Accounting

How will firms respond when AI agents reshape your firm’s business model?

Agentic AI holds much promise for the accounting profession. AI agents, defined as “software that is capable of at least some degree of autonomy to make decisions and interact with tools outside itself in order to achieve some sort of goal—whether booking a flight, sending a bill, or buying a gift—without constant human guidance” (by Chris Gaetano

Generative AI is already ushering in this change, and AI agents will take it to another level, fundamentally reshaping how firms win. Here are three ways AI agents will force a business model reckoning in accounting.

1. Death of the billable hour accelerates

The billable hour has been under scrutiny for years, but agentic AI will accelerate its demise at an unprecedented rate. Why? Because AI agents can scale 100 times faster than humans at a fraction of the labor costs, resulting in parallelized work for greater speed and efficiency. In this agentic AI world, the traditional time-and-materials billing model becomes increasingly nonsensical.

Imagine an army of AI agents that can:

- Generate many tax returns with reasonable “judgment” for initial reviews in the background, reducing the need for manual first-pass preparation;

- Reconcile financial statements instantly, identifying anomalies and inconsistencies with greater accuracy than a human who is manually doing this work;

- Draft audit reports overnight, improving speed and consistency without requiring overtime or additional staffing.

I cannot stress this enough: the firms that successfully transition to value-based pricing will be the winners in this new agentic AI economy. I hear of firms instituting technology fees or passing on specific software costs as a response to time saved in achieving an outcome. This is not enough if we want our profession to thrive.

True transformation requires a shift in how we define, price, and deliver value; it’s time to rip off the band-aid and do the hard work.

2. Current outsourcing models become obsolete

Outsourcing has been a great capacity expansion and cost-optimization solution for firms looking to grow and serve their clients well. Many times, outsourced roles focus on less complex and more deterministic work like reconciliations and tax prep and are managed by more senior accountants in the home office.

These are precisely the types of tasks AI agents will take over. As the agentic AI technology improves, firms will increasingly appreciate that AI agents don’t get sick, work 24/7 without burnout, can be quickly “onboarded” upon a firm-wide trained repository of data, and don’t leave for another job with higher pay. It is inevitable that agentic AI will eventually replace human-based outsourcing models as we know it, forcing firms to reallocate budgets and rethink staffing.

Outsourcing firms will not disappear overnight and there is still a great ROI to be gained from further investment today. However, over time, the nature of outsourcing will evolve dramatically. My many talented friends in the accounting outsourcing business are already aware of this shift and are actively working to redefine the value that outsourcing entities of the future can bring for firms.

3. Cost structures and workforce metrics transform

Nvidia CEO Jensen Huang said something clever at the CES show in January: “The IT department of every company is going to be the HR department of AI agents in the future.” He is pointing out the inevitable shift of firms who will soon be “hiring” AI agents alongside human employees.

Today, we judge the efficacy of engagements based on KPIs such as realization, utilization and bill rates. But in a world where AI agents execute on increasing portions of work alongside humans, how we measure profitability, cost structures and engagement performance will change.

Key shifts include:

- Human staff impact will be quantified differently, explicitly including their ability to manage AI agents for compensation considerations.

- Performance metrics will evolve—how do we measure AI agent vs. human staff performance, productivity and their direct contributions to success?

- IT budgets will increase as firms invest in AI agents to increase their “labor capacity.”

This transformation will require new benchmarking, financial models and internal engagement cost allocation between IT and HR.

How to prepare for the agentic AI world

The firms that win in this era of agentic AI will be those that take a proactive approach to business model evolution and rethink their approaches to value creation, talent management and financial modeling.

1. Transition to value-based pricing

The firms that wait too long to make this transition will struggle to justify their fees in an environment where AI agents dramatically reduce the time and cost required to deliver services. Key steps to take include:

- Identify high-value services that can be decoupled from time and materials billing.

- Educate clients on why they are paying for outcomes, not effort.

- Experiment with fixed-fee engagements where possible, ensuring pricing resilience in an AI-driven world.

- Incentivize teams based on client outcomes rather than hours logged.

2. Evolve your workforce strategy

The workforce of the future is hybrid—humans and AI agents working side by side. Firms that fail to adapt to this reality will overpay for human labor where AI could be leveraged or will fall behind competitors who optimize AI-human collaboration. Key steps to take include:

- Collaborate with outsourcing partners that are actively evolving their business models and technology capabilities alongside agentic AI developments.

- Create training programs in preparation for the agentic AI future.

3. Adjust cost structures and performance metrics

Firms that don’t rethink their profitability, cost allocation and engagement performance tracking will be flying blind in an agentic AI world. Key steps to take include:

- Redefine staff performance impact—factor in how well human staff work with technology and AI in performance and compensation models.

- Treat AI investments as labor-expanding strategies, not just tech expenses.

- Update engagement profitability models to incorporate AI-driven workstreams alongside human contributions.

