Personal Finance

Here’s what to know before using AI chatbots to file your taxes

Songsak Rohprasit | Moment | Getty Images

The tax deadline is approaching and some filers are turning to chatbots powered by artificial intelligence for help with returns.

But taxpayers should be wary of generative AI — which uses artificial intelligence to create content — for tax advice, experts say.

Nearly 1 in 5 Americans would trust ChatGPT, a popular AI chatbot from OpenAI, to review their income taxes, and 14% have used it, according to a February survey of roughly 1,000 U.S. adults from CardRates.com.

Another recent survey had similar findings, with 17% saying they have used AI for tax filing and 45% open to it for future use, a Harris Poll found.

While many experts are optimistic about the future of generative AI and taxes, filers should “proceed with caution” when using the software to file returns, said April Walker, lead manager for tax practice and ethics at the American Institute of CPAs.

More from Personal Finance:

There’s still time to reduce your tax bill or boost your refund before the deadline

An ‘often overlooked’ retirement savings option can lower your tax bill

Some retirement savers can still get a ‘special tax credit,’ IRS says

“We caution users against using ChatGPT for financial advice, as they should seek a professional instead. This activity actually goes against our usage policies,” a spokesperson from OpenAI told CNBC.

AI chatbots ‘aren’t ready for prime time’

This season, taxpayers have several options for AI-powered guidance, including software like ChatGPT, along with chatbots from TurboTax, H&R Block and the IRS.

In 2022, the IRS rolled out voice and chatbots to help answer basic payment and collection notice questions. The agency has since expanded its use of AI-driven technology.

Since the January 2022 rollout, the IRS used chatbots to help more than 13 million taxpayers and helped set up about $151 million in payment agreements, the agency announced in September.

Pranithan Chorruangsak | Istock | Getty Images

Meanwhile, TurboTax has unveiled the generative AI-powered “Intuit Assist” chatbot. The was chatbot was designed to help with software already using AI for “simplified filing” and more accurate returns, according to Karen Nolan, senior communications manager at Intuit TurboTax.

However, “AI is not completing or filing a tax return in TurboTax,” she said. “If a TurboTax filer ever has a question about their tax return, they are only a click away from a live tax expert at all times.”

H&R Block, which has used AI for years, also introduced a generative chatbot with “AI Tax Assist” this season. The tool assists the process for DIY filers and the company has instructions on the best way to use it.

“We also have a team of human testers reviewing questions and feedback daily to identify what to add and improve,” a company spokesperson said.

Still, AI chatbots “aren’t ready for prime time,” when filing tax returns, according to Subodha Kumar, professor of statistics, operations and data science at the Fox School of Business at Temple University.

Kumar has tested AI chatbots with his students and found the software works for general tax questions, but often provides wrong answers for more specific prompts.

For example, filers may not get accurate answers to tax questions from ChatGPT because its training is “general purpose” rather than tax-specific, he said.

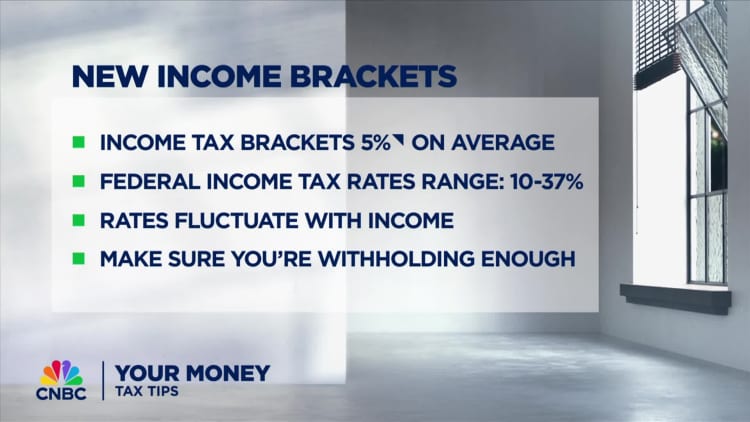

Plus, the data isn’t fully updated, with different knowledge cutoff dates, depending on which version of ChatGPT you’re using. The latest AI model is GPT-4 Turbo, and provides answers with context up to April 2023. That could be an issue with yearly inflation adjustments, tax changes from Congress and the IRS.

