Accounting

Trump signs executive action to create sovereign wealth fund

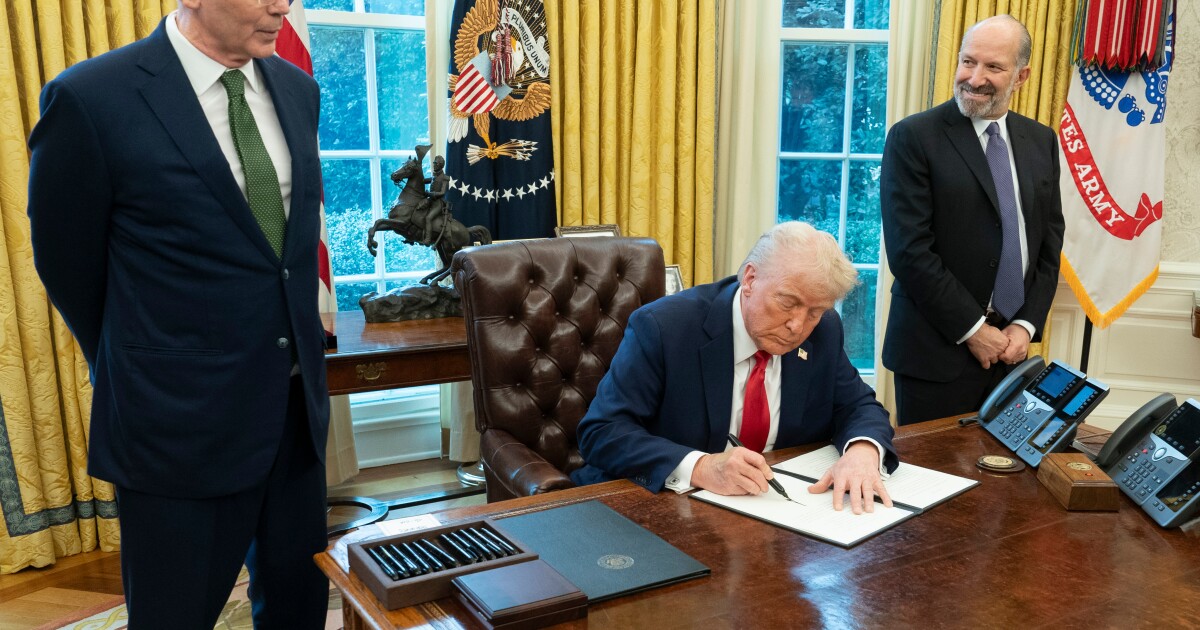

President Donald Trump signed an executive action he said would direct officials to create a sovereign wealth fund for the U.S., following through on an idea he floated during the presidential campaign.

“We have tremendous potential,” Trump told reporters in the Oval Office on Monday as he announced the move. The president said the action would charge Treasury Secretary Scott Bessent and Howard Lutnick, the nominee for Commerce secretary, with spearheading the effort.

Bessent, who joined Trump at the Oval Office, said the fund would be created in the next 12 months, calling it an issue “of great strategic importance.”

Trump suggested the fund could be used to facilitate the sale of TikTok, which is currently operating in the U.S. thanks to an extension he signed prolonging the deadline for a forced sale or shutdown.

Lutnick said the U.S. government could leverage its size and scale given the business it does with companies, citing drug makers as an example.

“If we are going to buy two billion COVID vaccines, maybe we should have some warrants and some equity in these companies,” he said.ot supported.

The action calls for officials to submit a plan to Trump within 90 days, including recommendations for funding, investment strategies, fund structure and governance. And it asks for an evaluation of the legal considerations for setting up and running a fund, including whether legislation is required.

Trump advisors have previously discussed plans to use the U.S. International Development Finance Corp. to partner with major institutional players to leverage U.S. economic powers.

Among those driving the conversation about using the DFC both more like a sovereign fund and as a tool to radically change America’s approach to foreign aid are Elon Musk and Stephen Feinberg, the billionaire co-founder of Cerberus Capital Management, who Trump has nominated as deputy defense secretary, according to people familiar who were close to the president’s transition team before taking office.

Trump on Friday said he was nominating Ben Black — the son of Apollo Global Management co-founder Leon Black — to head the DFC.

Trump floated the idea of a sovereign wealth fund during an address at the Economic Club of New York during the campaign in September, where he proposed funneling money from tariffs into a wealth fund that could invest in manufacturing hubs, defense and medical research.

“We will create America’s own sovereign wealth fund to invest in great national endeavors for the benefit of all the American people,” Trump said at the time and suggested that the Wall Street and corporate leaders at that event could have a role to play, helping to “advise and recommend investments.”

Sovereign wealth funds generally exist in countries that either have large foreign exchange reserves, such as China, or revenue from the sale of oil or other commodities, like Norway and Saudi Arabia. The money is then invested in everything from stocks and bonds to infrastructure and technology. Among the

“We’re going to monetize the asset side of the U.S. balance sheet for the American people,” Bessent said. “It’ll be a combination of liquid assets, assets we have in this country as we work to bring them out for the American people.”

Former President Joe Biden had also been crafting a proposal to create a fund that would invest in national security interests, including technology, energy and critical links in the supply chain.

There are 20 states that have sovereign wealth funds, generally funded by commodities or land, that might serve as models. The largest is the Alaska Permanent Fund, started in 1976, which currently manages about $82 billion. A more recent example is North Dakota’s $11.5 billion Legacy Fund, created in 2010.

North Dakota deposits 30% of its oil and gas tax revenue into the fund monthly. During any two-year budget cycle, the state can access 5% of the money to help finance projects and provide tax relief.

The fund helped make it possible for North Dakota to announce a plan late last month to phase out property taxes for homeowners over the next decade.

Trump on Monday delayed plans to hit Mexico and Canada with tariffs, citing measures the two countries were taking to crack down on the flow of fentanyl and illegal migration.

Leading Teams Through Energy and Macro Volatility

Managing Mortgage Rates and High Home Prices for home buyers

Alphabet Inc. Faces Investor Scrutiny After Reporting Negative Free Cash Flow for the first time

Armanino adds Strategic Accounting Outsourced Solutions

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

Tax Strategy: Employee Retention Credit update

-

Economics1 week ago

Economics1 week agoThe Warsh Shift: How the New Fed Chair Is Balancing War Drags and Tech Winds

-

Economics1 week ago

Economics1 week agoGlobal Trade Realignment and Supply Chains in 2026

-

Economics1 week ago

Economics1 week agoLabor Market Calibration: Analyzing the Shift Toward Skill-Based Allocation in 2026

-

Finance1 week ago

Finance1 week agoSouth Korea Raises Interest Rates to 2.75% for the First Time in More Than Three Years

-

Finance1 week ago

Finance1 week agoTokenized Real-World Assets: Institutional Ledger Adoption Achieves Scale in July 2026

-

Leaders1 week ago

Leaders1 week agoBerkshire Hathaway Chairman Reshapes His Long-Term Philanthropic Strategy

-

Economics7 days ago

Economics7 days agoUK Has a New Prime Minister Without a General Election

-

Economics1 week ago

Economics1 week agoGlobal Stock Market Weekly Recap: Tech Sell-Off Sparks International Rout