AI agents are no longer a far-off concept. While they are not quite ready for prime time for a mainstream CPA audience, they are here and slowly but surely changing the accounting profession. Firms that embrace these changes with strategic intent will thrive in the agentic AI economy.

Enjoy complimentary access to top ideas and insights — selected by our editors.

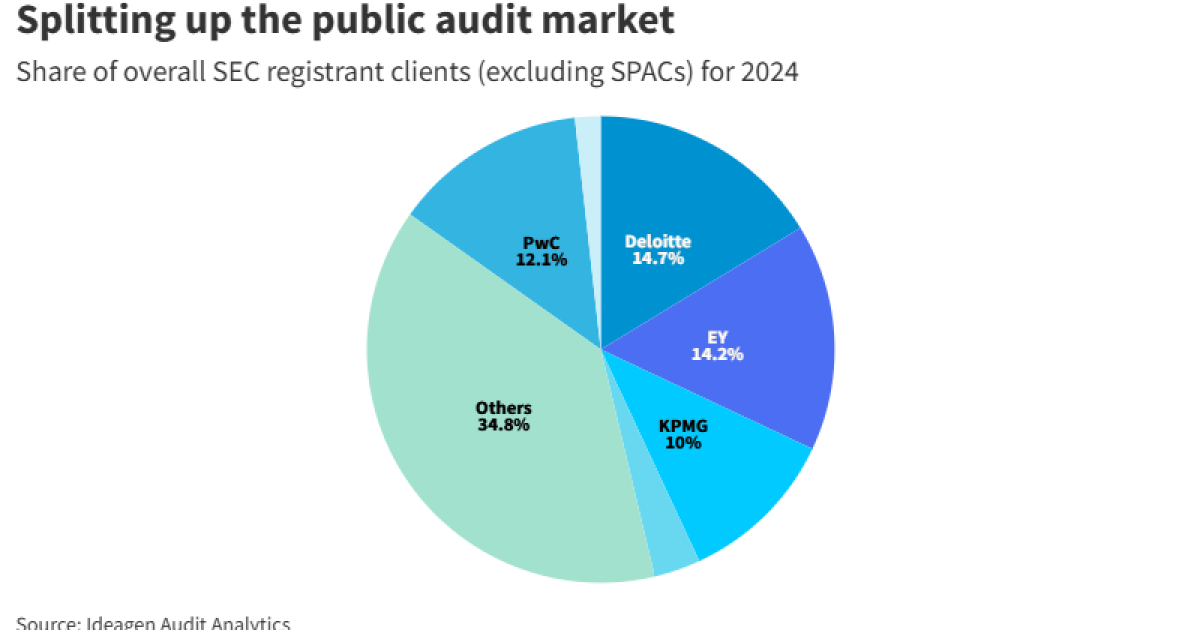

This week’s stats focus in part on the Securities and Exchange Commission audit client market, with overall market share for the largest firms, the overall number of new SEC audit clients, and top firms for new audit clients by quarter; as well as the number of accounting-related securities class actions; the amount of federal taxes paid by unauthorized immigrants in 2023; and the amount of federal debt per taxpayer.

Lack of awareness, fear of mistakes and penalties, and the cost of filing are preventing many families from claiming millions of dollars in tax credits, according to a new study.

The

Awareness gaps were a big barrier. Among households earning under $10,000 annually, 36% were unaware of any tax credits, more than double the rate among households earning over $150,000 (17%).

Misunderstanding their eligibility also kept many taxpayers from filing their annual returns. One-third of lower-income households earning under $26,000 who hadn’t filed taxes in the past three years said they didn’t file because they believed their income was too low. But within this group, 20% had earned income and 37% had children — factors that probably would have made them eligible for claiming the tax credits if they had filed.

Fear of making a mistake and being penalized for it was the most common barrier to filing a return, particularly among lower-income households. This fear had major consequences, as 61% of respondents who felt this way hadn’t filed tax returns in the past three years, and even when they did file, they were more likely to miss out on tax credits.

Filing a tax return can be expensive for families, forcing them to forgo other expenses in order to file. Even though 36% of survey respondents cited cost as a barrier, most had used professional tax help at some point due to concerns around navigating the process alone.

Accessing the right documents poses a challenge for taxpayers. Half of the survey respondents said they had trouble gathering the documents they needed to file their taxes, and 80% of those who faced documentation issues struggled with more than one type of document.

Most low-income households are already connected with other types of government support services, but tax credits feel like a separate disconnected area. The survey found 84% of households who had not filed taxes at all or irregularly in the past three years had participated in at least one other public support service during that same time period.

“Accessing tax credits is often overwhelming and costly, creating unnecessary barriers for the families who need this support the most,” said Devyani Singh, lead author of the report, in a statement. “Tax credits can be a critical lifeline for families that are struggling financially, and it’s up to state Departments of Revenue to look at the process as a delivery issue. There’s no one-size-fits-all solution to increasing tax credit uptake; improving access requires a multipronged strategy combining personalized outreach, streamlined systems, and policies that meet families where they are.”

