Economics

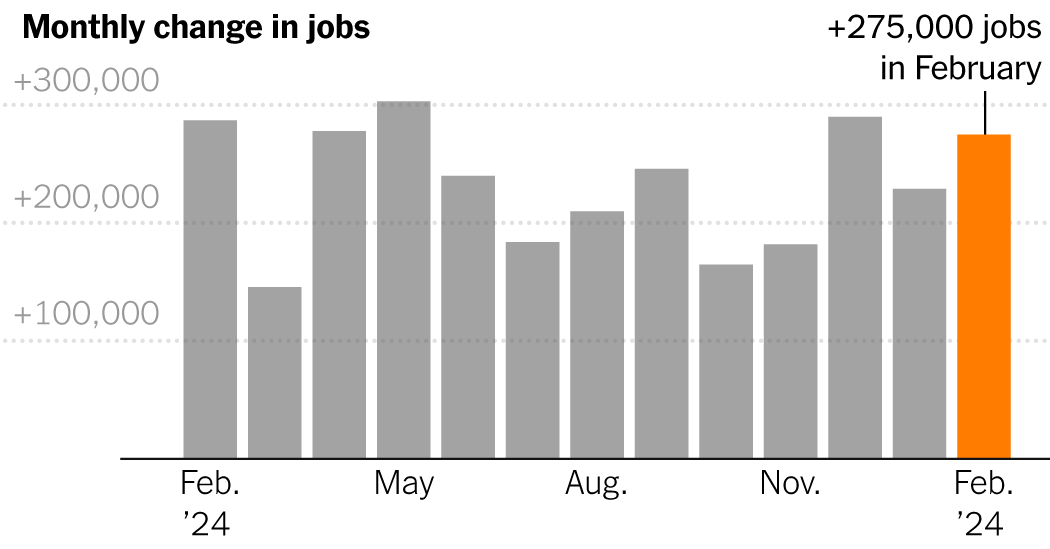

U.S. Employers Add 275,000 Jobs in Another Strong Month

Finance2 months ago

Gen X can’t retire on time as inflation outpaces wages, survey finds

Accounting2 months ago

Are you ready for it? 4 steps to successfully integrate AI into your operations

Personal Finance2 months ago

What that means for consumer loans

Accounting12 months ago

Armanino adds Strategic Accounting Outsourced Solutions

Accounting2 years ago

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

Accounting2 years ago