Accounting

Take comfort in gradual change in an era of audit upheaval

There is a saying that has been going through my mind of late: “May you live in interesting times.” Its origin is vague but many attribute it to a translation of a Chinese curse. Indeed, while the saying sounds like a blessing, it is more likely that wishing someone a life of interesting times is cursing them to a life of upheaval and conflict.

Whether you are optimistic, neutral or pessimistic about the current state of affairs, it’s safe to say we are all living in interesting times. Disruption has become a way of life in the 21st century. Consider this: In just the past five years we have experienced a global pandemic, geopolitical instability driven by wars in Ukraine and Gaza, intensifying natural disasters fueled by climate change, and technology disruptions brought on by artificial intelligence. Presently, we are all trying to decipher what will happen next with tariffs and their impacts on financial markets, which of late are behaving more like amusement park thrill rides than reflections of economic conditions.

I have written extensively about how today’s business leaders must learn to not only manage disruptive change but embrace it. In the second edition of my book,

However, I ran across a couple of interesting data points tucked into the latest

The Pulse data, which is gleaned from a survey of internal audit leaders across North America and Canada, show we’ve reached the inflection point in the generational transition. At 58%, Generation X (1965-1980) still makes up the lion’s share of chief audit executives, but the percentage of audit leaders who are millennials (1981-1996) now matches those who are baby boomers (1946-1964) at 21%.

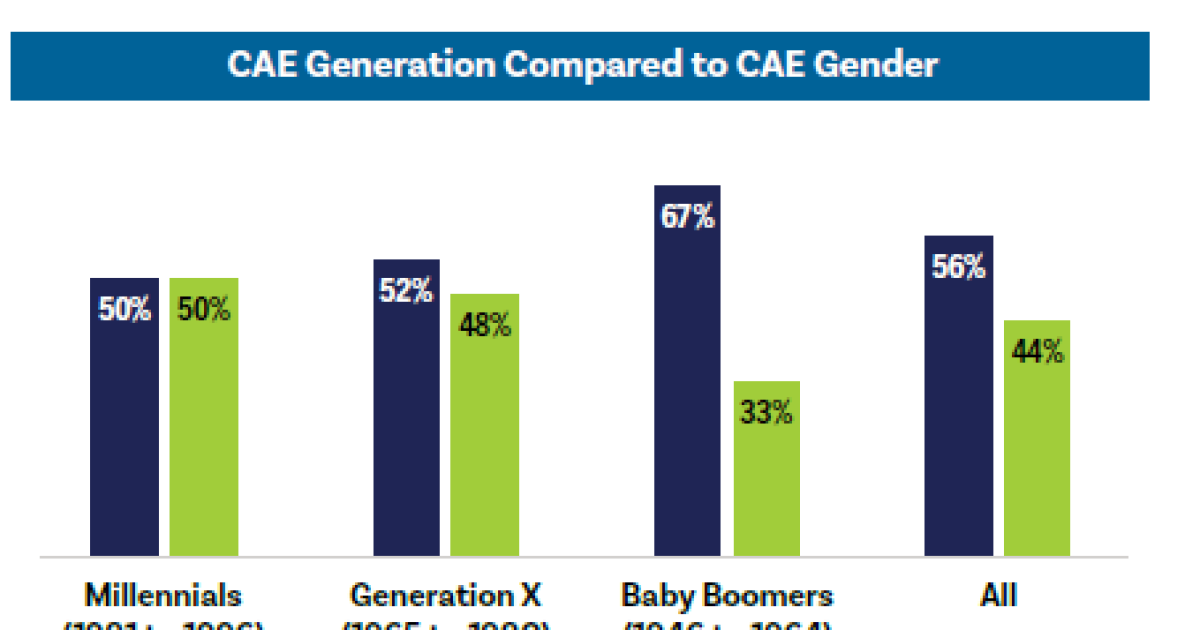

This clearly reflects the passing of the torch, because the numbers will continue to skew toward a younger generation of internal audit leaders with each passing year. I’ll explore what that means in a moment, but I also want to mention a second significant data point. The Pulse reports that women represent 44% of CAEs in North America overall, and a breakdown by age group shows the figure is significantly higher for audit leaders under 40.

The changing CAE gender profile

When I began my career in internal auditing in 1975, a woman leading an audit function was rare. However, over time pioneering women leaders emerged, including Carmen LaPointe, Betty McPhilimy and Patty Miller, each of whom went on to serve as IIA global board chairs. Since then, the IIA has had several other women lead the board including Angela Witzany, Jenitha Jones, Sally-Anne Pitt and current chairman Terry Grafenstine. The profession approaching true gender balance in leadership is something in which all internal audit practitioners should take great pride. Unlike generational change in leadership, gender equality is not inevitable.

