Personal Finance

Here’s the inflation breakdown for March 2024 — in one chart

Eric Thayer/Bloomberg via Getty Images

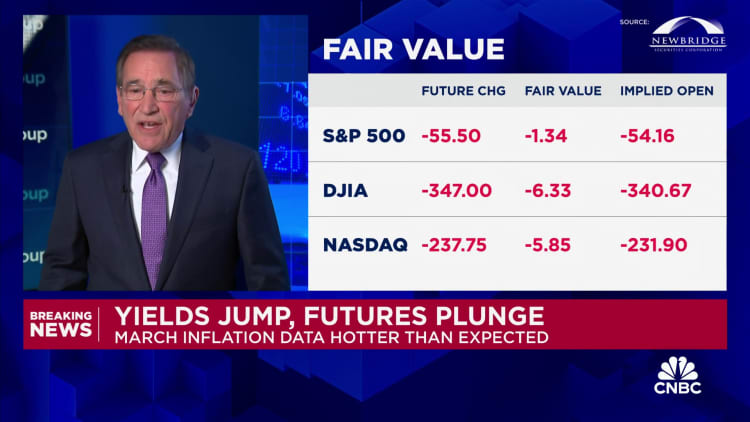

Inflation jumped in March as prices for consumer staples like gasoline edged higher and those for housing remain stubbornly high, suggesting inflation may be a bit stickier than seemed just a few months ago, economists said.

The consumer price index, a key inflation gauge, rose 3.5% in March from a year ago, the U.S. Labor Department reported Wednesday. That’s up from 3.2% in February.

CPI measures how fast prices are changing across the U.S. economy. It measures everything from fruits and vegetables to haircuts, concert tickets and household appliances.

The March inflation reading is down significantly from its 9.1% pandemic-era peak in 2022, which was the highest level since 1981. However, it remains above policymakers’ long-term target around 2%.

Progress in the inflation fight has somewhat flatlined in recent months.

“The disinflation has stalled out,” said Mark Zandi, chief economist at Moody’s Analytics.

“The big rock in the way here is the cost of shelter,” Zandi said.

While housing costs have moderated, they account for the largest share of the CPI inflation index and “are still growing strongly,” he added.

Despite progress having stalled, broader evidence doesn’t suggest a renewed surge in inflation — though it may take longer than expected to bring the rate back to target, economists said. In fact, underlying inflation after stripping out shelter costs is already back to target, Zandi said.

“I still hold to the view that inflation is moderating,” Zandi said. “It’s just taking frustratingly long to get there.”

Household paychecks can buy more stuff, though

Higher oil and gas prices take a toll

Gasoline prices increased 1.7% from February to March, the Bureau of Labor Statistics said. (This figure is adjusted to account for seasonal buying patterns.)

Average U.S. pump prices were $3.52 a gallon on April 1, up from $3.35 on March 4, according weekly data published by the Energy Information Administration.

The increase is largely attributable to higher oil prices. They’ve firmed amid a generally positive outlook for the global economy (meaning greater global oil demand) and controlled output among major oil-producing nations (meaning there hasn’t been a glut of oil), economists said.

Tensions in the Middle East may also be playing a role, Hamrick said.

Higher gas prices may filter through to higher prices elsewhere, since they factor into transportation and distribution costs for goods and even services like food delivery, he said.

Higher energy prices are what worries Zandi most relative to inflation readings. It’s likely the upward trend will continue in coming months, and the dynamic negatively impacts consumer buying power and sentiment, he said.

“Nothing does more damage to the economy more quickly than rising oil and gasoline prices,” he said.

Other ‘notable’ areas of inflation

In addition to shelter, motor vehicle insurance, medical care, recreation and personal care were “notable” contributors to “core” inflation (a reading that strips out volatile energy and food prices), the BLS said.

Shelter, motor vehicle insurance, medical care, apparel and personal care were notable contributors to monthly inflation from February to March, the agency said.

The overall monthly CPI reading, 0.4%, was much higher than the roughly 0.2% that would be expected on a consistently basis to bring inflation back to normal, economists said.

“There is no improvement here; we’re moving in the wrong direction,” Hamrick said.

“The usual trouble spots persist,” said Hamrick, who additionally called out costs for electricity and car maintenance and repairs.

Prices have fallen in some categories

Meanwhile, some consumer categories have seen improvement.

Prices fell for used cars and trucks, new vehicles and airline tickets between February and March, for example. They’re also down over the past year, by 2.2%, 0.1% and 7.1%, respectively, according to CPI data.

Lower prices for new and used cars should lead auto insurance and repair costs to fall as well, economists said.

Grocery prices are another bright spot, they said.

While some categories like eggs and pork chops have seen recent upward movement, the overall “food at home” index stood at 0% on a monthly basis in both February and March.

