Accounting

Fostering the next generation of women leaders in accounting and finance

In honor of Women’s History Month, I’ve taken time to reflect on my journey as a leader in the financial technology sector. Earlier in my career, I encountered the challenges that many women in our industry face, from biased hiring practices to persistent pay gaps. Advancing in accounting and finance often feels like walking a tightrope, demanding resilience, determination and a constant push for equity at every step.

At the same time, I’ve seen how much value women bring to our industry’s leadership spaces. Our differing perspectives and skills facilitate growth, improve company culture and foster the next generation of leaders.

Thankfully, with help from their own modern organizations, women have made tremendous progress in our field, but there’s still work to be done.

Women face challenges in advancing their careers

While workplace equality has come a long way, some women in accounting and finance still encounter barriers to advancement in companies that have yet to evolve. Fortunately, I’m proud to work for a forward-thinking financial technology company that actively fosters growth and advancement opportunities for women.

Perceptions and structural challenges can discourage many from long-term careers, contributing to their underrepresentation in leadership. By tackling these issues and reshaping the narrative, we can create more opportunities for women to thrive.

Stigma around the industry

Accounting and finance may not be the most “glamorous” of industries. Many young professionals overlook these fields, assuming they lack excitement or the potential for meaningful career growth.

My own career proves this isn’t true. Finance is a dynamic field with many opportunities for growth, networking and even travel. By connecting with young people and highlighting the most rewarding aspects of our field, we can inspire the next generation of accounting and finance professionals.

Barriers to leadership

In outdated organizations, women can encounter challenges that make it difficult to advance beyond entry- or mid-level positions. These barriers range from unconscious bias and lack of mentorship to structural hurdles that limit access to high-profile projects and leadership tracks. While many organizations have made strides in diversity and inclusion efforts, true progress requires more than just hiring initiatives — it demands a fundamental shift in how career development is structured.

One key solution may lie in rethinking internal career development programs. Without clear pathways for advancement, many talented women find themselves stagnating in roles that don’t fully utilize their skills or position them for leadership opportunities. Addressing this issue means implementing mentorship programs, leadership training and sponsorship opportunities that actively support women’s career progression.

Workplace biases and additional expectations

While great progress has been made, bias toward women in the financial and accounting industries still lingers within antiquated companies. Men who hold these views aren’t as outspoken about them as they may have been in the past. But the perspective often seeps into the expectations others have of women — even in leadership settings.

For example, women are often recognized for their natural ability to nurture and support those around them, which can be a valuable strength. However, this perception can sometimes lead to women being steered toward roles that may not fully align with their career goals — such as managing employees, onboarding new hires or organizing company events. Even seemingly small assumptions, like being assigned as the note taker due to “better handwriting,” can reinforce patterns that unintentionally limit access to higher-level opportunities.

The power of female mentorship in finance and accounting

Building a successful, high-level career as a woman in finance and accounting is absolutely possible. The challenge is that many of us start out without a clear roadmap for advancement. That’s why I’m a strong advocate for mentorship — having guidance and support early on can make all the difference in navigating the path to leadership.

When I started in our industry, a female leader took me under her wing. She taught me how to be an effective manager, how to act in a boardroom, and how to deal with people and challenges in different settings. But most importantly, she showed me how to infiltrate leadership spaces. This has had a profound impact on my career as an African-American woman in a primarily white, male-dominant industry.

That’s why I make it a priority to pay forward the guidance and support my own mentor once gave me. I believe in sharing knowledge freely, which is why I’m mentoring four rising women leaders, helping them build confidence, develop their skills and navigate workplaces that are still largely male-dominated.

Mentorship isn’t just about individual growth; it’s about ensuring each new generation of women in finance starts from a stronger position than the last. By passing down insights, strategies and hard-earned lessons, we create a ripple effect that accelerates progress. And that, more than anything, will help us close the leadership gap and advance at the same pace as our male counterparts.

Attracting the next generation of female leaders

Mentorship is a powerful tool for helping women advance once they’ve entered the finance industry. But the bigger challenge starts even earlier. Many ambitious young women don’t see finance as a career path worth pursuing. If we want to achieve true equality, we need to address this recruitment gap, making the industry more visible, accessible and appealing to the next generation of female leaders.

Engage young women early

First, we need to be more proactive in reaching young women at the start of their career journey. That means increasing our presence at local colleges, cultural fairs, conferences and professional events.

Finance is an incredibly rewarding career, but young women need to see that for themselves and have clear entry points to explore their potential. Internships, mentorship programs and even simple coffee meetings can make a huge difference in helping them take that first step. Think of it as building a bridge — one that connects ambitious young women to the opportunities our industry has to offer.

Creating an inclusive hiring process

Getting young women interested in finance is a great place to start. But we also need to ensure they’re being hired. A more inclusive hiring process is key to making that happen — one that minimizes the influence of unconscious bias and focuses purely on talent and potential.

One effective approach is blind hiring, where companies assess resumes and written responses without knowing a candidate’s gender. This levels the playing field, ensuring the most qualified person gets the job based on merit rather than outdated perceptions of who “fits the part.” By adopting practices like this, we can build a more diverse, equitable finance industry that welcomes and elevates women from the start.

