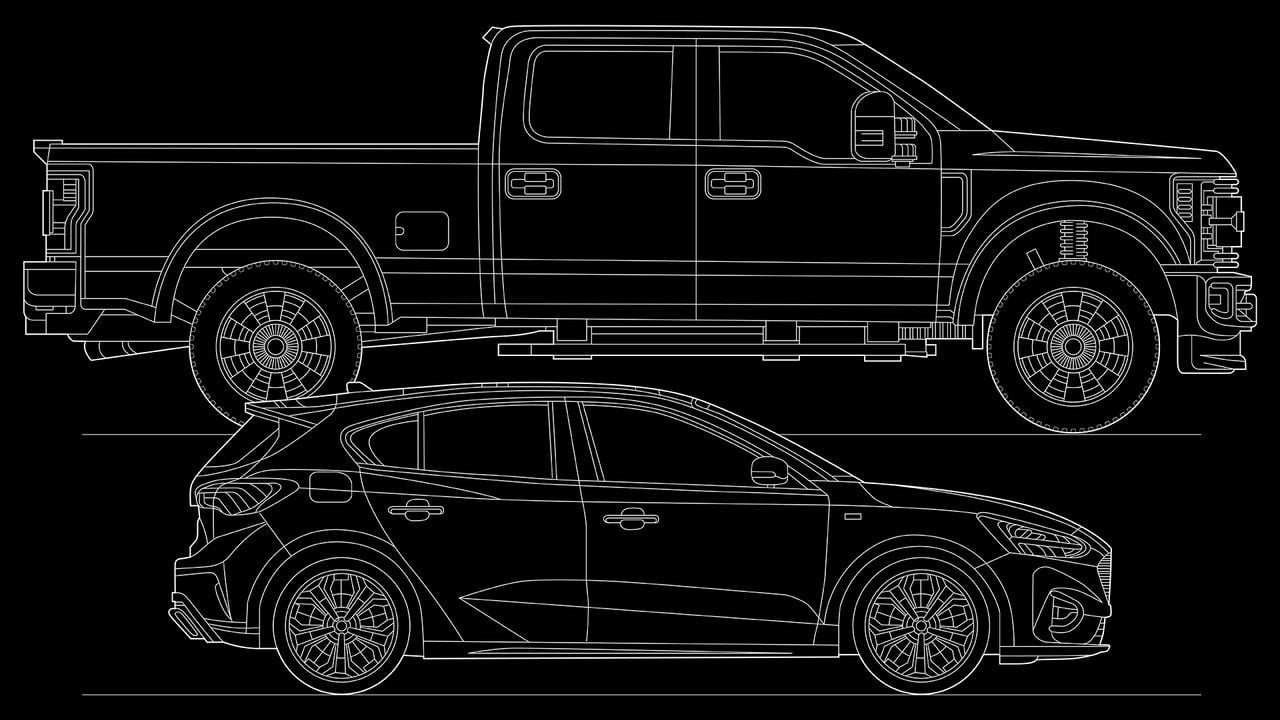

Witnesses said the driver showed no signs of slowing down. On June 3rd Nicole Louthain and her six-year-old daughter were stopped at a red light in Grand Forks, North Dakota when they were struck from behind by Travis Bell. Such crashes are not uncommon—around 10,000 rear-end collisions occur in America every day. What made this one noteworthy was that the vehicles involved were so unevenly matched. Ms Louthain was driving a Ford Focus, a compact car weighing around 3,000lb (1,360kg), whereas Mr Bell was in a 7,000lb Ram 3500 “heavy duty” pickup. Alas, the disparity proved deadly. Although Mr Bell was not harmed, Ms Louthain suffered serious injuries. (Court documents later showed that Mr Bell had been drinking.) Her daughter Katarina was air-lifted to a nearby hospital where she died two days later.

The crash in Grand Forks helps to illustrate a sad truth about America’s roads. For all the safety features available in cars today to help them avoid crashes, when they happen they are still often determined by the laws of physics. When two vehicles collide, it is usually the heavier one that prevails. This advantage has changed little over time. Thirty years ago when a passenger car crashed with a pickup truck or sport-utility vehicle (SUV), the driver of the car was roughly four times as likely to die; today this driver dies around three times as often. Critics say this is too high a price to pay for roomier interiors and more powerful engines. Carmakers insist they are giving consumers what they want. An analysis by The Economist shows that weight remains a critical factor in car crashes in America. Reining in the heaviest vehicles would save lives.

Chevrolet Silverado 5,774lb

Chevrolet Silverado 5,774lb

Chevrolet Silverado 5,774lb

Mismatches between big and small cars on America’s roads are not new. In the 1960s the 1,400lb Mini Cooper shared the road with the 5,000lb Cadillac Fleetwood and the 5,500lb Lincoln Continental. But whereas today heavier vehicles attract the bulk of the criticism, back then it was lighter ones that drew scrutiny. Indeed many cars of the time were woefully unsafe. In 1969 America’s National Highway Safety Bureau conducted crash tests on a Subaru 360 and a King Midget, two sub-1,000lb “mini-cars”. When pitted against vehicles twice their size, the tiny cars crumpled like soda cans.