When we dive deeper into the data, the true significance of the progress toward gender equality emerges. Baby boomers continue to skew the data toward males, where they make up two-thirds of CAEs born between 1946 and 1964. However, the gap closes significantly among Gen Xers (1965-1980) where women make up 48% of CAEs and comes to 50/50 parity among millennials (1981-1996).

A quick analysis of gender breakdown by industry finds women are making solid progress in other areas, as well. But we’d be hard pressed to find one where half of the leaders are women.

- Medical/health – 43%

- Education, consumer services and government – 40%

Women still lag significantly in leadership roles in:

- Food and beverage – 30%

- Transportation/logistics/supply chain, and automotive – 19%

- Aerospace/defense – 18%

- Agriculture – 17%

- Oil/gas/mining – 16%

It’s also encouraging to see the rapid pace at which women are ascending to leadership roles within the profession. We have available data from the IIA’s 2015 CBOK report, which provides a touchpoint. The report, which was based on a 2014-15 global survey of audit practitioners, found women held 31% of CAE positions globally and 39% in North America. In just 10 years, the percentage of female North American CAEs grew 5%.

Generational changes

Moving to the proverbial changing of the guard, the parity between baby boom and millennial internal audit leaders was inevitable as older CAEs leave the workforce. Of significance here is the timing. When I first saw the data, I thought to myself, “Whew, just in the nick of time.” Allow me to elaborate.

At the risk of generalizing, millennials bring to the table technology skills, views about work-life balance, and preferences in communication styles, creativity and diversity that are more suited to 21st century challenges. To be sure, baby boomer optimism, work ethic, loyalty and focus on teamwork helped found and build some of the greatest organizations the world has ever seen, including Microsoft, Apple, Nvidia, Amazon, Virgin Atlantic and others. Baby boomers also forged the digital foundation on which millennials will build the future.

However, the demands created by a world in near-constant upheaval require greater flexibility, agility, resilience and innovation that millennial characteristics are more likely to provide. It’s more than millennials being technologically adept. For example, millennials use digital tools for quick communication that support agility and flexibility, while boomers are more likely to prefer formal meetings and written communication.

There is little doubt that both generations share a desire for success and achievement, but their approaches and values differ significantly, reflecting the evolving social and economic landscape of their times.

From an internal audit perspective, greater numbers of millennial CAEs will invariably accelerate the long-overdue widespread adoption of technology among internal audit functions. What’s more, their communications styles, creativity and embracing of diversity will help position the profession to support organizations that are flexible, resilient, agile and, most importantly, built to succeed in interesting times.

House Republicans narrowly

The legislation now heads to the Senate where lawmakers are looking to make their own stamp on the bill. The core of the package — an extension of the president’s 2017 first-term tax cuts — is likely to stay, but the senators could make some changes to a slew of new tax and spending measures that touch many aspects of the economy.

Here’s a rundown of the House bill’s main provisions impacting people and businesses:

$40,000 SALT limit

The limit on

The bill also separately creates a new limit on the value of itemized deductions for those in the top 37% tax bracket that partly erodes the value of the new SALT cap.

Tips, overtime and autos

Tips and overtime pay would be exempt from income tax through 2028, the end of Trump’s second term, fulfilling — at least for four years — his

Medicaid

The bill would accelerate new Medicaid work requirements to December 2026 from 2029 in a gesture to satisfy ultraconservatives who wanted more spending cuts.

The December 2026 deadline would fall just one month after midterm elections, with Democrats eager to criticize Republicans for

Food stamps

The bill aims to save $300 billion by forcing states to pay more into the Supplemental Nutrition Assistance Program. It would also apply work requirements for longer. Beneficiaries must work through age 64, up from 54 under current law.

Interest expensing

Private equity and other heavily indebted business sectors won a major fight in the tax bill on interest expensing. The bill adds depreciation and amortization when determining the tax deductibility of a company’s debt payments. The maximum amount any company can get in such tax write-offs is calculated as a percentage of earnings. That’s why using EBITDA – which is typically bigger than EBIT — in this process would generate heftier tax deductions.

University endowment tax

Some private universities would face a

The provision would create a tiered system of taxation so that colleges and universities that meet a threshold based on the number of students would pay more. Under Trump’s 2017 tax law, some colleges with the most well-funded endowments currently pay a 1.4% tax on their net investment income. The levy would rise to as high as 21% on institutions with the largest endowments based on their student population.