The report pointed out that such factors are important for government agencies to consider, especially as the White House and some lawmakers in Congress express interest in increasing the amount families can get from the Child Tax Credit. However, the proposed shuttering of free tax-filing programs like Direct File, which

The Senate Finance Committee questioned Billy Young, President Trump’s nominee for Internal Revenue Service commissioner, about his plans for the beleaguered agency and promotion of dubious “tribal tax credits” and Employee Retention Tax Credits during a long-awaited confirmation hearing Tuesday after a series of acting commissioners temporarily held the role.

Trump

Long insisted during the confirmation hearing that he would defend the integrity of the IRS and maintain an open door policy, emulating the example of former commissioner Charles Rossotti, who served from 1997 to 2002.

“If confirmed, I will implement a comprehensive plan aimed at enhancing the IRS, but also one that develops a new culture at the agency,” he said in his opening statement. “I am eager to implement the necessary changes to maximize our effectiveness, while also remaining transparent with both Congress and taxpayers. It is important to also recognize the dedicated professionals currently at the IRS whose hard work too often goes unnoticed. It is my pledge that we will invest in retaining skilled members of the team. This does not mean a bloated agency, but an efficient one where employees have the tools they need to succeed.”

Committee chairman Mike Crapo, R-Idaho, expects to see changes at the agency. “Congressman Long is very clear that he will make himself available to all IRS employees, no matter their seniority,” Crapo said in his opening statement. “Moreover, he wants to implement a top-down culture change at the agency. This sea change will benefit American taxpayers, who too often view the IRS as foe, rather than friend. Congressman Long knows, from years of experience in the House, that to be a successful Commissioner, he must be a valuable partner in Congress’ efforts to ensure that new tax legislation is implemented and administered as Congress intends it to be. I am also confident that he will be fully transparent and responsive to Congress and the American people.”

Sen. Ron Wyden, D-Oregon, the top Democrat on the committee, questioned Long about his promotion of “tribal tax credits” and the fraud-plagued ERTC. “Most of Congressman Long’s experience with tax issues came after he left Congress, when he dove headlong into the tax scam industry,” he said in his opening statement. “Cashing in on the credibility of his election certificates, he raked in referral fees steering clients to firms that sold faked tax shelters and pushing small businesses to unknowingly commit tax fraud.”

Wyden asked Long about the $65,000 he earned from referring friends to tax promoters who claimed they had acquired income tax credits issued to a Native American tribe and then sold the tax credits to investors. “There’s a problem. The IRS said in March that the credits do not exist. They’re fake. They are a scam. Now you’re asking to be put in charge of the IRS, and the IRS confirms that these aren’t real. Tell the committee, do you believe these so-called tribal tax credits actually exist?”

Long insisted his only involvement with the credit was to connect interested friends and offer to put them on a Zoom call with someone, but he was not on the Zoom calls himself. Wyden pressed him on whether the tax credits actually exist.

“I think the jury’s still out on that,” Long admitted. “I know since 2022 they’ve been accepting them, so now they claim that they’re not. I think that all this is going to play out, and I want to have it investigated, just as you do. I know you’re very interested in this subject. I am too.”

Wyden also asked about

Wyden then asked him about his work with promoters of the Employee Retention Tax Credit. “You stated on a YouTube video that everybody qualifies for the Employee Retention Tax Credit, and you urge listeners to ignore CPAs that said they didn’t qualify. Do you really think everybody qualifies?”

“If you listen to that video, I hate to correct you, but I didn’t say everyone qualifies,” Long responded. “I said virtually everyone qualifies, meaning most people.”

Sen. Elizabeth Warren, D-Massachusetts, and other Democrats also questioned Long about whether he would follow Trump’s orders to audit certain taxpayers or remove the tax-exempt status of organizations, even if it violated the law. Long insisted he would follow the law but declined to explicitly say whether he would defy an order from Trump.

“I don’t intend to let anybody direct me to start an audit for political reasons,” he said.

Accountants on class actions, SEC audit clients and more

Misunderstandings keep families from claiming tax credits

Stocks making the biggest moves after hours: Palo Alto Networks, Take-Two Interactive and more

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Economics1 week ago

Economics1 week agoCPI inflation April 2025: Rate hits 2.3%

-

Economics1 week ago

Economics1 week agoTariff receipts topped $16 billion in April, a record that helped cut the budget deficit

-

Personal Finance7 days ago

Personal Finance7 days agoHouse Republicans advance Trump’s tax bill. ‘SALT’ deduction in limbo

-

Economics6 days ago

Economics6 days agoViolent crime is falling rapidly across America

-

Personal Finance1 week ago

Personal Finance1 week agoFidelity technical issues kept some investors out of their accounts

-

Economics1 week ago

Economics1 week agoGerman business leaders tell new government: It’s time to deliver

-

Economics5 days ago

Economics5 days agoThe low-end consumer is about to feel the pinch as Trump restarts student loan collections

-

Personal Finance1 week ago

Personal Finance1 week agoHow to save on groceries amid food price inflation