Personal Finance

CFPB fines Equifax $15 million for errors on credit reports

Elijah Nouvelage/Bloomberg via Getty Images

The Consumer Financial Protection Bureau fined Equifax $15 million over errors tied to consumer credit reports, alleging the company failed to conduct proper investigations of disputed information, the federal watchdog announced Friday.

Equifax is one of three major credit reporting agencies in the U.S., a group that also includes Experian and TransUnion.

“Equifax ignored consumer documents and evidence submitted with disputes, allowed previously deleted inaccuracies to be reinserted into credit reports, provided confusing and conflicting letters to consumers about the results of its investigations, and used flawed software code which led to inaccurate consumer credit scores,” according to the CFPB’s order.

Why credit reports are important

Credit reports are a ledger of consumers’ borrowing records, such as loan payment history and bankruptcy filings.

The financial consequences of inaccurate information on those reports can be “severe,” said Adam Rust, director of financial services at the Consumer Federation of America, a consumer advocacy group.

“It can change your ability to qualify for a loan, to get a job, to rent an apartment, all kinds of things that are very fundamental to navigating your personal life,” Rust said.

Equifax had ‘flawed’ process, CFPB says

Equifax processes about 765,000 consumer disputes a month, CFPB said.

Its “flawed” dispute policies and technology failures occurred since at least October 2017, “to the detriment of millions of consumers,” according to the CFPB, which alleged Equifax violated the Fair Credit Reporting Act.

More from Personal Finance:

Expert predictions for interest rates in 2025

Over 1 million people got student debt forgiven in 2024

Nearly half of credit card users are carrying debt

Equifax settled the allegations to “[turn] the page on the CFPB’s long-running investigation,” a company spokesperson wrote in an e-mail.

The company has invested more than $1.5 billion into technology and infrastructure improvements over the last few years, including “significant changes” to its dispute process and consumer support, the spokesperson said.

“Our Purpose is to help people live their financial best and we know consumers and our customers depend on our data for important financial decisions,” they wrote. “Even one error affecting a consumer is one error too many,” they added.

The $15 million civil penalty follows a lawsuit CFPB filed against another credit bureau, Experian, on Jan. 7, alleging the company conducted “sham” investigations of credit report errors. In a statement on its site, Experian said the lawsuit was “completely without merit” and an “example of irresponsible overreach.”

“Credit bureaus have been sued repeatedly for this kind of conduct,” said Chi Chi Wu, senior attorney at the National Consumer Law Center. “They’re decades-old problems,” she said.

An Equifax data breach in 2017 also compromised the personal information of 147 million consumers, for which the company ultimately agreed to settle for $700 million.

How to have good ‘hygiene’ with credit reports

Consumers should check their credit reports at least once a year, Rust said. The Federal Trade Commission also recommends doing a check before applying for credit, a loan, insurance or a job.

Consumers should ensure they recognize identity information on their credit report like addresses and Social Security numbers, and verify that account information such as debt balances and delinquency status are correct.

“That’s just a good practice of financial hygiene,” Rust said.

Importantly, a credit report differs from a credit score. The latter is a numerical output compiled with information on a consumer’s credit report.

“If you see a sudden change in credit score, that’s a signal,” Rust said.

The three major credit bureaus allow consumers to request a free copy of their credit report once a week. Consumers can request a copy at AnnualCreditReport.com and by calling 1-877-322-8228. (Other sites may charge consumers or be fraudulent, according to the Federal Trade Commission.)

What to do about a credit report error

Smith Collection/gado | Archive Photos | Getty Images

Consumers who see an error on their credit report should lodge a dispute in writing, along with documentation. Send that by postal mail to the credit bureau and request a return receipt, Wu said. Consumers have better odds of resolution by mail than online, she said.

Consumers should also file a complaint with the CFPB and their state attorney general’s office, Wu said.

Consumers can ask that a statement of their dispute be included in their file and in future credit reports, and also ask the credit bureau to provide their statement to anyone who received a copy of their report in the recent past, Wu said.

Consumers who can’t get an error fixed after repeated attempts may wish to consult an attorney, she said.

“Not every error will be worth bringing a lawsuit,” she said. “But if your loan ends up being more expensive because of a credit reporting error, that’s the kind of real harm [for which] you may want to consider litigation.”

They may be able to find an attorney through organizations like the National Association of Consumer Advocates, Wu said.

