The American workplace’s experiment with remote work happened, effectively, overnight: With the onset of the pandemic in March 2020, more than half of workers began working from home at least part of the time, according to Gallup. But the shift to a permanent hybrid-work reality has been gradual, with periods of tension as workers across white-collar industries pushed against executives’ return-to-office orders.

Those battles have largely come to an end, and workplaces have reached a new hybrid-work status quo. Roughly one-tenth of workers are cobbling together a combination of work in the office and from home, and a similar portion are working entirely remotely.

This population of hybrid and remote workers in the United States doesn’t quite mirror the larger population of workers: Government data shows they tend to have more education and are more often white and Asian.

~115 million workers

~14 million

~15 million

High school or less

Some college

Bachelor’s degree

Graduate degree

Each square here represents 50,000 workers between the ages of 18 and 64. In 2023, about 143 million people in that age range were working in the United States.

A graphic shows a grid of squares representing 143 million workers between 18 and 64.

Roughly 80 percent of those work fully in person. The remaining work either a hybrid schedule or fully remote.

The grid is then split into three sections with color, showing that roughly 115 million of the total 143 million workers are working in person, while about 14 million work a hybrid schedule and another 15 million work fully remote.

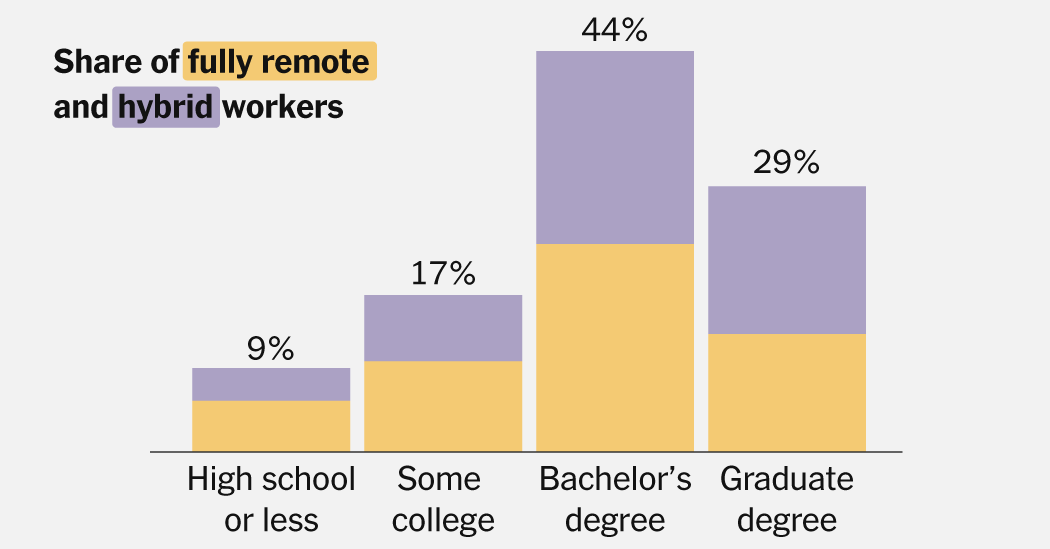

If we look at all workers by their level of education, the biggest group of workers have no college education.

The squares are then arranged by education level, showing that the largest group of workers, more than 47 million, have no college education.

But if we focus on just those who work at home all or some of the time, college educated workers become the most prominent. Working from home is, for the most part, a luxury for the highly educated.

All of the squares representing workers who work in person fly out of the graphic, leaving only workers who work either hybrid or fully remote. The largest group left is now workers with a bachelor’s degree, 12.5 million, followed by workers with graduate degrees, another eight million.

The pandemic laid bare inequalities in the American economy. White-collar workers were in many cases able to do their jobs safely at home, but lower-income workers often had to continue to work in person, even when health risks were highest. And now that the public health emergency is over, that workplace divide — who gets the benefits of remote flexibility and who does not — has become entrenched.

