Accounting

To PE, or not to PE, is that the question?

Many small and midsize firms are seeking a sounding board for the myriad calls they are getting from private equity firms and others seeking to acquire accounting practices. They’re exhausted. And the ongoing barrage continues to add pressure for firms to make a call on whether or not they should “go PE.”

There are benefits to upgrading aspects of public accounting with an infusion of profit-oriented owners instituting goals, accountability and growth drivers. However, each firm would do itself, and the profession, the best service by reflecting thoughtfully about the options at hand.

Before seeing “Should we go with private equity?” as the question, firms should step back and review their specific strategy and position. Maybe whether to go PE is still a possibility, but only after they’ve answered preliminary questions that would drive them to consider private equity.

What does a firm need to know to determine its interest, or not, in PE (or another external capital partner)?

10 critical questions for CPAs

- How do you measure success (profitability/financial reward, client service, internal culture, lifestyle, professional contributions, community contributions, among others)? It’s OK to measure success differently than your peers or industry benchmarks.

- How satisfied are you with your firm’s success? Rate each success area you identified above.

- How confident do you feel in your ability to continue your success (1) during your career, and (2) for the ongoing legacy of your firm (after you’ve retired and been paid out)? Note: Many firms feel confident enough in continuing at a rate that meets their needs, whether they are above or below traditional or industry benchmark measures of success. This is a fine place to be, and “not to PE.”

- How much preference do you have for autonomy in strategy and decision making versus having additional leadership and influences in these areas?

- How much preference do you have for continuing to champion industry trends and challenges, such as recruiting and technology/AI, with your current or projected internal resources?

- How much preference do you have for continuing to do the ongoing work related to back-office operations like billing, collections and firm administration?

- Do you have the internal leadership talent and culture of accountability to reach your goals?

- If you could have more profitability and resources along with the involvement of outside capital and influence, would you want that arrangement?

- If outside capital and influence are of interest to your firm, should you look at the pros and cons of mergers (equal or up), ESOPs, family office capital or others in addition to PE?

- What are the pros and cons of each option as it relates to the impact on your success measures identified above?

Much like a choose-your-own-adventure story, the answer to each of the 10 questions above doesn’t always lead where you might expect. You may find that PE is clearly the best choice for your firm. You may find that an ESOP is very attractive, or that selling to a larger CPA firm would be the best fit for your team and clients. You may feel more confused than ever. You may find that you remain content with your partnership-model firm, just as you were before.

Here are a few vignettes from firms I’ve talked with recently, and which options they are considering:

In one case, a $5 million firm wants to take a new step forward, something other than “what we’ve done” to propel it to future success. The partners want to continue to develop their next generation, allow current (not-quite-retirement-age) partners more opportunities, either via ongoing client service and less admin, or by moving from a client service role to an M&A role seeking out acquisitions for growth.

It’s likely this firm’s leaders would feel satisfied with their success but have some concern about their ability to continue it, especially in the realm of recruiting and the administrative work required to operate a CPA firm. They are interested in pursuing PE to expand their options and seek a secure future for retirees, partners, staff and clients.

In another case, an $8 million firm is content with its $600,000 average income per partner, and sufficient talent pipeline, including newer partners to replace upcoming retirements. The partners share a desire to keep buyouts at a reasonable price to allow newer partners similar current income success as earlier partners. They feel confident their in-house decision-making and governance will perpetuate the investments, profits, culture and client service they have enjoyed to date.

It’s likely this firm’s partners would feel satisfied with their success and are content with their leadership group’s abilities and capacity to continue it. They are interested in staying independent to continue the legacy, including autonomous decision-making and profits that they’ve built to date.

Making a decision

Along with those firms that know which option they would choose, many are in the land of uncertainty. For this I recommend continuing your quest to learn more about various options, engaging in a deeper strategic planning process and ultimately making a call, even if it’s for a limited timeframe, like six months, at which point you can revisit.

Decision-making will allow you to move on with your goals and objectives and know clearly whether you should pick up that next inbound call offering the riches of capital or continue to champion the business you’ve already built.