However, with models specifically trained for tax, Kumar expects a “big leap” from tax-specific AI chatbots by next season.

Protect yourself from data ‘leakage’

While experts agree that AI chatbots aren’t ready for personalized tax recommendations, there’s still a chance for education.

“I think there are opportunities to use tools like that in a generalized context,” said Michael Prinzo, managing principal of tax at CliftonLarsonAllen. “It could be an effective tool as long as personal information is protected.”

Experts warn there could be data security issues when plugging financial information into ChatGPT or other AI chatbots.

“There could be multiple types of [data] leakage,” explained Spencer Lourens, managing principal of data science, machine learning and artificial intelligence at CliftonLarsonAllen.

However, you could input a general fact pattern of possible income sources and tax breaks without including sensitive personal data and relying on the software for a specific answer.

Of course, you should always verify any information received from AI-powered chatbots by double-checking the details on the IRS website or with a tax professional, added Walker with the American Institute of CPAs.

US Secretary of Education Linda McMahon attends the International Women of Courage Awards Ceremony at the State Department in Washington, DC, on April 1, 2025.

Brendan Smialowski | Afp | Getty Images

Jason Collier, a special education teacher in Virginia, often needs to wait until payday to fill up the gas tank of his car — and in the meantime hopes he doesn’t run out.

“Money is tight when you’re a teacher,” Collier, 46, said.

Now he’s afraid that the U.S. Department of Education will soon garnish up to 15% of his wages because he’s behind on his student debt payments. Collier said he hasn’t been able to meet his monthly bill for years, while juggling the expenses of raising two children and medical expenses from a cancer diagnosis.

If his paycheck is garnished, “it would just be more of a pinch,” Collier said. “If I need a car repair, or something comes up, I might not be able to do those things.”

The consequences are punitive and sometimes tragic.

James Kvaal

former Education Dept. undersecretary

After a half-decade pause of collection activity on federal student loans, the Trump administration announced on April 21 that it would once again seize defaulted borrowers’ federal tax refunds, paychecks and Social Security benefits.

More than 5 million student loan borrowers are currently in default, and that total could swell to roughly 10 million borrowers within a few months, according to the Education Department.

The Biden administration focused on extending relief measures to struggling borrowers in the wake of the Covid pandemic and helping them to get current. The Trump administration’s aggressive collection activity is a sharp turn away from that strategy.

“Borrowers should pay back the debts they take on,” said U.S. Secretary of Education Linda McMahon in a video posted on X on April 22.

More than 42 million Americans hold student loans, and collectively, outstanding federal education debt exceeds $1.6 trillion. The Education Department can garnish up to 15% of defaulted borrowers’ disposable income and federal benefits, as well as their entire federal tax refunds.

“In an environment where the cost of living remains stubbornly high, this kind of withholding from your income can pose real problems when trying to make ends meet, and force people into choosing between vital expenses,” said Nancy Nierman, assistant director of the Education Debt Consumer Assistance Program in New York.

Most people who default on their student loans “truly cannot afford to pay them,” James Kvaal, who served as U.S. undersecretary of education for former President Joe Biden, said in an April interview with CNBC.

“The consequences are punitive and sometimes tragic,” Kvaal said.

A retiree who can’t go home now

Marceline Paul and her grandson

Courtesy: Marceline Paul

Marceline Paul is homesick.

But if the Trump administration begins garnishing her Social Security benefit next month, there’s no way she’ll be able to afford a trip back to Trinidad. She moved from there to the United States in the ’70s.

“I need to go home,” said Paul, 68, who worked for decades in the health care industry and retired during the Covid-19 pandemic to take care of her sick mother.

The student debt she had taken on for her daughter was the last thing on her mind during that time, she said: “I couldn’t focus on anything else.”

She felt terrified when she received a recent notice from the Education Dept. that her retirement check could be offset. Nearly all of her income comes from her monthly Social Security benefit of around $2,600. Social Security benefits can generally be reduced by up to 15% to repay student debt in default, so long as beneficiaries are left with at least $750 per month.

“When I saw that email, it made me sick to my stomach,” Paul said.

