Accounting

Accounting Today seeking 2025’s ‘Best Firms for Technology’

Accounting Today is accepting submissions for its report recognizing the Best Accounting Firms for Technology. This is the seventh year the publication will recognize firms in this category.

Given the growing importance of technology to the profession, the report will highlight a range of firms of different sizes that represent the cutting edge of the digital, technological revolution in accounting.

The Best Firms for Technology will be selected based on the policies and technologies they have in place, on their philosophies and strategies surrounding technology in their practice, and on their history in leveraging and implementing technology for their own and their clients’ benefit.

To participate, firms must complete the Best Firms for Tech submission form,

For more information, contact

Enjoy complimentary access to top ideas and insights — selected by our editors.

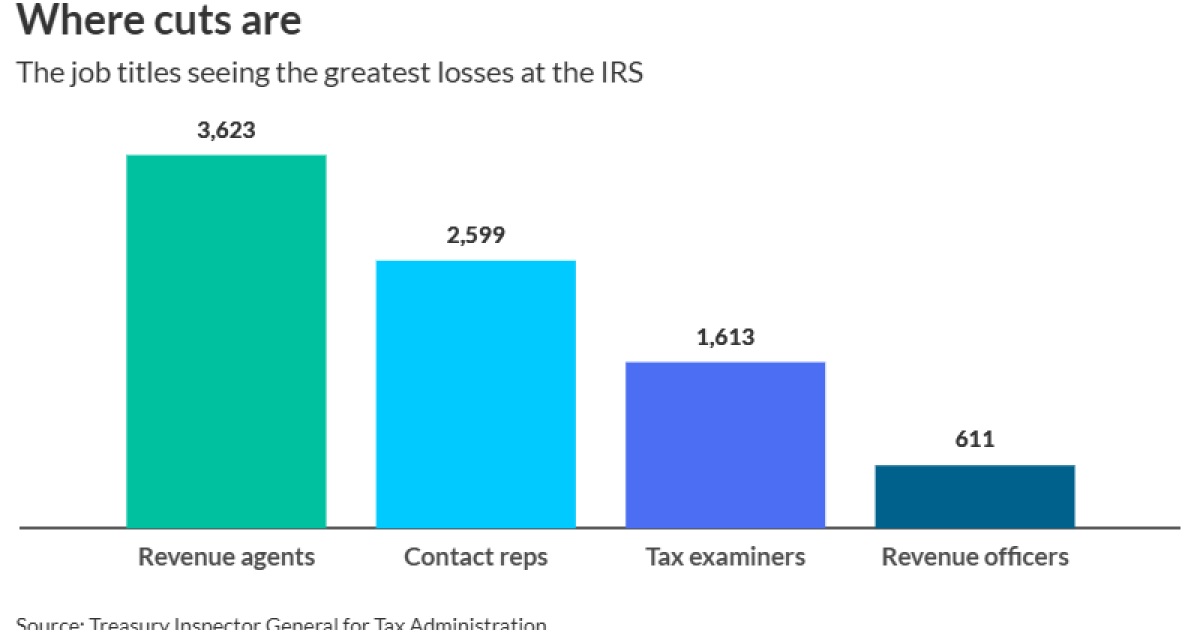

This week’s stats focus in part on the job titles seeing the greatest losses at the IRS during layoffs; as well as the states that have proposed or passed alternatives to the 150-hour rule; the percentage of master’s in accounting program applicants since 2020; the number of PwC employees laid off in May; the projected size of Deloitte’s new New York City headquarters; and the amount of 2026 HSA annual contribution limits, depending on coverage.

CrowdStrike Holdings Inc. said U.S. officials have asked for information related to the accounting of deals it’s made with some customers and said the cybersecurity firm is cooperating with the inquiry.

The Austin, Texas-based company said in a filing Wednesday that it has gotten “requests for information” from the U.S. Department of Justice and the Securities and Exchange Commission “relating to the company’s recognition of revenue and reporting of ARR for transactions with certain customers.” ARR refers to annual recurring revenue, a measure of earnings from subscriptions.

The company said the federal officials have also sought information related to a CrowdStrike update last year that crashed Windows operating systems around the world.

