Accounting

Morningstar rates 529 savings plans

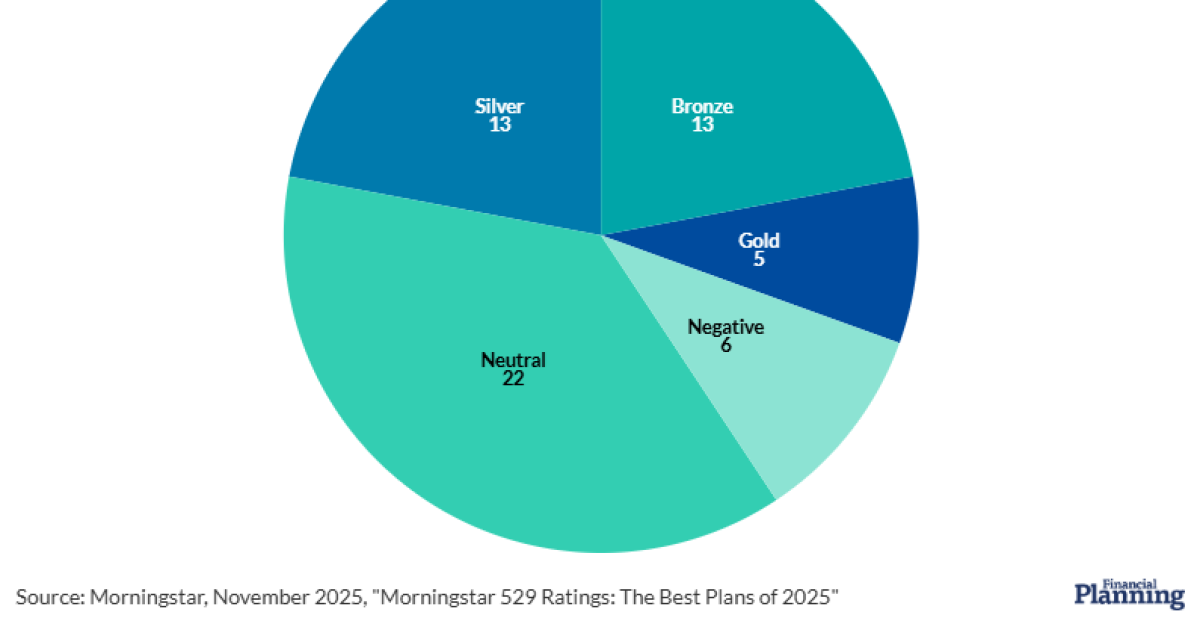

Very few 529 plans earned Morningstar’s top rating for investment quality, management, oversight and fees — but the tax savings are the X factor in educational investment accounts.

Just 31 out of 59 savings plans for college and other educational expenses rated “gold,” “silver” or “bronze” ratings from the research firm. But the seemingly poor showing belies general improvements among 529 providers since Morningstar began evaluating them 12 years ago, according to

Predominantly “meh” grades for the 529 plans came as no shock to Dinon Hughes, a partner at Portsmouth, New Hampshire-based registered investment advisory firm Nvest Financial and a member of this year’s class of

The plans themselves are “not that differentiated” from one another, beyond variation in tax-break structure by state and whether a wealth management firm has a selling agreement with certain providers that may limit a client’s options, Hughes noted.

“It’s worked for many plans for decades and decades and decades,” he said. “At their essence, all of them really offer the same things.”

READ MORE:

Investor demand for 529 plans

And that has proved appealing to many savers, to the tune of nearly 17 million 529 plan accounts with $525 billion in assets at the end of last year — an average of $30,961 per saver, according to the National Association of State Treasurers’ College Savings Plans Network, an advocacy group for state plan administrators.

Those numbers will likely grow alongside the rising cost of college, clients’ desire to avoid student loan debt and expansions of the 529 plan tax benefits

State taxes “should be the first consideration for most people” when thinking about 529 plans, according to Morningstar’s analysis, which included links to other guides about how to

Outside the tax impact, the 529 plans sold through advisors “tend to offer more actively managed strategies and niche exposures for a higher cost,” compared to the direct accounts with typically “smaller menus, more index funds and lower price tags,” Kim wrote in the report. The top-performing plans in Morningstar’s study offered lower fees than peers as well as allocations from thorough research, investment teams with substantial resources, long tenures and rigorous selection processes and “stable and engaged oversight from the state,” she wrote.

“If your state offers generous tax advantages and highly rated plans, you likely have an easy choice to make,” Kim wrote. “If your state does not offer (good) tax benefits and your state-sponsored plans earn a Morningstar Medalist Rating of ‘neutral’ or ‘negative,’ you are likely better served by a different state’s 529 plan. If your state offers generous tax benefits but lackluster plans, you should do a cost-benefit analysis of what it means to invest in the state versus out of state. Tax benefits are more certain than future returns.”

READ MORE:

Grading 529s and other savings methods

Despite the lackluster grades across this channel of asset management, Morningstar reported that the general trends in the past dozen years or so have worked in investors’ favor.

“Since Morningstar began rating 529 education savings plans in 2012, an increasing number of plans have adopted some or more of the positive attributes described in our methodology,” Kim wrote. “Asset managers no longer consider education savings plans as an afterthought to their existing multi-asset offerings; instead, we see an increasing dedication of research and resources to specifically help education savers. Stewardship standards continue to rise as well. Robust interaction between the state and its investment entity forms a baseline now, with more engaged state entities aggressively negotiating with external managers and advocating for their accountholders.”

When clients or prospective customers ask Hughes about 529 plans, he advises them to weigh the tax benefits and the investment options against the fees and rules for the use of the holdings in the future, he noted. But more savers are considering alternative options

“‘Hey, I don’t know if my kid’s going to college — I don’t know if I want to do that, and I don’t know if they’re going to want to do that,'” Hughes said some investors are telling him. “We’ve been having those types of conversations with parents who want to set something aside for their kids but might not want the 529 route.”

UK Has a New Prime Minister Without a General Election

Adaptive Governance in Volatile Markets

Navigating Sovereign Data Residency Mandates in the Age of AI

Armanino adds Strategic Accounting Outsourced Solutions

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

Tax Strategy: Employee Retention Credit update

-

Economics4 days ago

Economics4 days agoGlobal Trade Realignment and Supply Chains in 2026

-

Economics5 days ago

Economics5 days agoThe Warsh Shift: How the New Fed Chair Is Balancing War Drags and Tech Winds

-

Economics4 days ago

Economics4 days agoLabor Market Calibration: Analyzing the Shift Toward Skill-Based Allocation in 2026

-

Finance6 days ago

Finance6 days agoSouth Korea Raises Interest Rates to 2.75% for the First Time in More Than Three Years

-

Leaders6 days ago

Leaders6 days agoBerkshire Hathaway Chairman Reshapes His Long-Term Philanthropic Strategy

-

Finance4 days ago

Finance4 days agoTokenized Real-World Assets: Institutional Ledger Adoption Achieves Scale in July 2026

-

Economics6 days ago

Economics6 days agoGlobal Stock Market Weekly Recap: Tech Sell-Off Sparks International Rout

-

Accounting4 days ago

Accounting4 days agoStandardizing Global ESG Reporting: Key Compliance Imperatives for Mid-Year 2026