Already on a tight budget in retirement, the garnishment will force her to cut back on her everyday expenses, skip necessary repairs on her house in Maryland and forgo traveling to her home country.

“I don’t know the last time I had a vacation,” she said. “I’ve paid into the system and I should be able to retire.”

More than 450,000 borrowers ages 62 and older in default on their federal student loans and likely to be receiving Social Security benefits, the Consumer Financial Protection Bureau found earlier this year.

Collection activity begins despite chaotic time

Over the roughly five-year period during which the Education Dept. suspended its collection of federal student loans, there have been sweeping changes and disruptions to the lending system.

Millions of borrowers who signed up for the Biden administration’s new repayment plan, known as SAVE, or the Saving on a Valuable Education program, were caught in limbo after GOP-led lawsuits managed to get the plan blocked in the summer of last year. Many of those borrowers will now have to switch out of a Biden-era payment pause and into another repayment plan that will spike their monthly bill.

But in recent months, the Trump administration has terminated around half of the Education Department’s staff, including many of the people who helped assist borrowers.

Now some student loan borrowers report waiting hours on the phone before being able to reach someone about their debt, despite the Trump administration telling borrowers to contact it to get current.

The Education Department did not respond to a request for comment.

Borrowers try and fail to get current on their loans

Kia Brown, who works as a management analyst at the Department of Veterans Affairs, wants to start repaying her student loans again — but she said she’s run into numerous challenges trying to do so.

“The biggest issue I have is the lack of information,” said Brown, 44.

When she signed up for Biden’s SAVE plan, she could afford her monthly student loan bill of $150. But now that plan is blocked and she’s worried she won’t be able to afford her new payment.

She received conflicting information over whether her student loan servicer was Mohela or Navient (millions of people have had their accounts transferred between companies in recent years.) When she tried to reach someone at Navient about her student debt, she was on hold for more than two hours.

Meanwhile, a representative at Mohela couldn’t tell her what her new student loan payment would be, though she was quoted $319 by the company’s automated phone system.

Mohela and Navient did not respond to a request for comment.

Brown is still not sure which company is managing her account.

“The narrative is that people are dodging their payments,” Brown said, but added that she doesn’t think that’s true for many borrowers. “I truly believe many people will be blindsided due to lack of guidance on how to repay.”

If she’s not able to reach someone at the Education Dept. to get current on her payments and her wages are garnished, it’ll be a significant hardship for her family, she said.

“We’re living paycheck to paycheck,” she said. “I’m lucky if I can even put aside $100 for myself.”

U.S. President Donald Trump talks to reporters aboard Air Force One, en route to Abu Dhabi, United Arab Emirates, on May 15, 2025.

Brian Snyder | Reuters

As the Trump administration ramps up its student loan collection efforts, worried borrowers need to ask themselves a key question: Am I delinquent, or in default? The answer determines your best next steps.

“We’ve had a lot of clients contacting us recently who are extremely stressed and, in some cases panicked, about their loan situation,” said Nancy Nierman, assistant director of the Education Debt Consumer Assistance Program in New York.

More from Personal Finance:

How many consumers are preparing for an economic hit

Why Americans think real estate, gold are the best long-term investments

Trump tariffs sparked ‘uptick’ in I bond interest, advisor says. What to know

However, some borrowers wrongly believe they’ll be subject to wage garnishments or offsets of their retirement benefits — when in fact they are delinquent but not yet in default, Nierman said.

If you’re delinquent, there are things you can do to avoid default. And even those who are in default and at risk for collections can take steps to avoid such outcomes.

“The federal student loan system does provide several paths for bringing loans out of default,” she said.

Delinquent or in default? Here’s how to tell

Just because you’re behind on your payments doesn’t mean you’re in default.

Your student loan becomes past due, or delinquent, the first day after you miss a payment, according to the U.S. Department of Education.

Nearly 8% of total student debt was reported as 90 days past due in the first quarter of 2025, the New York Fed recently found.

Once you are delinquent for 90 days or more, your student loan servicer will report your past due status to the national credit bureaus, which can lead to a drop in your credit score.

The Federal Reserve predicted in March that some people with a student loan delinquency could see their scores fall by as much as 171 points. (Credit scores typically range from 300 to 850, with around 670 and higher considered good.)