White and Asian workers are more likely to work from home

Share of fully remote and hybrid workers who identify as a given race or ethnicity vs. the same group’s share of the entire work force

White

Asian

Hispanic

Black

Other

0

10

20

30

40

50

60%

Hispanic workers and Black workers are underrepresented in remote work.

Only 10% of remote

20% of all

share of all workers

The divide in who gets the flexibility to work remotely also reflects the country’s racial inequalities. Because white and Asian workers are more likely to hold office jobs, they are more likely to have the opportunity to work remotely part or all of the time. Black and Hispanic workers, meanwhile, more frequently hold jobs in food service, construction, retail, health care and other fields that require them to be in person.

The youngest workers are working from home less often

Share of fully remote and hybrid workers who fall in each age group vs. the same group’s share of the entire work force

Under 25

25-34

35-44

45-54

55-64

0

5

10

15

20

25%

share of all workers

When employers were first mounting their return-to-office battles, many assumed that their youngest employees would be the toughest to persuade to come back. But today, young people make up a greater share of those working in person than their share of the total work force.

That is partly because a smaller share of Americans under 25 have completed college degrees. Many work in jobs like food service that cannot be done remotely. But that is not the whole story: Even among college graduates, workers in their 20s are more likely to be in the office full time than their older colleagues. That suggests that young workers are embracing the benefits of in-person work: socialization, mentorship and face time with the boss. The potential downsides of fixed office schedules may also matter less to them: Relatively fewer young workers might have children (or aging parents) at home, making remote flexibility less of a priority.

More women work remotely, but it’s complicated.

Remote work also breaks down along gender lines — though it does not lend itself to a simple narrative.

Overall, women are more likely than men to work remotely. That’s partly because more women have college degrees, so more of them are in the kind of professional jobs in which flexible arrangements have become the norm. Even among those without college degrees, women are more likely to work at a desk in an administrative or customer support role, while men more often work in construction, manufacturing and other jobs that can only be done in person.

Looking narrowly at just college graduates, remote work patterns for women and men look more evenly distributed, with men slightly more likely to work remotely than women. But there’s one place where the pattern looks different: among parents with young children.

Parents have been some of the biggest winners in the flexible-work era. Remote flexibility made more feasible the constant juggling of professional and caretaking obligations. But it is mothers, not fathers, who appear to be taking the most advantage of workplace flexibility, whether out of choice or necessity.

Share of fully remote and hybridcollege-educated workers who have children or not, by gender

College-educated men

With no kids

With young kids

With older kids

0

10

20

30

40

50

60%

vs. share of all working college-educated men

College-educated women

With no kids

With young kids

With older kids

Mothers of young kids are more likely to work from home than other women.

Note: Young kids are those 5 years old or younger.

Among college-educated men, having children does not make much difference to whether they work at home or in person. Among women, it’s a different story. Mothers of young children are much more likely to work remotely than women without children or mothers of older children.

When possible, disabled workers often choose to go fully remote

Fully remote and hybrid work often get talked about in the same breath. But in some cases, the implications are different.

For many workers with disabilities, the normalization of remote work has offered an opportunity to avoid energy-draining commutes and offices that are not designed to accommodate their needs. For others, it has opened up pathways into industries that were previously difficult to break into.

But those gains come primarily from fully remote work, not the hybrid model that has come to dominate some industries. Workers with disabilities are 22 percent more likely to work fully remotely than otherwise similar workers without disabilities, but only slightly more likely to work a hybrid schedule, according to research from the Economic Innovation Group. Workers with disabilities that limit mobility, such as those who use wheelchairs, were particularly likely to benefit from the opportunity to work entirely from home.

Employers should “understand the significant difference between full-remote and hybrid-remote,” the researchers wrote. “A labor market that includes a greater number of full-remote jobs will open the door for far more otherwise qualified workers.”