IT auditors who know a lot about artificial intelligence can now show it through a new certification, as the

The credential requires knowledge of a wide range of AI-related audit skills, proven through an exam scheduled through ISACA. Only those with an active CISA from ISACA, CIA from the IIA, and CPA from the AICPA are eligible to pursue the AAIA, which covers the key domains of AI governance and risk, AI operations, AI auditing tools and techniques.

Chiefly, professionals must demonstrate “AI operations” skills that concern balancing sustainability, operational readiness and the risk profile with the benefits and innovation AI promises to support enterprise-wide adoption of this powerful technology. This includes AI-specific data management, AI solution lifecycle management, AI-specific change management, supervision of AI solutions (especially agents), testing techniques for AI solutions, AI-specific threats and vulnerabilities, and AI-specific incidence response management.

The next largest area of focus is “AI governance and risk,” which is mainly concerned with advising stakeholders on implementing AI solutions through appropriate and effective policy, risk controls, data governance and ethical standards. This encompasses general knowledge of AI and its business impacts, AI governance and program management, AI risk management, data and data governance programs, and how AI fits into standards frameworks and professional ethics.

After that is “AI auditing tools and techniques,” which focuses on optimizing audit outcomes for innovation and highlights the professional’s knowledge of audit techniques tailored to AI systems and the use of AI-enabled tools to streamline audit efficiency and provide faster, quality insights. This includes audit planning and design, testing and sampling methodologies, evidence collection techniques, data quality and analytics, outputs and reports, all specific to AI.

There are a number of task-based secondary classifications, such as “utilize AI solutions to enhance audit processes, including planning, execution and reporting” and “evaluate algorithms and models to ensure AI solutions are aligned to business objectives, policies and procedures.”

“ISACA is proud to have served the global audit community for more than 55 years through our audit and assurance standards, frameworks and certifications, and we are continuing to help the community evolve and thrive with the certifications and training they need in this new era of audits involving AI,” said Shannon Donahue, ISACA chief content and publishing officer. “Through AAIA, auditors can demonstrate their expertise and trusted advisory skills in navigating AI-driven challenges while upholding the highest industry standards.”

As AI becomes increasingly integrated into the world economy, a number of standard-setting and certification bodies have responded to rising concerns about the impact the technology can have on business and the economy as a whole. The National Institute of Standards and Technology released its

Enjoy complimentary access to top ideas and insights — selected by our editors.