Lower credit scores can lead to higher borrowing costs on consumer loans such as mortgages, car loans and credit cards.

But you’re not considered to be in default on your student loans until you haven’t made your scheduled payment in at least 270 days, the Education Department says.

Only borrowers in default face garnishments

The federal government has extraordinary collection powers on its student loans and it can seize borrowers’ tax refunds, paychecks and Social Security retirement and disability benefits.

But only those who’ve defaulted on their student loans can face these consequences, experts said.

How to get out of student loan delinquency

Delinquent student loan borrowers should call their student loan servicer right away and request a retroactive forbearance for missed payments and then a temporary forbearance until they enroll in a repayment plan they can afford, according to the experts at the Education Debt Consumer Assistance Program. Some monthly bills under income-driven repayment plans wind up being as low as zero dollars.

There are also economic hardship and unemployment deferments available for those who qualify, as well as other ways to keep your loan payments paused while not falling behind.

How to get out of student loan default

Meanwhile, more than 5.3 million student loan borrowers are currently in default, and that total could swell to roughly 10 million borrowers within a few months, the Education Department estimates.

You can contact the government’s Default Resolution Group and pursue a number of different avenues to get current on your loans, including enrolling in an income-driven repayment plan or signing up for loan rehabilitation.

You can get out of default on your student loans through rehabilitating or consolidating your debt, Nierman said.

Rehabilitating involves making “nine voluntary, reasonable and affordable monthly payments,” according to the U.S. Department of Education. Those nine payments can be made over “a period of 10 consecutive months,” it said.

Consolidation, meanwhile, may be available to those who “make three consecutive, voluntary, on-time, full monthly payments.” At that point, they can essentially repackage their debt into a new loan.

After you’ve emerged from default, experts also recommend requesting a monthly bill you can afford.

If you don’t know who your loan servicer is, you can find out at Studentaid.gov.

“Explore your options and create a plan for returning your loans back to good standing so you will not be subject to punitive collections activity,” Nierman said.

Kate_sept2004 | E+ | Getty Images

Long-term care can be costly, extending well beyond $100,000. Yet, financial advisors say many households aren’t prepared to manage the expense.

“People don’t plan for it in advance,” said Carolyn McClanahan, a physician and certified financial planner based in Jacksonville, Florida. “It’s a huge problem.”

Over half, 57%, of Americans who turn 65 today will develop a disability serious enough to require long-term care, according to a 2022 report published by the U.S. Department of Health and Human Services and the Urban Institute. Such disabilities might include cognitive or nervous system disorders like dementia, Alzheimer’s or Parkinson’s disease, or complications from a stroke, for example.

The average future cost of long-term care for someone turning 65 today is about $122,400, the HHS-Urban report said.

But some people need care for many years, pushing lifetime costs well into the hundreds of thousands of dollars — a sum “out of reach for many Americans,” report authors Richard Johnson and Judith Dey wrote.

The number of people who need care is expected to swell as the U.S. population ages amid increasing longevity.

“It’s pretty clear [workers] don’t have that amount of savings in retirement, that amount of savings in their checking or savings accounts, and the majority don’t have long-term care insurance,” said Bridget Bearden, a research and development strategist at the Employee Benefit Research Institute.

“So where is the money going to come from?” she added.

Long-term care costs can exceed $100,000

While most people who need long-term care “spend relatively little,” 15% will spend at least $100,000 out of pocket for future care, according to the HHS-Urban report.

Expense can differ greatly from state to state, and depending on the type of service.

Nationally, it costs about $6,300 a month for a home health aide and $9,700 for a private room in a nursing home for the typical person, according to 2023 data from Genworth, an insurer.

It seems many households are unaware of the potential costs, either for themselves or their loved ones.

For example, 73% of workers say there’s at least one adult for whom they may need to provide long-term care in the future, according to a new poll by the Employee Benefit Research Institute.

However, just 29% of these future caregivers — who may wind up footing at least part of the future bill —had estimated the future cost of care, EBRI found. Of those who did, 37% thought the price tag would fall below $25,000 a year, the group said.

The EBRI survey polled 2,445 employees from ages 20 to 74 years old in late 2024.