The provision is a major escalation in Trump’s fight with Harvard and other elite colleges and universities, which he has sought to strong-arm into making curriculum and cultural changes that he favors. Harvard, Yale, Stanford, Princeton and MIT would face the

Private foundation tax

Private foundations also would face an

Sports teams

The bill would limit write-offs for professional football, basketball, baseball, hockey and soccer franchises that claim deductions connected to the team’s intangible assets, including copyright, patents or designs.

Electric vehicles

A popular consumer tax credit of up to $7,500 for the purchase of an electric vehicle would be fully eliminated by the end of 2026, and only manufacturers that have sold fewer than 200,000 electric vehicles by the end of this year would be eligible to receive it in 2026. Tax incentives for the purchase of commercial electric vehicles and used electric vehicles would also be repealed.

Renewable tax credits

The legislation would cut hundreds of billions of dollars in spending by

It would also hasten more stringent restrictions that would disqualify any project deemed to benefit China from receiving credits. Those limits, which some analysts have said could render the credits useless for many projects, would kick in next year.

The legislation would also extend through 2031 tax credits for the production of biofuels.

Bonus for elderly

Americans 65 and older who don’t itemize their taxes would get a $4,000 bonus added to their standard deduction through 2028. That benefit would phase out for individuals making more than $75,000 and couples making more than $150,000. It would be retroactive to the beginning of this year.

Trump had campaigned on ending taxes on Social Security benefits, but that proposal would have run afoul of a special procedure Republicans are using to push through the tax-law changes without any Democratic votes. The higher standard deduction is an alternative way of targeting a benefit to the elderly but doesn’t fully offset Social Security taxes paid by many seniors.

Targeting immigrants

Immigrants would face a new 3.5% tax on

Factory incentives

The bill does not include Trump’s call for a lower corporate tax rate for domestic producers. Instead, it allows 100% depreciation for any new “qualified production property,” like a factory, if construction begins during Trump’s term — beginning on Jan. 20 and before Jan. 1, 2029, and becomes operational before 2033. That would be a major incentive for new facilities as Trump

Child tax credit

The maximum child tax credit would rise to $2,500 from $2,000 through 2028 and then drop to $2,000 in subsequent years.

Trump Accounts

The bill would create new tax-exempt investment accounts to benefit children, dubbed Trump Accounts. An earlier version of the bill called them

Pass-through deduction

Owners of pass-through businesses would be allowed to exclude 23% of their business income when calculating their taxes, a 3-percentage-point increase from the current rate. The increase is a win for pass-through firms — partnerships, sole proprietorships and S corporations — which make up the vast majority of businesses in the US.

Research and development

The bill would temporarily reinstate a tax deduction for research and development, a top priority for manufacturers and the tech industry. The deduction will last through the end of 2029.

Oil, gas and coal

The bill would raise billions by mandating the Interior Department hold at least 30 oil and gas lease sales over 15 years in the Gulf of Mexico, which Trump ordered to be renamed to the Gulf of America. It would withdraw Biden-era restrictions on development in Alaska’s Arctic National Wildlife Refuge. The measure would also mandate at least six offshore lease sales in Alaska’s Cook Inlet region over six years. The legislation would also require Interior to offer at least four million acres of coal resources for lease in the West within 90 days of enactment.

Radio spectrum

The legislation would restore the Federal Communications Commission’s ability for the next decade to

New spending

The bill would allocate $150 billion for the military and $175 billion for immigration and border security.

Trump greenlights Nippon merger with US Steel

Deferred capital gains tax on mutual funds: Lawmakers pitch rule change

Stocks making the biggest moves midday: AAPL, ROST, INTU, BAH

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Personal Finance1 week ago

Personal Finance1 week agoHouse Republicans advance Trump’s tax bill. ‘SALT’ deduction in limbo

-

Economics1 week ago

Economics1 week agoThe low-end consumer is about to feel the pinch as Trump restarts student loan collections

-

Economics1 week ago

Economics1 week agoViolent crime is falling rapidly across America

-

Economics1 week ago

Economics1 week agoAre American Catholics ready for an American pope?

-

Economics1 week ago

Economics1 week agoEmbrace the woo woo

-

Blog Post6 days ago

Blog Post6 days agoBest Practices to Auditing Your Bookkeeping Records

-

Economics1 week ago

Economics1 week agoConsumer sentiment falls in May as Americans’ inflation expectations jump after tariffs

-

Economics1 week ago

Economics1 week agoJPMorgan Chase CEO Jamie Dimon says recession is still on the table for U.S.