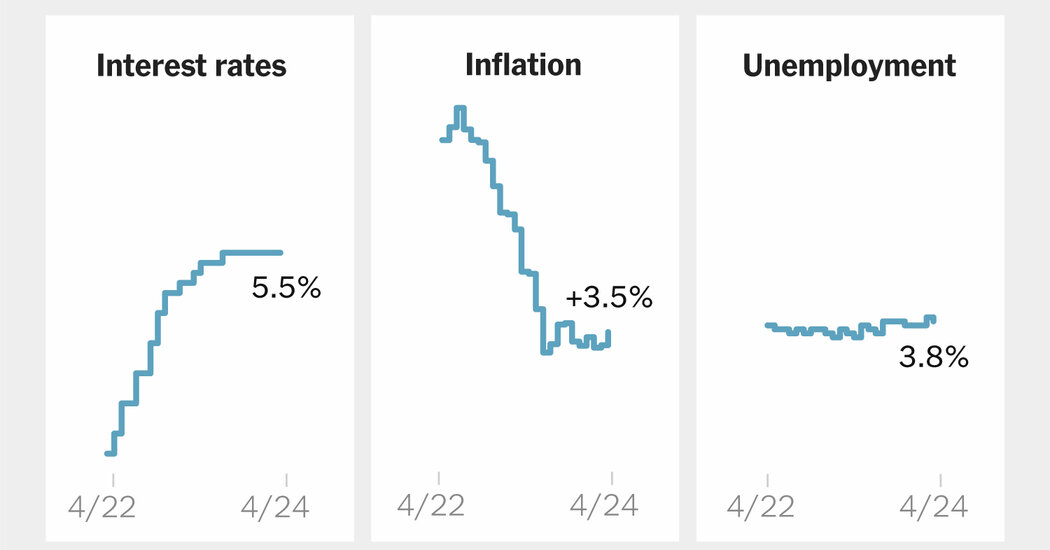

Inflation is stubborn, not surging.

Inflation, as measured by the 12-month change in the Consumer Price Index, peaked at just over 9 percent in the summer of 2022. The rate then fell sharply for a year, before stalling out at about 3.5 percent in recent months. An alternative measure that is preferred by the Fed shows lower inflation — 2.5 percent in the latest data, from February — but a similar overall trend.

In other words: Progress has slowed, but it hasn’t reversed.

On a monthly basis, inflation has picked up a bit since the end of last year. And prices continue to rise quickly in specific categories and for specific consumers. Car owners, for example, are being hit by a triple whammy of higher gas prices, higher repair costs and, most notably, higher insurance rates, which are up 22 percent over the past year.

But in many other areas, inflation continues to recede. Grocery prices have been flat for two months, and are up just 1.2 percent over the past year. Prices for furniture, household appliances and many other durable goods have been falling. Rent increases have moderated or even reversed in many markets, although that has been slow to show up in official inflation data.

“Inflation is still too high, but inflation is much less broad than it was in 2022,” said Ernie Tedeschi, a research scholar at Yale Law School who recently left a post in the Biden administration.

The rest of the economy is doing well.

The recent leveling-off in inflation would be a big concern if it were accompanied by rising unemployment or other signs of economic trouble. That would put policymakers in a bind: Try to prop up the recovery and they could risk adding more fuel to the inflationary fire; keep trying to tamp down inflation and they could tip the economy into a recession.

But that isn’t what is happening. Outside of inflation, most of the recent economic news has been reassuring, if not outright rosy.

The labor market continues to smash expectations. Employers added more than 300,000 jobs in March, and have added nearly three million in the past year. The unemployment rate has been below 4 percent for more than two years, the longest such stretch since the 1960s, and layoffs, despite cuts at a few high-profile companies, remain historically low.

Wages are still rising — no longer at the breakneck pace of earlier in the recovery, but at a rate that is closer to what economists consider sustainable and, crucially, that is faster than inflation.

Rising earnings have allowed Americans to keep spending even as the savings they built up during the pandemic have dwindled. Restaurants and hotels are still full. Retailers are coming off a record-setting holiday season, and many are forecasting growth this year as well. Consumer spending helped fuel an acceleration in overall economic growth in the second half of last year and appears to have continued to grow in the first quarter of 2024, albeit more slowly.

At the same time, sectors of the economy that struggled last year are showing signs of a rebound. Single-family home construction has picked up in recent months. Manufacturers are reporting more new orders, and factory construction has soared, partly because of federal investments in the semiconductor industry.

Interest rates are going to stay high for a while.

So inflation is too high, unemployment is low and growth is solid. With that set of ingredients, the standard policymaking cookbook offers up a simple recipe: high interest rates.

Sure enough, Fed officials have signaled that interest rate cuts, which investors once expected early this year, are now likely to wait at least until the summer. Michelle Bowman, a Fed governor, has even suggested that the central bank’s next move could be to raise rates, not cut them.

Investors’ expectation of lower rates was a big factor in the run-up in stock prices in late 2023 and early 2024. That rally has lost steam as the outlook for rate cuts has grown murkier, and further delays could spell trouble for stock investors. Major stock indexes fell sharply on Wednesday after the unexpectedly hot Consumer Price Index report; the S&P 500 ended the week down 1.6 percent, its worst week of the year.

Borrowers, meanwhile, will have to wait for any relief from high rates. Mortgage rates fell late last year in anticipation of rate cuts but have since crept back up, exacerbating the existing crisis in housing affordability. Interest rates on credit card and auto loans are at the highest levels in decades, which is particularly hard on lower-income Americans, who are more likely to rely on such loans.

There are signs that higher borrowing costs are beginning to take a toll: Delinquency rates have risen, particularly for younger borrowers.

“There are reasons to be worried,” said Karen Dynan, a Harvard economist who was a Treasury official under President Barack Obama. “We can see that there are parts of the population that are for one reason or another coming under strain.”

In the aggregate, however, the economy has withstood the harsh medicine of higher rates. Consumer bankruptcies and foreclosures haven’t soared. Nor have business failures. The financial system hasn’t buckled as some people feared.

“What should keep us up at night is if we see the economy slowing but the inflation numbers not slowing,” Ms. Edelberg of the Hamilton Project said. So far, though, that isn’t what has happened. “We still just have really strong demand, and we just need monetary policy to stay tighter for longer.”

Economics

Consumer sentiment reading rebounds to much higher level than expected as people get over tariff shock

China retail sales, industrial output, fixed asset investment in May

Why aren’t Chinese consumers spending enough

New ETF gives investor chance to act like a private equity giant

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Economics1 week ago

Economics1 week agoJobs report May 2025:

-

Economics1 week ago

Economics1 week agoDonald Trump has many ways to hurt Elon Musk

-

Economics1 week ago

Economics1 week agoSending the National Guard to LA is not about stopping rioting

-

Finance1 week ago

Finance1 week agoStocks making the biggest moves midday: WOOF, TSLA, CRCL, LULU

-

Blog Post1 week ago

Blog Post1 week agoMastering Bookkeeping Tasks During Peak Business Seasons

-

Economics1 week ago

Donald Trump has many ways to hurt Elon Musk

-

Personal Finance1 week ago

Personal Finance1 week agoWhat Pell Grant changes in Trump budget, House tax bill mean for students

-

Economics1 week ago

Economics1 week agoRussia cuts sky-high interest rates for the first time since 2022