Personal Finance

Students going into skilled trades are finding secure jobs, good pay

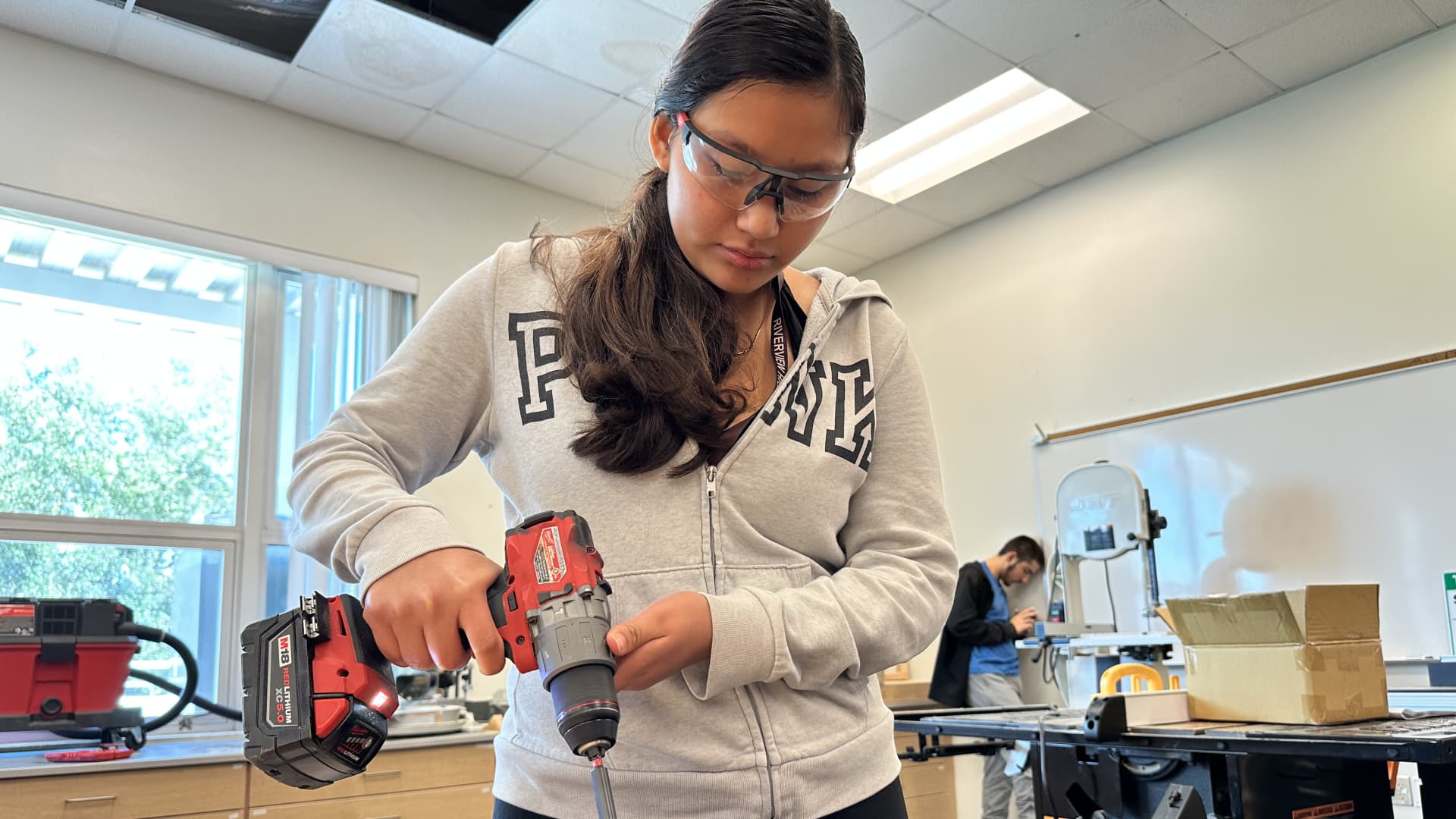

Angela Ramirez-Riojas, 18, is enrolled in Riverview High School’s construction academy.

Courtesy: Riverview High School

For Angela Ramirez-Riojas, 18, going to college was always plan B.

Her grandfather works in construction, and that motivated Ramirez-Riojas to follow in his footsteps.

“I’ve gone with him to work,” she said. “He frames houses and I really enjoyed being there with him because I look up to him. He’s very smart and knows a lot about working with his hands.”

Ramirez-Riojas, who is a senior at Riverview High School in Riverview, Florida, enrolled in her school’s recently opened vocational program in construction. The job training was particularly appealing, she said.

“I want something quick to help me move along,” she said.

Still, higher education isn’t completely off the table, she said. “College is a second option for me.”

Interest in the skilled trades is rising among teens

Three years ago, Riverview High School opened its construction academy to help put students like Ramirez-Riojas on a path to well-paying jobs after graduation, often in lieu of a four-year degree.