People enjoy an unusually warm day in New York City as temperatures reach the low 80s on June 4, 2025 in New York City.

Spencer Platt | Getty Images

Summer Fridays may be considered the most desirable perk of the season, but fewer employers are on board with the shortened workweek.

Companies have steadily phased out summer Fridays — a policy that allows workers to take Friday afternoon off over the summer months — as work-from-home Fridays became more common, experts say.

“Pre-pandemic, summer Fridays were thing, but hybrid overall has taken over,” said Bill Driscoll, technology workplace trends expert at staffing and consulting firm Robert Half.

As more commuters settle into flexible working arrangements, fewer workers are making Friday trips at all compared to mid-week traffic patterns, according to the 2024 Global Traffic Scorecard released in January by INRIX Inc., a traffic-data analysis firm.

More from Personal Finance:

Job market is ‘trash’ right now, career coach says

Millions would lose health insurance under GOP megabill

Average 401(k) balances drop 3% due to market volatility

Among employees, however, summer Fridays are the most valued summer benefit, followed by summer hours and flextime, according to a new survey by job site Monster, which polled more than 400 U.S. workers in June.

“Summer Fridays are highly valued among workers because, for many, they represent more than just a few extra hours off,” said Scott Blumsack, Monster’s chief strategy and marketing officer. This perk “can go a long way in showing employees they’re valued, which can help prevent burnout, boost morale, and improve retention during a season when disengagement can run high.”

Still, 84% of workers are not offered any summer-specific benefits, even though 55% also said those benefits improve productivity, Monster found.

Instead, hybrid — and to a lesser extent fully remote — job postings have increased in the last year as employers compete for talented job seekers who prioritize flexibility, according to research by Robert Half.

“Hybrid is a highly desirable situation right now and one that all levels of employees are looking for,” said Robert Half’s Driscoll.

More than five years after the pandemic, 72% of organizations also have return-to-office mandates, according to a separate hybrid work study by Cisco.

But, even with the mandates, employees are less likely to work in the office on Fridays, and much more likely to commute Monday to Thursday, Cisco found.

Employees value flexibility

As employee burnout and disengagement grows amid the wave of in-office mandates, work-life balance and flexible hours have become increasingly important, other studies show.

Corporate wellness company Exos, which works with large organizations such as JetBlue and Adobe, says burnout has gone down significantly among employees at firms that have made Fridays more flexible. Exos also tested out “You Do You Fridays” — and found significant benefits.

The more adaptable the schedule, the more positively employees view their company’s policies, the Cisco report also found.

With hybrid arrangements now common, workers put a high value on that flexibility — and 63% of all workers would even accept a pay cut for the option to work remotely more often, according to Cisco’s global survey of more than 21,500 employers and employees working full-time.

Speaker of the House Mike Johnson, R-La., pictured at a press conference after the House narrowly passed a bill forwarding President Donald Trump’s agenda on May 22 in Washington, DC.

Kevin Dietsch | Getty Images

House reconciliation legislation, also known as the One, Big, Beautiful Bill, includes changes aimed at helping to boost family’s finances.

Those proposals — including $1,000 investment “Trump Accounts” for newborns and an enhanced maximum $2,500 child tax credit — would help support eligible parents.

Proposed tax cuts in the bill may also provide up to $13,300 more in take-home pay for the average family with two children, House Republicans estimate.

“What we’re trying to do is help hardworking Americans who are trying to provide for their families and make ends meet,” House Speaker Mike Johnson, R-La., said during a June 8 interview with ABC News’ “This Week.”

Yet the proposed changes, which emphasize work requirements, may reduce aid for children in low-income families when it comes to certain tax credits, health coverage and food assistance.

Households in the lowest decile of the income distribution would lose about $1,600 per year, or about 3.9% of their income, from 2026 through 2034, according to a June 12 letter from the Congressional Budget Office. That loss is mainly due to “reductions in in-kind transfers,” it notes — particularly Medicaid and the Supplemental Nutrition Assistance Program, or SNAP, formerly known as food stamps.