Building workplaces that retain women

We should also seek to build workplaces that retain a higher percentage of their female employees. That starts with paying women an equal wage. But it also means embracing work-life balance and flexibility.

Flexibility in the workplace isn’t just a perk — it’s a necessity for retaining top female talent. Companies that offer hybrid or remote work options, flexible scheduling and generous parental leave policies create environments where women don’t have to choose between career advancement and personal commitments. When organizations recognize that productivity isn’t defined by rigid office hours, they open the door for more women to thrive in finance without sacrificing other aspects of their lives.

Internal career development programs

Finally, we should create more sophisticated career development programs. These help women progress in their careers by showing them exactly what they need to do to rise into leadership. They help with retention and advancement — two key steps toward equality in the financial industry.

A well-designed career development program does more than offer occasional workshops or mentorship opportunities. It provides a structured framework for growth, outlining the skills, experiences and milestones necessary for women to progress into leadership roles. These programs should include:

● Transparent promotion criteria – Clearly defining what it takes to move up in an organization helps eliminate ambiguity and bias, ensuring women have the same opportunities for advancement as their male colleagues.

● Mentorship and sponsorship – While mentorship provides guidance, sponsorship connects women with influential advocates who can actively support their career growth, recommend them for leadership roles and open doors to high-profile projects.

● Leadership training and skill-building – Equipping women with executive-level skills, such as negotiation, strategic decision-making and financial forecasting, prepares them for leadership positions and strengthens their confidence in pursuing them.

● Stretch assignments and high-visibility projects – Women should be given opportunities to take on challenging assignments that demonstrate their capabilities and position them for promotion. Too often, they are siloed into support roles rather than being encouraged to lead critical initiatives.

● Work-life integration support – Career growth shouldn’t come at the cost of personal wellbeing. Programs that include flexible leadership tracks, remote work options and family-friendly policies ensure women can advance without sacrificing work-life balance.

The path forward

I’m fortunate to have found my path in the industry, gaining momentum in leadership and ultimately securing a role at

- Engaging young women early in their careers

- Promoting woman-to-woman mentorship relationships;

- Removing bias from our hiring processes; and

- Creating more concrete career development programs.

The future for women in finance is full of potential, but there’s still work to be done. Progress won’t happen on its own — it requires collective effort, commitment and a shared vision to create real change.

Enjoy complimentary access to top ideas and insights — selected by our editors.

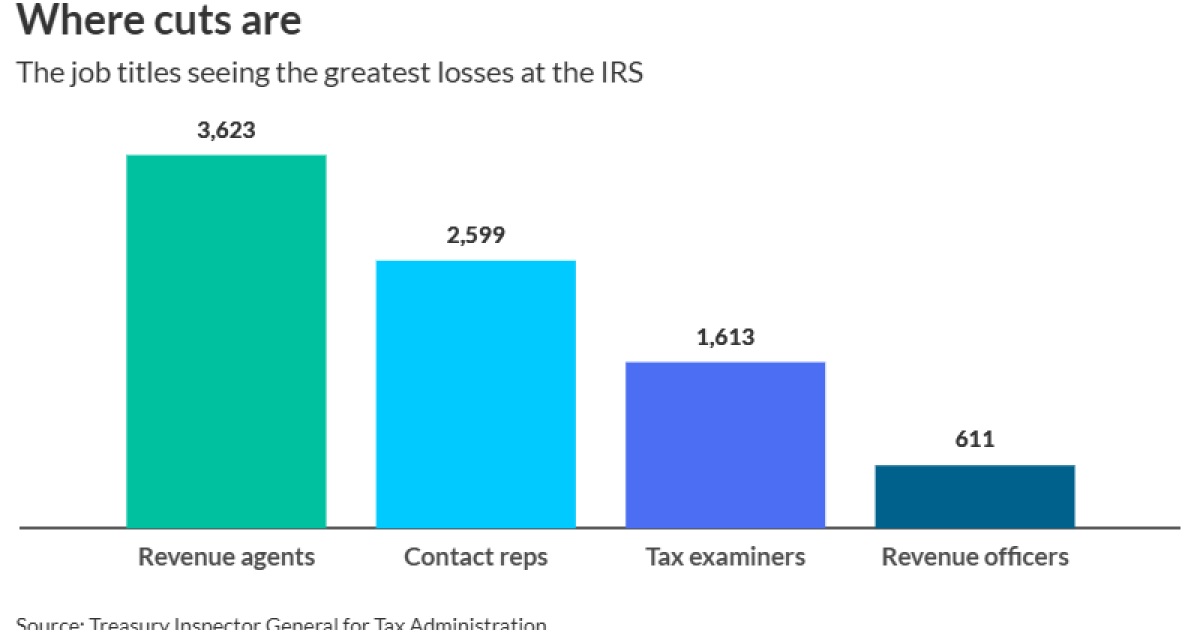

This week’s stats focus in part on the job titles seeing the greatest losses at the IRS during layoffs; as well as the states that have proposed or passed alternatives to the 150-hour rule; the percentage of master’s in accounting program applicants since 2020; the number of PwC employees laid off in May; the projected size of Deloitte’s new New York City headquarters; and the amount of 2026 HSA annual contribution limits, depending on coverage.

