Do you know who loves tax season?

Personal Finance

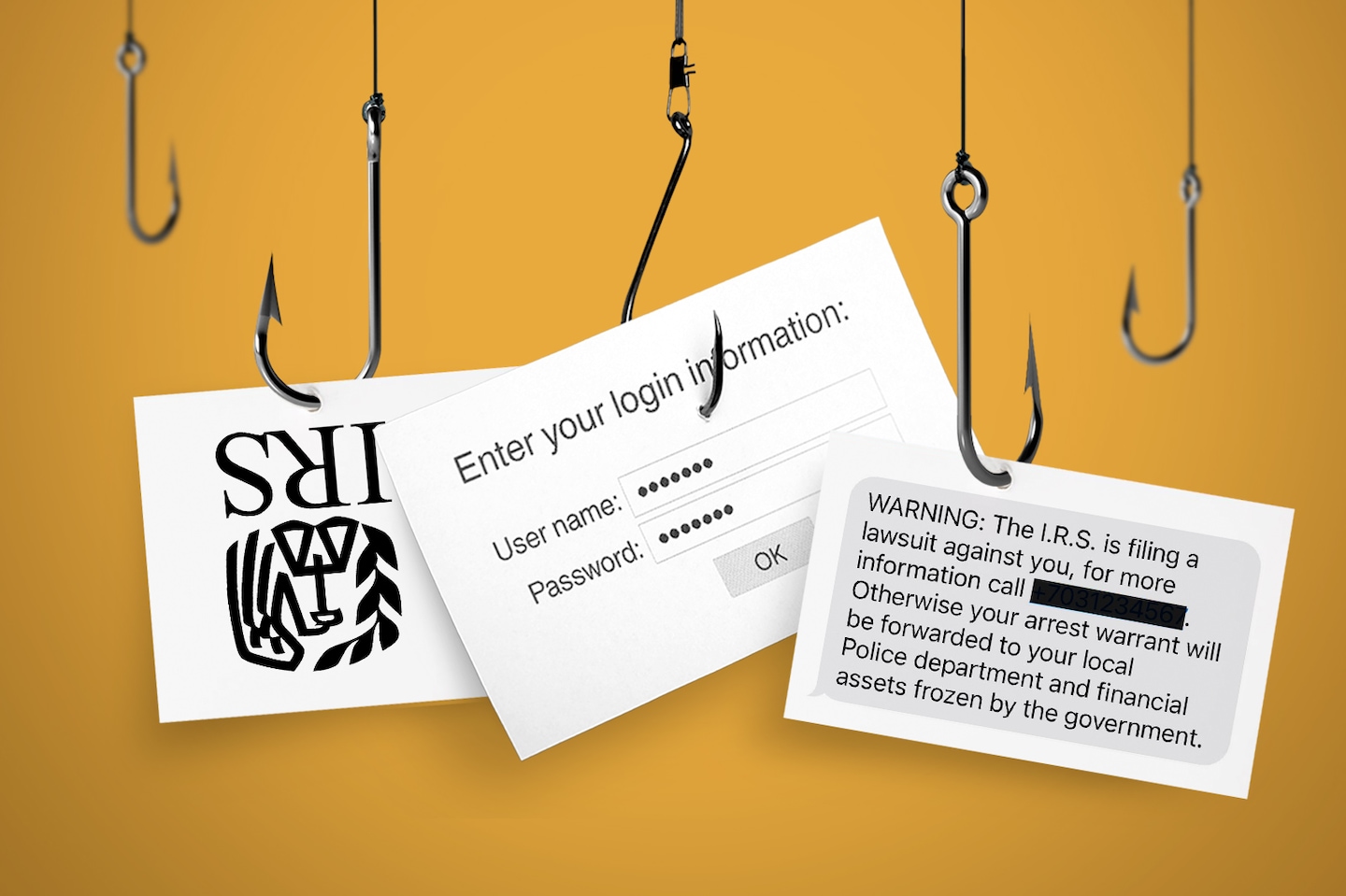

Tax time is prime time for scammers and scheming tax preparers

Personal Finance

Algorithmic Wealth Management: Balancing Automated Financial Planning with Human Oversight

Personal Finance

High-Yield Optimization: Structuring Personal Cash Reserves in a Sustained Rate Environment

Economics3 days ago

UK Has a New Prime Minister Without a General Election

Leaders3 days ago

Adaptive Governance in Volatile Markets

Insights3 days ago

Navigating Sovereign Data Residency Mandates in the Age of AI

Accounting1 year ago

Armanino adds Strategic Accounting Outsourced Solutions

Accounting2 years ago

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

Accounting2 years ago

Tax Strategy: Employee Retention Credit update

-

Economics4 days ago

Economics4 days agoGlobal Trade Realignment and Supply Chains in 2026

-

Economics5 days ago

Economics5 days agoThe Warsh Shift: How the New Fed Chair Is Balancing War Drags and Tech Winds

-

Economics4 days ago

Economics4 days agoLabor Market Calibration: Analyzing the Shift Toward Skill-Based Allocation in 2026

-

Finance6 days ago

Finance6 days agoSouth Korea Raises Interest Rates to 2.75% for the First Time in More Than Three Years

-

Leaders6 days ago

Leaders6 days agoBerkshire Hathaway Chairman Reshapes His Long-Term Philanthropic Strategy

-

Finance4 days ago

Finance4 days agoTokenized Real-World Assets: Institutional Ledger Adoption Achieves Scale in July 2026

-

Economics6 days ago

Economics6 days agoGlobal Stock Market Weekly Recap: Tech Sell-Off Sparks International Rout

-

Accounting4 days ago

Accounting4 days agoStandardizing Global ESG Reporting: Key Compliance Imperatives for Mid-Year 2026