20 million children won’t get full $2,500 child tax credit

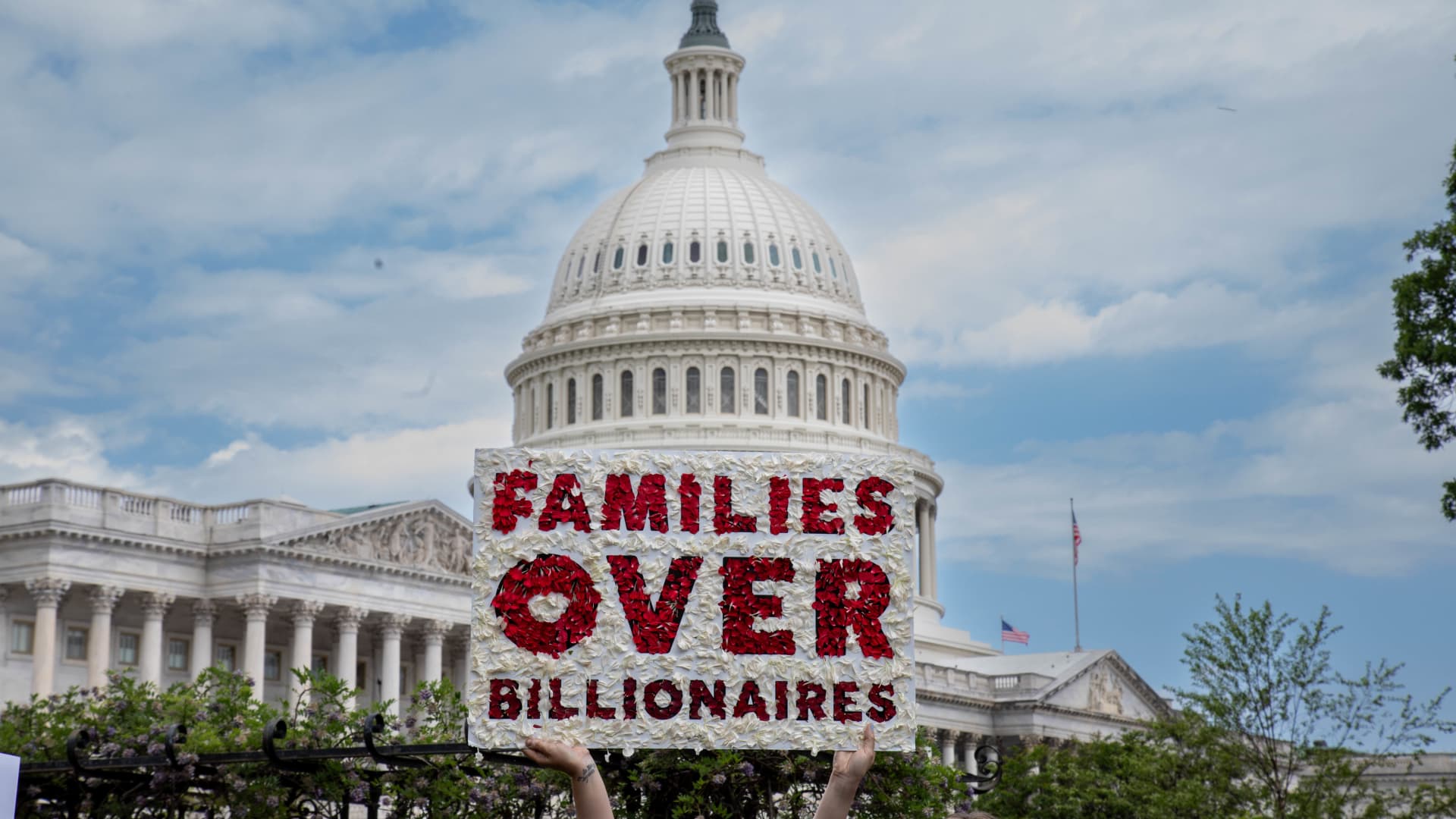

A member of MomsRising holds a sign on Capitol Hill to urge lawmakers to reject tax breaks for billionaires and protest cuts to Medicaid and child care on Capitol Hill on May 8 in Washington, D.C.

Brian Stukes | Getty Images Entertainment | Getty Images

House Republicans have proposed increasing the maximum child tax credit to $2,500 per child, up from $2,000, a change that would go into effect starting with tax year 2025 and expire after 2028.

The change would increase the number of low-income children who are locked out of the child tax credit because their parents’ income is too low, according to Adam Ruben, director of advocacy organization Economic Security Project Action. The tax credit is not refundable, meaning filers can’t claim it if they don’t have a tax obligation.