Over the years policymakers struggled to solve this mismatch, or “incompatibility”, problem. Often, they made things worse. When Congress set fuel-efficiency standards in the wake of the oil shocks of the 1970s, cars were swiftly downsized. Within ten years cars shed 1,000lb; trucks dropped 500lb. Although these changes saved motorists money at the pump, they also led to more traffic fatalities. A paper published in 1989 by researchers at the Brookings Institution and the Harvard School of Public Health estimated that the shift towards smaller, lighter cars in the 70s and 80s boosted fatalities by 14-27%. A report released in 2002 by America’s National Research Council concluded that the downsizing of America’s fleet led to thousands of unnecessary deaths.

As cars got bigger, regulators shifted their focus from the lightest vehicles to the heaviest ones. The impetus for this was the rise of SUVs. Between 1990 and 2005 the market share of such vehicles in America grew from 6% to 26% pushing up the weight of an average new car from 3,400lb to nearly 4,100lb. As suburban soccer moms traded in their station wagons for Ford Expeditions, many felt safer. And they were right. “One of the reasons the roads are much safer is because vehicles… [are] bigger and they’re heavier than they were,” Adrian Lund of the Insurance Institute for Highway Safety (IIHS), an industry research organisation, told conference-goers in 2011. The Competitive Enterprise Institute, a think-tank, even advocated for supersizing America’s fleet to improve safety, writing in the Wall Street Journal that large vehicles are “the solution, not the problem”.

But researchers quickly learned that the extra protection provided by heavier vehicles comes at the expense of others on the road. In a paper published in 2004 Michelle White of the University of California, San Diego estimated that for every deadly crash avoided by an SUV or pickup truck, there are an additional 4.3 among other drivers, pedestrians and cyclists. Another paper in 2012 by Shanjun Li of Resources for the Future, a think-tank, estimated that when a car crashes with an SUV or pickup, rather than another car, the fatality rate of the driver increases by 31%. In 2014 Michael Anderson and Maximilian Auffhammer of the University of California, Berkeley estimated that when two cars crash, a 1,000lb increase in the weight of one vehicle raises the fatality rate in the other by 47%.

Researchers also found that the safety benefits of vehicle weight suffer from diminishing returns. This means that, once vehicles reach a certain weight, packing on more pounds provides little additional safety, while inflicting more harm on others. “At some point heavy vehicles cost more lives…than they save,” wrote Brian O’Neill and Sergey Kyrychenko of the IIHS in 2004. This makes intuitive sense, says Mr Anderson of Berkeley. “Once you outweigh the other guy by a factor of two times, is adding 200 pounds more really going to make a difference for you? Probably not. But it’ll make sure that he gets completely destroyed.”

So how big is too big? At what point do the costs of the heaviest vehicles—measured in lives lost—vastly exceed their benefits? To answer this question, The Economist compiled ten years’ worth of crash data from more than a dozen states. Like the data compiled by Mssrs Anderson and Auffhammer, our figures come from reports filed by police officers, who are tasked with recording information about car crashes when called to the scene. Although all states collect such data, we focus on those that collect the most detailed figures and share them with researchers. The resulting dataset, which covers more than a third of America’s population, provides us with a sample that is both big and representative.

In total, our dataset includes millions of crashes across 14 states occurring between 2013 and 2023. Although accident reports vary from state to state, most of the crashes in our database include information about the geographic location of the crash, the number of cars involved, each passenger’s age and gender, whether they were wearing seatbelts and the types of injuries that they suffered. To obtain the curb weight of each vehicle, we collected the vehicle identification numbers (VINs) included in each crash report, and then matched them to vehicle specs data from VinAudit, an auto-data provider. Combining these data yielded roughly 10m crashes. After dropping observations with missing data, we were left with around 7.5m two-vehicle crashes involving more than 15m cars.

What do these data tell us about the relationship between vehicle weight and road safety?

The heaviest 1% of vehicles in our dataset—those weighing around 6,800lb—suffer 4.1 “own-car deaths” per 10,000 crashes, on average, compared with around 6.6 for cars in the middle of our sample weighing 3,500lb, and 15.8 for the lightest 1% of vehicles weighing just 2,300lb. But heavy cars are also far more dangerous to other drivers. The heaviest vehicles in our data were responsible for 37 “partner-car deaths” per 10,000 crashes, on average, compared with 5.7 for median-weight cars and 2.6 for the lightest cars.