“Food prices have come to a standstill,” Zandi said. “For most Americans, the thing that bothers them the most about inflation is high food prices.”

Out-of-whack supply and demand

At a high level, supply-and-demand imbalances are what trigger out-of-whack inflation.

For example, the Covid-19 pandemic disrupted supply chains for goods. Americans’ buying patterns also simultaneously shifted away from services — like entertainment and travel — toward physical goods since they stayed at home more, driving up demand and fueling decades-high goods inflation.

Additionally, supply-and-demand dynamics in the labor market pushed wage growth to the highest level in decades, putting upward pressure on prices for services, which are more wage-sensitive.

Now that supply-chain issues are “pretty close to fixed,” there’s “little scope” for goods to contribute to disinflation moving forward, said Sarah House, senior economist at Wells Fargo Economics.

“You need services to take the mantle of disinflation,” because goods have “petered out,” she added.

Housing falls in the services category. It accounts for the largest share of the consumer price index, so disinflation in this category would likely have a large impact on inflation readings.

So far, housing inflation has remained stubbornly high — even as economists have predicted it would start moderating any day given broadly positive trends in prices for new tenant rental leases, for example.

“It seems to be taking a bit longer than people thought,” said Andrew Hunter, deputy chief U.S. economist at Capital Economics.

“It’s coming,” he said. “It’s just a matter of when.”

U.S. Senate Majority Leader John Thune (R-SD) speaks at a press conference following the U.S. Senate Republicans’ weekly policy luncheon on Capitol Hill in Washington, D.C., U.S., June 10, 2025.

Kent Nishimura | Reuters

As Senate Republicans release key details of President Donald Trump‘s spending package, some provisions, including the federal deduction for state and local taxes, known as SALT, remain in limbo.

Enacted via the Tax Cuts and Jobs Act, or TCJA, of 2017, there’s currently a $10,000 limit on the SALT deduction through 2025. Before 2018, the tax break — including state and local income and property taxes — was unlimited for filers who itemized deductions. But the so-called alternative minimum tax reduced the benefit for some higher earners.

The Senate Finance Committee’s proposed text released on Monday includes a $10,000 SALT deduction cap, which is expected to change during Senate-House negotiations on the spending package. That limit is down from the $40,000 cap approved by House Republicans in May.

More from Personal Finance:

Fed is likely to hold rates steady this week. What it means for you

How to protect assets amid immigration raids, deportation worries

IRS: Make your second-quarter estimated tax payment by June 16

The SALT deduction has been ‘contentious’

“SALT has been contentious for eight years,” said Andrew Lautz, associate director for the Bipartisan Policy Center’s economic policy program.

Since 2017, the SALT deduction cap has been a key issue for certain lawmakers in high-tax states like New York, New Jersey and California. These House members have leverage during negotiations amid a slim House Republican majority.

Under current law, filers who itemize tax breaks can’t claim more than $10,000 for the SALT deduction, including married couples filing jointly, which is considered a “marriage penalty.”

However, raising the SALT deduction cap has been controversial. If enacted, benefits would primarily flow to higher-income households, according to a May analysis from the Committee for a Responsible Federal Budget.

Currently, the vast majority of filers — roughly 90%, according to the latest IRS data — use the standard deduction and don’t benefit from itemized tax breaks.

Plus, the 2017 SALT cap was enacted to help pay for other TCJA tax breaks, and some lawmakers support the lower limit for funding purposes.

In the Senate, “there isn’t a high level of interest in doing anything on SALT,” Senate Majority Leader John Thune said June 15 on “Fox News Sunday.”

“I think at the end of the day, we’ll find a landing spot, hopefully that will get the votes that we need in the House, a compromise position on the SALT issue,” he said.

But some House Republicans have already pushed back on the proposed $10,000 SALT deduction cap included in the Senate draft.

Rep. Mike Lawler, R-N.Y., on Monday described the Senate proposed $10,000 SALT deduction limit as “DEAD ON ARRIVAL” in an X post.

Meanwhile, Rep. Nicole Malliotakis, R-N.Y., on Monday also posted about the $10,000 cap on X. She said the lower limit was “not only insulting but a slap in the face to the Republican districts that delivered our majority and trifecta.”

U.S. President Donald Trump looks on as Fed Chair Jerome Powell speaks at the White House in Washington on Nov. 2, 2017.

Carlos Barria | Reuters

Political pressure is mounting against the Federal Reserve Chair Jerome Powell, and yet the Federal Reserve is expected to hold interest rates steady at the end of its two-day meeting this week.

Despite a wave of recent attacks on Powell from President Donald Trump, futures market pricing is implying virtually no chance of an interest rate cut, according to the CME Group’s FedWatch gauge.