Today, there are 17 million children who either receive no credit or a partial credit because their family’s income is too low, Ruben said. Under the House Republicans’ plan, that would increase by 3 million children. Consequently, 20 million children would be left out of the full child tax credit because their families earn too little, he said.

“It is raising the credit for wealthier families while excluding those vulnerable families from the credit,” Ruben said. “And that’s not a pro-family policy.”

A single parent with two children would have to earn at least $40,000 per year to access the full child tax credit under the Republicans’ plan, he said. For families earning the minimum wage, it may be difficult to meet that threshold, according to Ruben.

In contrast, an enhanced child tax credit put in place under President Joe Biden made it fully refundable, which means very low-income families were eligible for the maximum benefit, according to Elaine Maag, senior fellow at the Urban-Brookings Tax Policy Center.

In 2021, the maximum child tax credit was $3,600 for children under six and $3,000 for children ages 6 to 17. That enhanced credit cut child poverty in half, Maag said. However, immediately following the expiration, child poverty increased, she said.

The current House proposal would also make about 4.5 million children who are citizens ineligible for the child tax credit because they have at least one undocumented parent who files taxes with an individual tax identification number, Ruben said. Those children are currently eligible for the child tax credit based on 2017 tax legislation but would be excluded based on the new proposal, he said.

New red tape for a low-income tax credit

House Republicans also want to change the earned income tax credit, or EITC, which targets low- to middle-income individuals and families, to require precertification to qualify.

When a similar requirement was tried about 20 years ago, it resulted in some eligible families not getting the benefit, Maag said. The new prospective administrative barrier may have the same result, she said.

More than 2 million children’s food assistance at risk

Momo Productions | Digitalvision | Getty Images

House Republican lawmakers’ plan includes almost $300 billion in proposed cuts to the Supplemental Nutrition Assistance Program, or SNAP, through 2034.

SNAP currently helps more than 42 million people in low-income families afford groceries, according to Katie Bergh, senior policy analyst at the Center on Budget and Policy Priorities. Children represent roughly 40% of SNAP participants, she said.

More than 7 million people may see their food assistance either substantially reduced or ended entirely due to the proposed cuts in the House reconciliation bill, estimates CBPP. Notably, that total includes more than 2 million children.

“We’re talking about the deepest cut to food assistance ever, potentially, if this bill becomes law,” Bergh said.

More from Personal Finance:

Experts weigh pros and cons of $1,000 Trump baby bonus

How Trump spending bill may curb low-income tax credit

Why millions would lose health insurance under House spending bill

Under the House proposal, work requirements would apply to households with children for the first time, Bergh said. Parents with children over the age of 6 would be subject to those rules, which limit people to receiving food assistance for just three months in a three-year period unless they work a minimum 20 hours per week.

Additionally, the House plan calls for states to fund 5% to 25% of SNAP food benefits — a departure from the 100% federal funding for those benefits for the first time in the program’s history, Bergh said.

States, which already pay to help administer SNAP, may face tough choices in the face of those higher costs. That may include cutting food assistance or other state benefits or even doing away with SNAP altogether, Bergh said.

While the bill does not directly propose cuts to school meal programs, it does put children’s eligibility for them at risk, according to Bergh. Children who are eligible for SNAP typically automatically qualify for free or reduced school meals. If a family loses SNAP benefits, their children may also miss out on those benefits, Bergh said.

Health coverage losses would adversely impact families

A protestor holds a sign on May 7, 2025 in Washington, D.C.

Leigh Vogel | Getty Images Entertainment | Getty Images

Families with children may face higher health care costs and reduced access to health care depending on how states react to federal spending cuts proposed by House Republicans, according to the Center on Budget and Policy Priorities.

The House Republican bill seeks to slash approximately $1 trillion in spending from Medicaid, the Children’s Health Insurance Program and Affordable Care Act marketplaces.

Medicaid work requirements may make low-income individuals vulnerable to losing health coverage if they are part of the expansion group and are unable to document they meet the requirements or qualify for an exemption, according to CBPP. Parents and pregnant women, who are on the list of exemptions, could be susceptible to losing coverage without proper documentation, according to the non-partisan research and policy institute.

Eligible children may face barriers to access Medicaid and CHIP coverage if the legislation blocks a rule that simplifies enrollment in those programs, according to CBPP.

