Accounting

Embracing Sufficient Truth for finance and AI success

For decades, the “Single Version of Truth” has been the gold standard for finance and accounting professionals seeking to reconcile data across the enterprise. The instinct is understandable: a perfectly balanced ledger and a single, agreed-upon dataset are foundational to financial integrity. But as technology and business needs evolve — particularly with the rise of AI and data science — the pursuit of a single, perfect dataset is no longer just unrealistic; it can hinder progress.

Today’s finance leaders face mounting pressure to deliver faster and more actionable insights. Data and analytics are CFOs’ top priority, yet many organizations stall major technology initiatives, from ERP upgrades to AI pilots, because they’re waiting for their data to be “perfect” before taking the next step. This is a costly mistake.

The reality is that, in a modern enterprise, a true Single Version of Truth is nearly impossible to achieve. Data is distributed across countless systems, each with its own definitions and business logic. Even if you could force every stakeholder onto a single dataset, the process would be expensive, slow and fraught with politics. Worse, by the time you’re done, much of the data will already be out of date or irrelevant for decision-making.

Instead, forward-thinking finance leaders are embracing the concept of “Sufficient Truth.” This approach pursues informed trade-offs between the cost of bad data and the cost of additional governance. It’s about ensuring data is “fit for purpose”— clean and governed enough to support compliance, reporting and analytics, but not so rigid that it stifles innovation or responsiveness.

Data fabric, data mesh and the illusion of unity

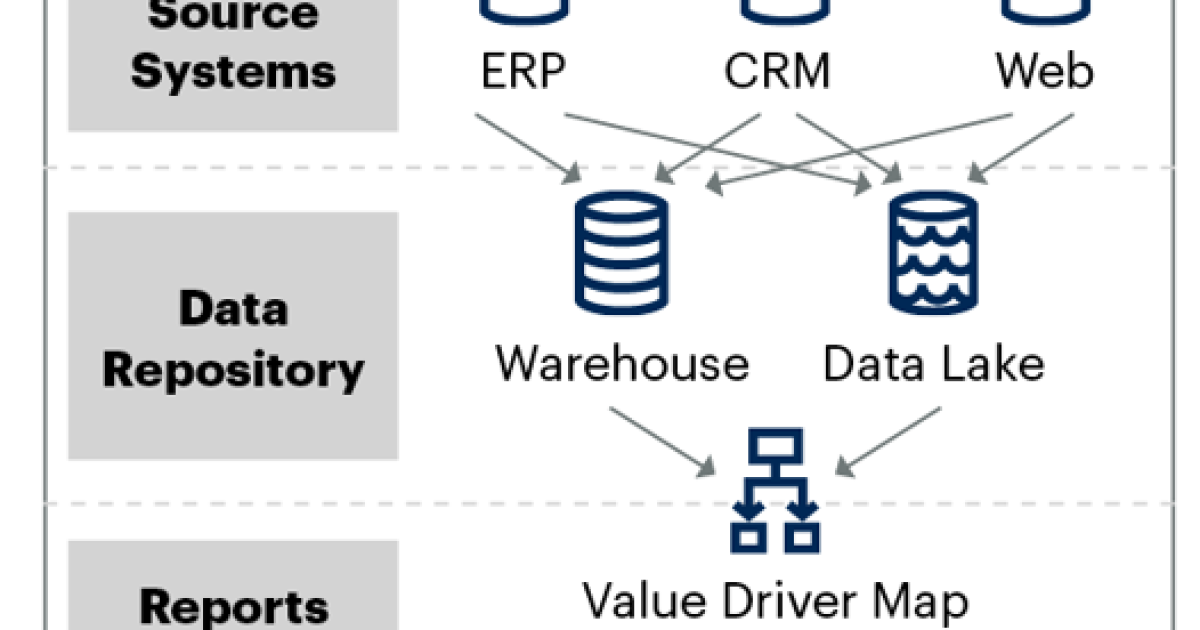

Emerging technologies like data fabric and data mesh are changing the landscape. These federated or virtualized platforms present users with a seamless experience, hiding the complexity of multiple underlying data sources. To the end user, it looks like a single unified source — even though data may actually reside in many silos.

This is a game-changer for finance and AI. With a data fabric, access to information is enabled to a degree never seen before. However, it’s critical to recognize that the “single” view is a product of technology, not a guarantee of perfect, immutable data. Data security, access controls and governance are more important than ever, particularly when sensitive financial or HR data is involved.