CrowdStrike Holdings Inc. said U.S. officials have asked for information related to the accounting of deals it’s made with some customers and said the cybersecurity firm is cooperating with the inquiry.

The Austin, Texas-based company said in a filing Wednesday that it has gotten “requests for information” from the U.S. Department of Justice and the Securities and Exchange Commission “relating to the company’s recognition of revenue and reporting of ARR for transactions with certain customers.” ARR refers to annual recurring revenue, a measure of earnings from subscriptions.

The company said the federal officials have also sought information related to a CrowdStrike update last year that crashed Windows operating systems around the world.

“The company is cooperating and providing information in response to these requests,” the filing states.

U.S. prosecutors and regulators have been investigating a $32 million deal between CrowdStrike and a technology distributor, Carahsoft Technology Corp., to provide cybersecurity tools to the Internal Revenue Service, Bloomberg News first reported in February. The IRS never purchased or received the products, Bloomberg News

The investigators are probing what senior CrowdStrike executives may have known about the $32 million deal and are examining other transactions made by the cybersecurity firm, Bloomberg News

Asked for comment about the filing, CrowdStrike spokesperson Brian Merrill said, “As we have told Bloomberg repeatedly, this is old news and we stand by the accounting of the transaction.”

A lawyer for Carahsoft previously declined to comment on the federal investigations, and representatives didn’t respond to subsequent requests for comment about them.

Tech titan Elon Musk ratcheted up his offensive against Donald Trump’s signature tax bill on Wednesday, urging that Americans contact their lawmakers to “KILL” the legislation.

“Call your Senator, Call your Congressman,” Musk wrote in a

The post came one day after Musk lashed out at the tax bill, describing it as a budget-busting “disgusting abomination” as Republican fiscal hawks stepped up criticism of the massive fiscal package.

Trump hasn’t publicly responded to Musk’s comments, but the White House put out a statement Wednesday saying the legislation “unleashes an era of unprecedented economic growth.”

And House Speaker Mike Johnson told reporters that Musk is “dead wrong” about the bill and that the tax cuts will pay for themselves through economic growth.

Musk’s public condemnation pits him against the president at a critical time as Trump is personally lobbying holdouts on the bill. His campaign against the legislation threatens to stiffen resistance and delay enactment of the tax cuts and debt ceiling increase.

Musk has attacked the legislation days after leaving a temporary assignment leading the administration’s Department of Government Efficiency initiative to cut federal spending. The Tesla Inc. chief executive officer’s high-profile role in the Trump administration eroded his business brand and sales of his company’s electric vehicles plunged.

The House-passed version of the tax and spending bill would add $2.4 trillion to U.S. budget deficits over the next decade, according to an

The CBO’s calculation reflects a $3.67 trillion decrease in expected revenues and a $1.25 trillion decline in spending over the decade through 2034, relative to baseline projections. The score doesn’t account for any potential boost to the economy from the bill, which Johnson and Trump argue would offset the revenue losses.

Musk, the world’s richest man with a net worth of about $377 billion according to the Bloomberg Billionaires Index, has become a crucial financial backer of the Republican party. After making modest donations most years, Musk became the biggest U.S. political donor in 2024, giving more than $290 million.

Johnson said Musk had promised to help reelect Republicans just a day before savaging Trump’s bill. Musk did not respond to a request for comment.

Most of Musk’s giving was aimed at electing Trump but he also supported congressional candidates. America PAC, the super political action committee that Musk largely funded, spent $18.5 million in 17 separate House races. Though that total pales in comparison to the roughly $255 million he spent backing Trump, the spending means a lot in a congressional election, where challengers on average raise less than $1 million.

Control of the House will likely be decided by the outcome of fewer than two dozen close races in the 2026 midterm elections. The GOP’s chances of holding their majority would suffer a major blow if Musk were to withdraw his financial support.

How to review your insurance policy

Accountants on IRS and PwC layoffs, accounting students and more

Can AI predict Supreme Court rulings?

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Economics1 week ago

Economics1 week agoElon Musk says Trump’s spending bill undermines the work DOGE has been doing

-

Accounting1 week ago

Accounting1 week agoHighest paid jobs in corporate accounting

-

Blog Post4 days ago

Blog Post4 days agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics1 week ago

Economics1 week agoHow young voters helped to put Trump in the White House

-

Personal Finance1 week ago

Personal Finance1 week agoHarvard, Trump international enrollment battle affects college applicants

-

Economics6 days ago

Economics6 days agoWhy the president must not be lexicographer-in-chief

-

Personal Finance1 week ago

Personal Finance1 week agoCrypto in 401(k) plans: Trump administration eases rules

-

Finance1 week ago

Finance1 week agoVail Resorts, GameStop and more