The president has argued that maintaining a fed funds rate that is too high makes it harder for businesses and consumers to borrow, adding more strain to the U.S. economy. The federal funds rate sets what banks charge each other for overnight lending, but also affects many of the borrowing and savings rates most Americans see every day.

More from Personal Finance:

Here’s the inflation breakdown for May 2025

What’s happening with unemployed Americans — in five charts

The economic cost of Trump, Harvard battle over student visas

With a rate cut likely postponed until at least September, consumers struggling under the weight of high prices and high borrowing costs aren’t getting much relief, experts say.

“The combination of high interest rates, stubborn inflation and economic uncertainty is a pretty challenging one,” said Matt Schulz, chief credit analyst at LendingTree. “Most Americans don’t have a ton of wiggle room and today they have even less.”

From credit cards and mortgage rates to auto loans and savings accounts, here’s a look at how the Fed plays a role in your finances.

Credit cards

Credit card debt continues to be a pain point for consumers struggling to keep up with high prices. Since most credit cards have a variable rate, there’s a direct connection to the Fed’s benchmark.

But even with the Fed on the sidelines, credit card rates have edged higher. The average annual percentage rate is currently just over 20%, according to Bankrate, not far from last year’s all-time high.

“This is a sign of banks trying to protect themselves from the risk that is out there in these uncertain times,” Schulz said. However, in this case, there is something consumers can do about higher APRs.

“The truth is that people have way more power over the rates they pay than they think they do, especially if they have good credit,” Schulz said.

Rather than wait for a rate cut that may be months away, borrowers could switch now to a zero-interest balance transfer credit card or consolidate and pay off high-interest credit cards with a lower-rate personal loan, he said.

Mortgages

Since 15- and 30-year mortgages are largely tied to Treasury yields and the economy, those rates haven’t moved much — and that hasn’t helped would-be buyers.

The average rate for a 30-year, fixed-rate mortgage has stayed within the same narrow range for months and is currently near 6.9%, according to Bankrate. Tack on the nationwide problem of limited inventory and housing affordability remains a key issue, regardless of the Fed’s next move.

“I don’t see any major changes coming in the immediate future, meaning that those shopping for a home this summer should expect rates to remain relatively high,” Schulz said.

Auto loans

Auto loan rates are fixed, and not directly tied to the Fed. But payments are getting bigger because car prices are rising, in part due to impacts from Trump’s trade policy.

Currently, the average rate on a five-year new car loan is 7.24%, according to Bankrate.

The growth in median car payments is outpacing both new and used car prices, according to separate data from Bank of America. Now, of those households with a monthly car payment, 20% pay more than $1,000 a month.

“Combine that with the potential for tariffs to drive auto prices even higher, and it adds up to a really challenging time to buy a car,” Schulz said. “However, shopping for the best rate and getting approved for financing before you ever set foot in the dealership can bring significant savings,” he added.

Student loans

Federal student loan rates are set once a year, based in part on the last 10-year Treasury note auction in May and fixed for the life of the loan, so most borrowers are somewhat shielded from Fed moves and recent economic turmoil.

Current interest rates on undergraduate federal student loans made through June 30 are at 6.53%. Starting July 1, the interest rates will be 6.39%.

Although borrowers with existing federal student debt balances won’t see their rates change, many are now facing other headwinds and fewer federal loan forgiveness options.

Savings

On the upside, top-yielding online savings accounts still offer above-average returns and currently pay more than 4%, according to Bankrate.

While the central bank has no direct influence on deposit rates, the yields tend to be correlated to changes in the target federal funds rate — so holding that rate unchanged has kept savings rates elevated, for now.

“The thing that is lost in this, is that savers, including millions of retirees, are actually earning good income on their savings, provided they have their money parked in a competitive place,” said Greg McBride, Bankrate’s chief financial analyst.

Senate Republicans release revised tax cuts and debt limit bill

Tax savings for business owners hiring kids

‘SALT’ deduction in limbo as Senate Republicans unveil tax plan

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Economics1 week ago

Economics1 week agoSending the National Guard to LA is not about stopping rioting

-

Blog Post1 week ago

Blog Post1 week agoMastering Bookkeeping Tasks During Peak Business Seasons

-

Accounting1 week ago

Accounting1 week agoInstead adds AI-driven tax reports

-

Personal Finance1 week ago

Personal Finance1 week agoWhat Pell Grant changes in Trump budget, House tax bill mean for students

-

Personal Finance6 days ago

Personal Finance6 days agoHow markets performed for investors so far

-

Economics6 days ago

Economics6 days agoIs there a “woke right” in America?

-

Personal Finance6 days ago

Personal Finance6 days agoTrump’s ‘big beautiful’ bill may curb access to low-income tax credit

-

Finance6 days ago

Finance6 days agoGundlach says to buy international stocks on dollar’s ‘secular decline’