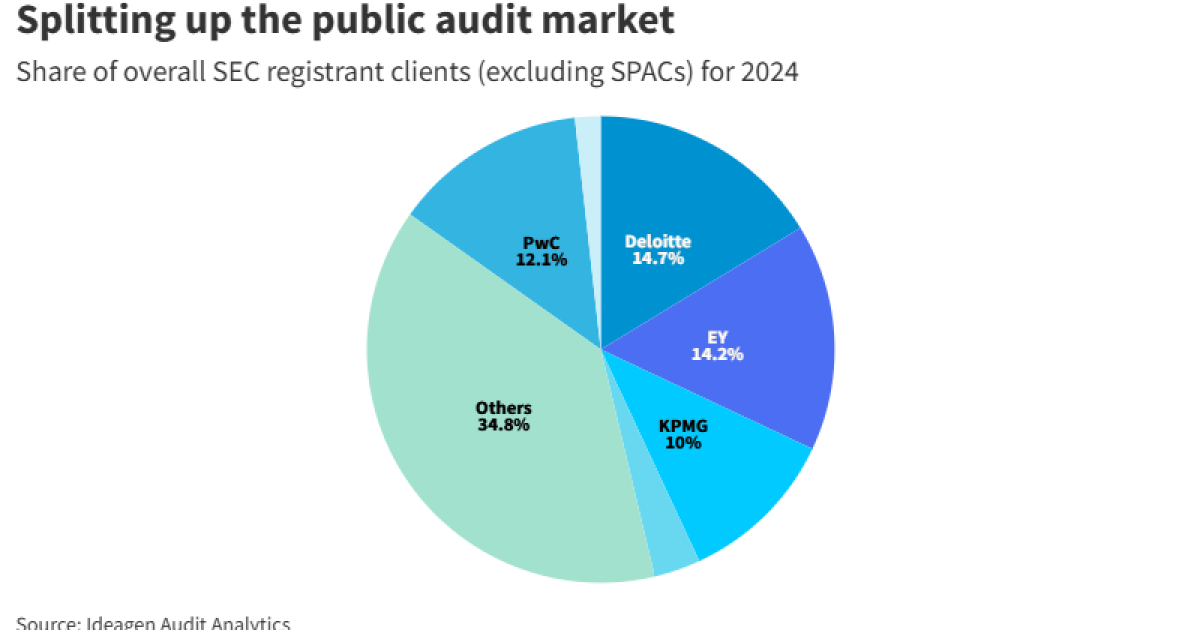

This week’s stats focus in part on the Securities and Exchange Commission audit client market, with overall market share for the largest firms, the overall number of new SEC audit clients, and top firms for new audit clients by quarter; as well as the number of accounting-related securities class actions; the amount of federal taxes paid by unauthorized immigrants in 2023; and the amount of federal debt per taxpayer.

Lack of awareness, fear of mistakes and penalties, and the cost of filing are preventing many families from claiming millions of dollars in tax credits, according to a new study.

The

Awareness gaps were a big barrier. Among households earning under $10,000 annually, 36% were unaware of any tax credits, more than double the rate among households earning over $150,000 (17%).

Misunderstanding their eligibility also kept many taxpayers from filing their annual returns. One-third of lower-income households earning under $26,000 who hadn’t filed taxes in the past three years said they didn’t file because they believed their income was too low. But within this group, 20% had earned income and 37% had children — factors that probably would have made them eligible for claiming the tax credits if they had filed.

Fear of making a mistake and being penalized for it was the most common barrier to filing a return, particularly among lower-income households. This fear had major consequences, as 61% of respondents who felt this way hadn’t filed tax returns in the past three years, and even when they did file, they were more likely to miss out on tax credits.

Filing a tax return can be expensive for families, forcing them to forgo other expenses in order to file. Even though 36% of survey respondents cited cost as a barrier, most had used professional tax help at some point due to concerns around navigating the process alone.

Accessing the right documents poses a challenge for taxpayers. Half of the survey respondents said they had trouble gathering the documents they needed to file their taxes, and 80% of those who faced documentation issues struggled with more than one type of document.

Most low-income households are already connected with other types of government support services, but tax credits feel like a separate disconnected area. The survey found 84% of households who had not filed taxes at all or irregularly in the past three years had participated in at least one other public support service during that same time period.

“Accessing tax credits is often overwhelming and costly, creating unnecessary barriers for the families who need this support the most,” said Devyani Singh, lead author of the report, in a statement. “Tax credits can be a critical lifeline for families that are struggling financially, and it’s up to state Departments of Revenue to look at the process as a delivery issue. There’s no one-size-fits-all solution to increasing tax credit uptake; improving access requires a multipronged strategy combining personalized outreach, streamlined systems, and policies that meet families where they are.”

The report pointed out that such factors are important for government agencies to consider, especially as the White House and some lawmakers in Congress express interest in increasing the amount families can get from the Child Tax Credit. However, the proposed shuttering of free tax-filing programs like Direct File, which

ISACA offers AI audit credential

Stocks making the biggest moves premarket: TGT, PANW, LOW, UNH

Accountants on class actions, SEC audit clients and more

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Economics1 week ago

Economics1 week agoCPI inflation April 2025: Rate hits 2.3%

-

Economics1 week ago

Economics1 week agoTariff receipts topped $16 billion in April, a record that helped cut the budget deficit

-

Personal Finance1 week ago

Personal Finance1 week agoHouse Republicans advance Trump’s tax bill. ‘SALT’ deduction in limbo

-

Economics6 days ago

Economics6 days agoViolent crime is falling rapidly across America

-

Personal Finance1 week ago

Personal Finance1 week agoFidelity technical issues kept some investors out of their accounts

-

Economics1 week ago

Economics1 week agoGerman business leaders tell new government: It’s time to deliver

-

Economics5 days ago

Economics5 days agoThe low-end consumer is about to feel the pinch as Trump restarts student loan collections

-

Personal Finance1 week ago

Personal Finance1 week agoHow to save on groceries amid food price inflation