The fit-for-purpose approach: centralized where it matters, flexible where it counts

Sufficient Truth is not about abandoning standards. Data should include a variety of source systems and data repositories that are clean enough to support compliance and core reporting, but not so rigidly governed that it stifles innovation.

Gartner (August 2025)

Certain data, especially master data like customers, vendors or employees, must be tightly governed and consistent across the enterprise. This is especially true for financial reporting, where immutability and auditability are nonnegotiable. Controllers and CFOs must ensure that the data underlying the P&L, balance sheet and cash flow statements is reliable and defendable.

But not all data requires this level of rigor. Many data elements, such as addresses used by different departments, or rapidly changing operational metrics, benefit from a more flexible, federated governance model. Sufficient Truth means centralizing governance where ambiguity is unacceptable and pushing it out to regional or local teams where greater flexibility is needed. The result is a data environment that is more fit for purpose, rather than fit to a singular, rigid standard.

AI and Sufficient Truth: progress without perfection

A common myth is that AI and advanced analytics require perfect data. AI can actually function and even thrive with data of varying quality and completeness. AI models can fill gaps, normalize inconsistent inputs, and even generate synthetic data to address missing information. The key is to anchor your data governance and master data management to business needs and outcomes, not to an unattainable ideal of perfection.

Consider the example of an oil and gas company that used AI to optimize rig performance. Their data was at first messy and inconsistent, but by focusing on the data that matters most for their decision models, they are more apt to achieve significant operational improvements and millions in savings — without waiting for perfect data.

The Sufficient Truth approach is about incremental progress. Define your use case, govern your data to the extent necessary for that purpose, deploy your analytics or AI, and then move on to the next business outcome. This cycle allows finance teams to avoid the “boil the ocean” trap and deliver value quickly, even as data quality continues to improve over time.

The future is Sufficient Truth

The era of the Single Version of Truth as the only acceptable standard is over. Finance must adopt a toolkit of approaches that balance accuracy, speed, flexibility, and business relevance. Sufficient Truth makes smart, risk-based decisions about where to invest in data quality and governance, and where to accept “good enough” to keep the business moving forward.

Stop waiting for perfect data. Start building a data strategy that is sufficient for your needs, robust where it counts, and flexible enough to enable the next wave of finance innovation — including AI.

Grant Faulkner Nelson is a vice president, team manager and key initiative leader at

Since joining the company in 2019, he has become well-known for his ability to professionally challenge both experts’ and clients’ D&A predispositions with constructive alternatives. His 22 years of practitioner experience leading D&A strategy, D&A governance and MDM, advanced analytics, COEs, FP&A, management reporting and dashboarding) enables him to comfortably flex with clients’ needs. Additionally, his down-to-earth approach has made him highly sought after by many within both the finance and analytics functions. He earned his MBA from Georgia State University’s Robinson College of Business and his B.S. from the University of Colorado, Boulder in International Affairs. As a family man and former rugby player, he enjoys staying active and, after hours, is often found coaching his daughters’ sports teams.

UK Has a New Prime Minister Without a General Election

Adaptive Governance in Volatile Markets

Navigating Sovereign Data Residency Mandates in the Age of AI

Armanino adds Strategic Accounting Outsourced Solutions

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

Tax Strategy: Employee Retention Credit update

-

Economics4 days ago

Economics4 days agoGlobal Trade Realignment and Supply Chains in 2026

-

Economics5 days ago

Economics5 days agoThe Warsh Shift: How the New Fed Chair Is Balancing War Drags and Tech Winds

-

Economics4 days ago

Economics4 days agoLabor Market Calibration: Analyzing the Shift Toward Skill-Based Allocation in 2026

-

Finance6 days ago

Finance6 days agoSouth Korea Raises Interest Rates to 2.75% for the First Time in More Than Three Years

-

Leaders6 days ago

Leaders6 days agoBerkshire Hathaway Chairman Reshapes His Long-Term Philanthropic Strategy

-

Finance4 days ago

Finance4 days agoTokenized Real-World Assets: Institutional Ledger Adoption Achieves Scale in July 2026

-

Economics6 days ago

Economics6 days agoGlobal Stock Market Weekly Recap: Tech Sell-Off Sparks International Rout

-

Accounting4 days ago

Accounting4 days agoStandardizing Global ESG Reporting: Key Compliance Imperatives for Mid-Year 2026