“The company is cooperating and providing information in response to these requests,” the filing states.

U.S. prosecutors and regulators have been investigating a $32 million deal between CrowdStrike and a technology distributor, Carahsoft Technology Corp., to provide cybersecurity tools to the Internal Revenue Service, Bloomberg News first reported in February. The IRS never purchased or received the products, Bloomberg News

The investigators are probing what senior CrowdStrike executives may have known about the $32 million deal and are examining other transactions made by the cybersecurity firm, Bloomberg News

Asked for comment about the filing, CrowdStrike spokesperson Brian Merrill said, “As we have told Bloomberg repeatedly, this is old news and we stand by the accounting of the transaction.”

A lawyer for Carahsoft previously declined to comment on the federal investigations, and representatives didn’t respond to subsequent requests for comment about them.

Tech titan Elon Musk ratcheted up his offensive against Donald Trump’s signature tax bill on Wednesday, urging that Americans contact their lawmakers to “KILL” the legislation.

“Call your Senator, Call your Congressman,” Musk wrote in a

The post came one day after Musk lashed out at the tax bill, describing it as a budget-busting “disgusting abomination” as Republican fiscal hawks stepped up criticism of the massive fiscal package.

Trump hasn’t publicly responded to Musk’s comments, but the White House put out a statement Wednesday saying the legislation “unleashes an era of unprecedented economic growth.”

And House Speaker Mike Johnson told reporters that Musk is “dead wrong” about the bill and that the tax cuts will pay for themselves through economic growth.

Musk’s public condemnation pits him against the president at a critical time as Trump is personally lobbying holdouts on the bill. His campaign against the legislation threatens to stiffen resistance and delay enactment of the tax cuts and debt ceiling increase.

Musk has attacked the legislation days after leaving a temporary assignment leading the administration’s Department of Government Efficiency initiative to cut federal spending. The Tesla Inc. chief executive officer’s high-profile role in the Trump administration eroded his business brand and sales of his company’s electric vehicles plunged.

The House-passed version of the tax and spending bill would add $2.4 trillion to U.S. budget deficits over the next decade, according to an

The CBO’s calculation reflects a $3.67 trillion decrease in expected revenues and a $1.25 trillion decline in spending over the decade through 2034, relative to baseline projections. The score doesn’t account for any potential boost to the economy from the bill, which Johnson and Trump argue would offset the revenue losses.

Musk, the world’s richest man with a net worth of about $377 billion according to the Bloomberg Billionaires Index, has become a crucial financial backer of the Republican party. After making modest donations most years, Musk became the biggest U.S. political donor in 2024, giving more than $290 million.

Johnson said Musk had promised to help reelect Republicans just a day before savaging Trump’s bill. Musk did not respond to a request for comment.

Most of Musk’s giving was aimed at electing Trump but he also supported congressional candidates. America PAC, the super political action committee that Musk largely funded, spent $18.5 million in 17 separate House races. Though that total pales in comparison to the roughly $255 million he spent backing Trump, the spending means a lot in a congressional election, where challengers on average raise less than $1 million.

Control of the House will likely be decided by the outcome of fewer than two dozen close races in the 2026 midterm elections. The GOP’s chances of holding their majority would suffer a major blow if Musk were to withdraw his financial support.

Accountants on IRS and PwC layoffs, accounting students and more

Can AI predict Supreme Court rulings?

Stocks making the biggest moves after hours: FIVE, MDB, VRNT

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Economics1 week ago

Economics1 week agoElon Musk says Trump’s spending bill undermines the work DOGE has been doing

-

Accounting1 week ago

Accounting1 week agoHighest paid jobs in corporate accounting

-

Blog Post4 days ago

Blog Post4 days agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics1 week ago

Economics1 week agoHow young voters helped to put Trump in the White House

-

Personal Finance1 week ago

Personal Finance1 week agoHarvard, Trump international enrollment battle affects college applicants

-

Economics6 days ago

Economics6 days agoWhy the president must not be lexicographer-in-chief

-

Personal Finance1 week ago

Personal Finance1 week agoCrypto in 401(k) plans: Trump administration eases rules

-

Finance1 week ago

Finance1 week agoVail Resorts, GameStop and more