Accounting

Stephano Slack tops slow quarter for new SEC audit clients

The departure of audit firms from the Securities and Exchange Commission market can prove a boon for those who remain: Pennsylvania-based auditor Stephano Slack brought on the most new SEC clients in the fourth quarter of 2024 thanks to picking up engagements from an exiting firm — a repeat of

Wayne, Pennsylvania-based Stephano Slack grabbed 11 new clients (and netted 10) from Blue Bell, Pennsylvania-based Morison Cogen, which stopped providing audit services to publicly traded companies in the fall of 2025. (See “

That isn’t the only way to pick up new clients, of course: Houston-based HTL International added six of its eight new clients in Q4 from TPS Thayer in Sugar Land, Texas, after the two firms created a strategic collaboration in November that included HTL bringing on the audit team of TPS Thayer.

And while it was a relatively slow quarter for the largest auditing firms, the combination of CBIZ/CBIZ CPAs and Marcum late last year looks likely to benefit a range of audit firms, with Marcum shedding a net of 27 firms. Three out of CBIZ CPAs’ six new clients came from Marcum, while lots of other firms picked up individual Marcum clients. (See “

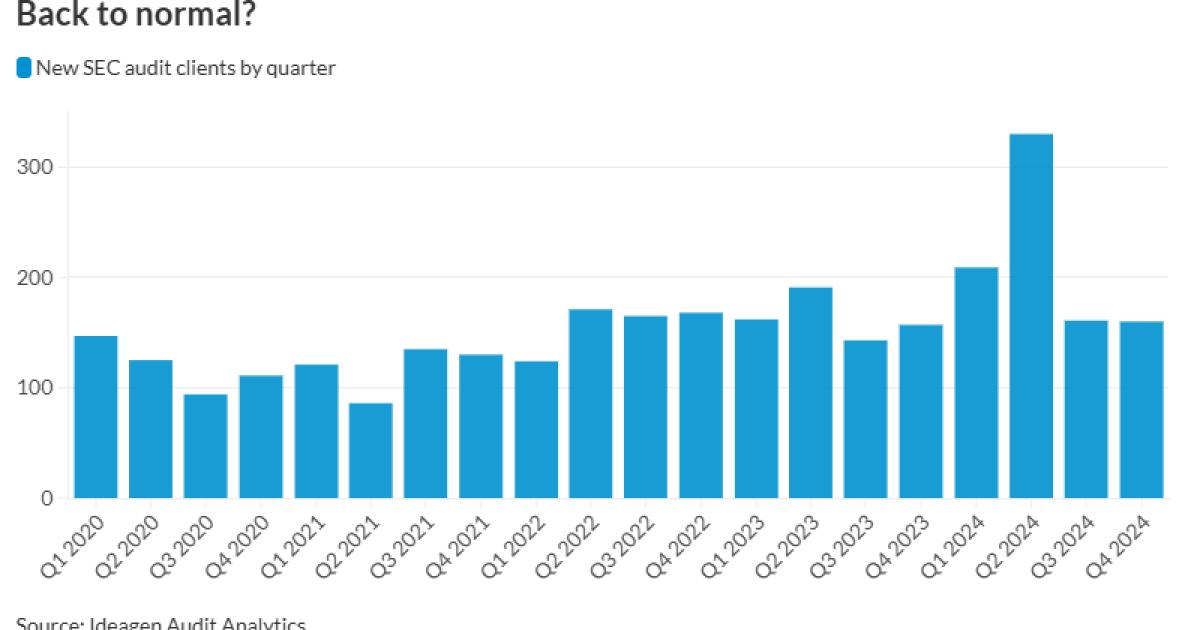

The total number of new engagements hit 160, roughly the same as Q3 and much lower than previous two quarters (which had been boosted in part by the implosion of audit firm BF Borgers), but still well above the low numbers from the midst of the COVID pandemic.

SEC clients by filing status, and more

In terms of clients by filing status, KPMG once again led among new large accelerated filers, while Stephano Slack took the lead among non-accelerated filers and small reporting companies. (See “

BDO USA took the lead among large auditors in terms of new clients in Q4, and that helped it top the league tables for new market capitalization audited, with the overwhelming majority coming in the form of computer server manufacturer Super Micro Computer Inc.’s $49 billion. BDO also took second in new audit fees, thanks again to Super Micro, which accounted for $4.76 million of the firm’s $5.84 million. (See “

Meanwhile, PwC came first in new assets audited, thanks largely to adding asset manager Nuveen, while KPMG came first in new audit fees, with natural gas and electric power distribution company UGI Corp. contributing the most, at $9 million. KPMG also came second in new market cap and new assets audited.

Data for the quarterly rankings are provided by Ideagen Audit Analytics, a premium online intelligence service delivering audit, regulatory and disclosure analysis. Reach them at (508) 476-7007,

Senate Republicans included a tax break estimated to be worth more than $1 billion for oil and gas producers in their version of President Donald Trump’s sprawling fiscal package.

The provision would allow energy companies subject to a 15%

The change, included in the legislation released Monday by Republicans on the Senate tax writing committee, is nearly identical to a

Lankford’s bill, called the Promoting Domestic Energy Production Act, would cost the US government $1.1 billion over 10 years,

A representative for Lankford declined to comment.

Earlier this year, Lankford told

“If we can’t get rid of that entirely we at least need to give some relief to those folks who are independent producers,” Lankford said. “We need to be able to get some relief to them so they’re not constantly worried about it.”

Environmental and watchdog groups including Friends of the Earth and Public Citizen panned the provision included in the Senate bill as a giveaway to fossil fuel companies.

“This proposal would introduce a massive new loophole for oil and gas companies,” said Lukas Shankar-Ross, deputy director for climate for Friends of the Earth.

Wealthy U.S. colleges scored a win on Monday with the release of Senate Republicans’

Private universities with at least 500 students that have endowments of $2 million per pupil or more would pay an excise tax of 8% under the new bill released by the Senate Committee on Finance. The levy would be placed on net-investment income earned by the endowments. That’s much lower than the 21% rate that was included in the House proposal, which passed the chamber in May.

The endowment tax would raise revenue to offset President Donald Trump’s tax cuts and it would punish universities that are “

Under the new proposal, institutions with endowments of $750,000 to $1,999,999 per student would face a tax of just 4%. Under the

Religious schools would be exempt from the tax in both the House and Senate proposals. The

Karin Johns, director of tax policy for the National Association of Independent Colleges and Universities, said the tax should be eliminated and not expanded.

“The tax remains purely punitive, unfairly impacts one sector of higher education, disincentivizes charitable giving, and siphons funds to the federal government used to support students and their families,” she said in an emailed statement.

-

Accounting1 week ago

Accounting1 week agoInstead adds AI-driven tax reports

-

Economics1 week ago

Economics1 week agoSending the National Guard to LA is not about stopping rioting

-

Personal Finance1 week ago

Personal Finance1 week agoWhat Pell Grant changes in Trump budget, House tax bill mean for students

-

Personal Finance1 week ago

Personal Finance1 week agoHow markets performed for investors so far

-

Personal Finance1 week ago

Personal Finance1 week agoTrump’s ‘big beautiful’ bill may curb access to low-income tax credit

-

Economics1 week ago

Economics1 week agoIs there a “woke right” in America?

-

Finance1 week ago

Finance1 week agoChina’s EV race to the bottom leaves a few possible winners

-

Finance1 week ago

Finance1 week agoGundlach says to buy international stocks on dollar’s ‘secular decline’