Methodology

The data in this article comes from the Current Population Survey, a monthly survey of 60,000 U.S. households conducted by the Census Bureau. Respondents are asked how many hours they worked the previous week, and how many of those hours they teleworked or worked from home. “Fully remote” workers are those who worked all of their hours remotely; “hybrid” workers are those who worked some but not all of their hours remotely. Respondents who were not employed, or who did not work at all in the previous week, are excluded. Data shown is for calendar year 2023. Figures are rounded throughout.

NORMALLY, GAVIN NEWSOM is loose. The Democratic governor of California talks with a staccato cadence, often flitting from one incomplete thought to the next. When he talks to journalists or asks a guest on his podcast a meandering question, he tends to use a lot of meaningless filler words: “in the context of” is a frequent Newsomism. But on June 10th he was clear and direct. “This brazen abuse of power by a sitting president inflamed a combustible situation,” he said during a televised address after President Donald Trump deployed nearly 5,000 troops to Los Angeles to quell protests over immigration raids. “We do not want our streets militarised by our own armed forces. Not in LA. Not in California. Not anywhere.”

A woman shops at a supermarket on April 30, 2025 in Arlington, Virginia.

Sha Hanting | China News Service | Getty Images

Consumers in the early part of June took a considerably less pessimistic about the economy and potential surges in inflation as progress appeared possible in the global trade war, according to a University of Michigan survey Friday.

The university’s closely watched Surveys of Consumers showed across-the-board rebounds from previously dour readings, while respondents also sharply cut back their outlook for near-term inflation.

For the headline index of consumer sentiment, the gauge was at 60.5, well ahead of the Dow Jones estimate for 54 and a 15.9% increase from a month ago. The current conditions index jumped 8.1%, while the future expectations measure soared 21.9%.

The moves coincided with a softening in the heated rhetoric that has surrounded President Donald Trump’s tariffs. After releasing his April 2 “liberation day” announcement, Trump has eased off the threats and instituted a 90-day negotiation period that appears to be showing progress, particularly with top trade rival China.

“Consumers appear to have settled somewhat from the shock of the extremely high tariffs announced in April and the policy volatility seen in the weeks that followed,” survey director Joanne Hsu said in a statement. “However, consumers still perceive wide-ranging downside risks to the economy.”

To be sure, all of the sentiment indexes were still considerably below their year-ago readings as consumers worry about what impact the tariffs will have on prices, along with a host of other geopolitical concerns.

On inflation, the one-year outlook tumbled from levels not seen since 1981.

The one-year estimate slid to 5.1%, a 1.5 percentage point drop, while the five-year view edged lower to 4.1%, a 0.1 percentage point decrease.

“Consumers’ fears about the potential impact of tariffs on future inflation have softened somewhat in June,” Hsu said. “Still, inflation expectations remain above readings seen throughout the second half of 2024, reflecting widespread beliefs that trade policy may still contribute to an increase in inflation in the year ahead.”

The Michigan survey, which will be updated at the end of the month, had been an outlier on inflation fears, with other sentiment and market indicators showing the outlook was fairly contained despite the tariff tensions. Earlier this week, the Federal Reserve of New York reported that the one-year view had fallen to 3.2% in May, a 0.4 percentage point drop from the prior month.

At the same time, the Bureau of Labor Statistics this week reported that both producer and consumer prices increase just 0.1% on a monthly basis, pointing toward little upward pressure from the duties. Economists still largely expect the tariffs to show impact in the coming months.

The soft inflation numbers have led Trump and other White House officials to demand the Fed start lowering interest rates again. The central bank is slated to meet next week, with market expectations strongly pointing to no cuts until September.

Economics1 week ago

Economics1 week ago

Blog Post1 week ago

Blog Post1 week ago

Accounting1 week ago

Accounting1 week ago

Personal Finance1 week ago

Personal Finance1 week ago

Personal Finance6 days ago

Personal Finance6 days ago

Economics6 days ago

Economics6 days ago

Personal Finance6 days ago

Personal Finance6 days ago

Finance6 days ago

Finance6 days ago