To estimate this relationship more precisely, and control for potential sources of bias, we conducted a regression analysis of our sample of 7.5m two-vehicle crashes. We found that getting into a crash with a vehicle that is 1,000lb heavier is associated with a 0.06 percentage-point increase in the probability of suffering a fatality, even after controlling for the curb weight of one’s own car, the age and gender of the driver, the population density of the crash location and whether the passengers were wearing seatbelts. Given that the probability of suffering a fatality in a two-vehicle crash is 0.09%, on average, this suggests that getting hit by an additional 1,000lbs of steel and aluminium—roughly the difference between a Toyota Camry and a Ford Explorer—boosts the likelihood of a fatality by 66%.

As for the weight at which the social costs of driving a heavier vehicle exceed the benefits, the evidence is clear. Vehicles in the top 10% of our sample—those weighing at least 5,000lb—experience roughly 26 deaths per 10,000 crashes, on average, including 5.9 in their own car and 20.2 in partner vehicles. For vehicles in the next-heaviest 10% of our sample—those weighing between 4,500lb and 5,000lb—the equivalent figures are 5.4 and 10.3 deaths per 10,000 crashes. A back-of-the-envelope estimate suggests that if the heaviest tenth of vehicles in America’s fleet were downsized to this lighter weight class, road fatalities in multi-car crashes—which totaled 19,081 in 2023—could be reduced by 12%, or 2,300, without sacrificing the safety of any cars involved.

Given these figures, one might expect carmakers to be slamming the brakes on production of their heaviest SUVs and pickups. In fact, they are pressing on the accelerator. Official figures from the Environmental Protection Agency show that the average new car in America weighs more than 4,400lb (compared with 3,300lb in the European Union and 2,600lb in Japan). In 2023 vehicles weighing more than 5,000lb accounted for a whopping 31% of new cars, up from 22% five years earlier.

United States, new vehicle production

Source: Environmental Protection Agency

United States, new vehicle production

Source: Environmental Protection Agency

United States, new vehicle production

Source: Environmental Protection Agency

It would be easy to blame car buyers for this trend but Mr Anderson says that Americans looking for a new car face a Cold War-style “arms race”. “As you see the vehicle fleet around you getting heavier, then you want to protect yourself rationally by buying a bigger and heavier car.” Such rational individual decisions have led to a suboptimal outcome for society as a whole.

When asked to comment on The Economist’s findings, representatives from the big three car manufacturers pointed to safety features that help drivers avoid crashes, rather than those that make them less deadly. “Vehicle weight doesn’t solely determine crash performance,” Mike Levine, a Ford spokesman, wrote in an email, highlighting crash-avoidance technologies such as automatic emergency braking and front and rear “brake assist”. General Motors pointed out that carmakers have improved the compatibility of their vehicles over the years, citing a voluntary deal struck by manufacturers in 2003, more than twenty years ago. Stellantis (whose biggest shareholder part-owns The Economist’s parent company) declined to comment except to say that the company’s vehicles “meet or exceed all applicable federal safety standards”.

Regulators are ill-equipped to fix the problem. America’s tax system subsidises heavier vehicles by setting more lenient fuel-efficiency standards for light trucks, and allowing bosses who purchase heavy-duty vehicles for business purposes to deduct part of the cost from their taxable income. The National Highway Traffic Safety Administration (NHTSA), America’s top auto-safety agency, uses a five-star rating system to score crash performance, but only takes account of the safety of the occupants of the vehicle in question, not that of other drivers. “Our rating system reflects a bias towards the occupant,” explains Laura Sandt of the Highway Safety Research Centre at the University of North Carolina, “it is not designed to rate the car in terms of its holistic safety effects.” The NHTSA declined to comment on The Economist’s findings.

There are signs that Americans may be wising up. A survey conducted last year by YouGov, a pollster, found that 41% of Americans think that SUVs and pickup trucks have become too big; 49% said such vehicles are more dangerous for other cars and 50% said they endanger cyclists and pedestrians. Researchers are raising the alarm. Since 1989 the IIHS has regularly published the driver fatality rates of popular car models. In 2023, for the first time, the group also estimated the rate at which cars kill drivers in other vehicles. Policymakers are starting to take notice too. “I’m concerned about the increased risk of severe injury and death for all road users from heavier curb weights,” Jennifer Homendy, chair of the National Transportation Safety Board, said in a speech last year.

But the odds that carmakers curb their heaviest, most dangerous vehicles are slim. American car buyers value safety, but mainly for themselves, not society as a whole. And although regulators are tasked with protecting consumers, they rarely do so at the expense of choice, no matter how deadly the consequences. “There may be a certain point where you say, ‘you know what, passenger vehicles shouldn’t be weighing this much,’” says Raul Arbelaez of the IIHS’s Vehicle Research Centre. “But it would, politically, be really hard to gain any momentum on that.” Finally the shift towards electric power is likely to increase their weight further, as battery-powered vehicles tend to be heavier than their internal-combustion equivalents.

“Manufacturers are playing by the book,” says Mark Chung of the National Safety Council, a non-profit. “They’re making a business decision, and it’s a rational decision. Unless they’re forced to think differently, they’re not going to. So I think this is where our federal partners really need to step up.”■

Sources: State governments; VinAudit; The Economist