This program “is not a ‘Last Chance U,'” said Erin Haughey, Riverview’s principal. “If we have students who are highly motivated, they want to learn the skill, they want to be in the trade, then they get to stay in our community and they get to do a job they love.”

With the capacity for 20 students in the workshop at a time, and only three classes offered each year, there is now a waiting list to get in, she said. Of the 120 students who sign up each spring, only 60 ultimately secure spots.

“I could fill Jeff’s classroom twice over,” said Haughey, referring to Jeff Lahdenpera, the building trades teacher.

More from Personal Finance:

Teens are losing faith in college

These are the top 10 highest-paying college majors

The sticker price at some colleges is now nearly $100,000 a year

“It’s not only throwing nails and two by fours,” Lahdenpera said. Students can get certified in carpentry, plumbing and electrical work, and continue on to pursue various specialties, including construction management, administration, logistics and transportation, marketing and graphics or human resources.

“Construction trades is not just the physical part, there’s other parts of it that encompass the whole industry,” Lahdenpera said.

Construction worker shortage is boosting pay

In addition to providing students with a career-connected pathway available at a lower cost than a four-year college, Riverview’s construction academy was also created to help address a local labor shortage, which mirrors what is happening nationwide.

The academy was funded, in part, by a $50,000 donation from Neal Communities, a private builder based in Lakewood Ranch, Florida.

“There’s a lot of development that’s happening right now in our counties,” said Katie Alderman, Neal’s community affairs coordinator.

America needs construction workers. This year, the construction industry would have to attract more than half a million workers more on top of the normal pace of hiring to meet the demand for labor, according to a model developed by Associated Builders and Contractors. Currently, the unemployment rate in the industry is 3.2%, well below the national average of 4.2%.

The shortage of skilled tradespeople, largely due to experienced workers aging out of the field, is not only boosting the number of job opportunities but also the pay.

In fact, new construction hires earn more than new hires in the professional services, according to payroll-services provider ADP.

At the end of last year, median pay for new hires in construction was $48,089, up 5.1% from a year earlier. The median pay for new hires in professional services was nearly $10,000 lower, at $39,520, up just 2.7% from the year before.

“This is just the law of supply and demand,” said certified financial planner Ted Jenkin, CEO and founder of oXYGen Financial in Atlanta.

Gen Z is becoming the ‘toolbelt generation’

Roughly half, 49%, of high schoolers now believe a high school degree, trade program, two-year degree or other type of enrichment program is the highest level of education needed for their anticipated career path, according to a report by Junior Achievement and Citizens Bank.

Even more — 56% — believe that real world and on-the-job experience is more beneficial than obtaining a higher education degree. The survey polled 1,000 teenagers between the ages of 13 and 18 in July.

There’s an insulting presumption that a four-year college is the gold standard — it’s not.

Ted Jenkin

CEO and founder of oXYGen Financial

The college affordability crisis and the rise of alternative career pathways, together, are helping transform Generation Z into the so-called “toolbelt generation,” according to Jenkin, who is also a member of CNBC’s Financial Advisor Council.

“There’s an insulting presumption that a four-year college is the gold standard — it’s not,” Jenkin said.

From 2022 to 2023, enrollment in vocational programs jumped 16%, the National Student Clearinghouse found. And many of these young adults are benefiting from the secure job track and high earnings potential these vocational jobs now provide, Jenkin said.

“The delta between white-collar jobs and good blue-collar jobs is not that big anymore,” Jenkin said. “That gap is closing.”

Personal Finance

Algorithmic Wealth Management: Balancing Automated Financial Planning with Human Oversight

Personal Finance

High-Yield Optimization: Structuring Personal Cash Reserves in a Sustained Rate Environment

Global Stock Market Analysis and Key Trends Across Europe and East Asia

Memory Stock Rally and Recent Volatility increased fear among tech investors

Energy Stocks Outperform as Crude Surges Past $100

Armanino adds Strategic Accounting Outsourced Solutions

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

Tax Strategy: Employee Retention Credit update

-

Economics6 days ago

Economics6 days agoThe Warsh Shift: How the New Fed Chair Is Balancing War Drags and Tech Winds

-

Economics5 days ago

Economics5 days agoGlobal Trade Realignment and Supply Chains in 2026

-

Economics5 days ago

Economics5 days agoLabor Market Calibration: Analyzing the Shift Toward Skill-Based Allocation in 2026

-

Finance1 week ago

Finance1 week agoSouth Korea Raises Interest Rates to 2.75% for the First Time in More Than Three Years

-

Finance5 days ago

Finance5 days agoTokenized Real-World Assets: Institutional Ledger Adoption Achieves Scale in July 2026

-

Leaders1 week ago

Leaders1 week agoBerkshire Hathaway Chairman Reshapes His Long-Term Philanthropic Strategy

-

Economics1 week ago

Economics1 week agoGlobal Stock Market Weekly Recap: Tech Sell-Off Sparks International Rout

-

Economics4 days ago

Economics4 days agoGlobal Grid Upgrades Reshape Macro Economics