In addition, an estimated 4.2 million individuals may be uninsured in 2034 if enhanced premium tax credits that help individuals and families afford health insurance are not extended, according to CBO estimates. Meanwhile, those who are covered by marketplace plans would have to pay higher premiums, according to CBPP. Without the premium tax credits, a family of four with $65,000 in income would pay $2,400 more per year for marketplace coverage.

Artificial intelligence makes people more valuable, according to PwC’s 2025 Global AI Jobs Barometer report.

Pixdeluxe | E+ | Getty Images

While there hasn’t been much hiring for so-called “white collar” jobs, the contraction is not because of artificial intelligence, economists say. At least, not yet.

Professional and business services, the industry that represents white-collar roles and middle and upper-class, educated workers, hasn’t experienced much hiring activity over the past two years.

In May, job growth in professional and business services declined to -0.4%, slightly down from -0.2% in April, according to the Bureau of Labor Statistics. In other words, the sector has been losing job opportunities, according to Cory Stahle, an economist at job search site Indeed.

Meanwhile, industries like health care, construction and manufacturing have seen more job creation. In May, nearly half of the job growth came from health care, which added 62,000 jobs, the bureau found.

More from Personal Finance:

Here’s what’s happening with unemployed Americans — in five charts

The pros and cons of a $1,000 baby bonus in ‘Trump Accounts’

Social Security cost-of-living adjustment may be 2.5% in 2026

However, economists have said that the decline in white-collar job openings is more driven by structural issues in the economy rather than artificial intelligence technology taking people’s jobs.

“We know for a fact that it’s not AI,” said Alí Bustamante, an economist and director at the Roosevelt Institute, a liberal think tank.

Indeed’s Stahle agreed: “This is more of an economic story and less of an AI disruption story, at least so far.”

Artificial intelligence is still in early stages

There are a few reasons AI is not behind the declining job creation in white-collar sectors, according to economists.

For one, the decline in job creation has been happening for years, Bustamante said. In that timeframe, AI technology “was pretty awful,” he said.

What’s more, the technology is even now still in early stages, to the point where the software cannot execute key skills without human intervention, said Stahle.

A 2024 report by Indeed researchers found that of the more than 2,800 unique work skills identified, none are “very likely” to be replaced by generative artificial intelligence. GenAI creates content like text or images based on existing data.

Across five scenarios — “very unlikely,” “unlikely,” “possible,” “likely” and “very likely” — about 68.7% of skills were either “very unlikely” or “unlikely” to be replaced by GenAI technology, the site found.

“We might get to a point where they do, but right now, that’s not necessarily looking like it’s a big factor,” Stahle said.

‘Jobs are going to transform’

While AI has yet to replace human workers, there may come a time where the technology does disrupt the labor force.

“Certainly, jobs are going to transform,” Stahle said. “I’m not going to downplay the potential impacts of AI.”

Stahle said that openings for consulting jobs focused on implementing generative AI have been rising. Over the past year, management consulting roles with AI language accounted for 12.4% of GenAI postings, showing signs of growing demand, per a February report by Indeed.

A separate report by the World Economic Forum in January forecasts that by 2030, the new technology will create 170 million new jobs, or 14% of the current total employment.

However, that growth could be offset by the decline in existing roles. The report cites that about 92 million jobs, or 8% of the current total employment, could be displaced by AI technology.

For knowledge-based workers whose skills may overlap with AI, consider investing in developing skills on how to use AI technology to stay ahead, Stahle said.

Summer Fridays are increasingly rare as hybrid schedules gain steam

How House Republicans’ ‘big beautiful’ bill may affect children

‘White collar’ jobs are down — but don’t blame AI yet, economists say

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Economics7 days ago

Economics7 days agoJobs report May 2025:

-

Economics7 days ago

Economics7 days agoDonald Trump has many ways to hurt Elon Musk

-

Finance7 days ago

Finance7 days agoStocks making the biggest moves midday: WOOF, TSLA, CRCL, LULU

-

Economics5 days ago

Economics5 days agoSending the National Guard to LA is not about stopping rioting

-

Economics7 days ago

Donald Trump has many ways to hurt Elon Musk

-

Blog Post6 days ago

Blog Post6 days agoMastering Bookkeeping Tasks During Peak Business Seasons

-

Personal Finance5 days ago

Personal Finance5 days agoWhat Pell Grant changes in Trump budget, House tax bill mean for students

-

Personal Finance6 days ago

Personal Finance6 days agoForgotten 401(k) fees cost workers thousands in retirement savings