Many types of insurance often don’t cover costs

Maskot | Maskot | Getty Images

There’s a good chance much of the funding for long-term care will come out-of-pocket, experts said.

Health insurance generally doesn’t cover long-term care services, and Medicare doesn’t cover most expenses, experts said.

For example, Medicare may partially cover “skilled” care for the first 100 days, said McClanahan, the founder of Life Planning Partners and a member of CNBC’s Financial Advisor Council. This may be when a patient requires a nurse to help with rehab or administer medicine, for example, she said.

Where is the money going to come from?

Bridget Bearden

research and development strategist at the Employee Benefit Research Institute

But Medicare doesn’t cover “custodial” care, when someone needs help with daily activities like bathing, dressing, using the bathroom and eating, McClanahan said. These basic everyday tasks constitute the majority of long-term care needs, according to the HHS-Urban report.

Medicaid is the largest payer of long-term care costs today, Bearden said. Not everyone qualifies, though: Many people who get Medicaid benefits are from lower-income households, EBRI’s Bearden said. To receive benefits for long-term care, households may first have to exhaust a big chunk of their financial assets.

“You basically have to be destitute,” McClanahan said.

Republicans in Washington are weighing cuts to Medicaid as part of a large tax-cut package. If successful, it’d likely be harder for Americans to get Medicaid benefits for long-term care, experts said.

Long-term care insurance considerations

The Good Brigade | Digitalvision | Getty Images

Few households have insurance policies that specifically hedge against long-term care risk: About 7.5 million Americans had some form of long-term care insurance coverage in 2020, according to the Congressional Research Service.

By comparison, more than 4 million baby boomers are expected to retire per year from 2024 to 2027.

Washington state has a public long-term care insurance program for residents, and other states like California, Massachusetts, Minnesota, New York and Pennsylvania are exploring their own.

Long-term care insurance policies make most sense for people who have a high risk of needing care for a lengthy duration, McClanahan said. That may include those who have a high risk of dementia or have longevity in their family history, she said.

McClanahan recommends opting for a hybrid insurance policy that combines life insurance and a long-term care benefit; traditional stand-alone policies only meant for long-term care are generally expensive, she said.

Be wary of how the policy pays benefits, too, she said.

For example, “reimbursement” policies require the insured to choose from a list of preferred providers and submit receipts for reimbursement, McClanahan said. For some, especially seniors, that may be difficult without assistance, she said.

With “indemnity” policies, which McClanahan recommends, insurers generally write benefit checks as soon as the insured qualifies for assistance, and they can spend the money how they see fit. However, the benefit amount is often lower than reimbursement policies, she said.

How to be proactive about long-term care planning

“The challenge with long-term care costs is they’re unpredictable,” McClanahan said. “You don’t always know when you’ll get sick and need care.”

The biggest mistake McClanahan sees people make relative to long-term care: They don’t think about long-term care needs and logistics, or discuss them with family members, long before needing care.

For example, that may entail considering the following questions, McClanahan said:

- Do I have family members that will help provide care? Would they offer financial assistance? Do I want to self-insure?

- What are the financial logistics? For example, who will help pay your bills and make insurance claims?

- Do I have good advance healthcare directives in place? For example, as I get sicker will I let family continue to keep me alive (which adds to long-term care expenses), or will I move to comfort care and hospice?

- Do I want to age in place? (This is often a cheaper option if you don’t need 24-hour care, McClanahan said.)

- If I want to age in place, is my home set up for that? (For example, are there many stairs? Is there a tiny bathroom in which it’s tough to maneuver a walker?) Can I make my home aging-friendly, if it’s not already? Would I be willing to move to a new home or perhaps another state with a lower cost of long-term care?

- Do I live in a rural area where it may be harder to access long-term care?

Being proactive can help families save money in the long term, since reactive decisions are often “way more expensive,” McClanahan said.

“When you think through it in advance it keeps the decisions way more level-headed,” she said.

Pilotless planes are taking flight in China. Bank of America says it's time to buy

Student loan borrowers brace for wage garnishment

Best Practices to Auditing Your Bookkeeping Records

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Personal Finance1 week ago

Personal Finance1 week agoHow consumers prepare for an economic hit

-

Personal Finance1 week ago

Personal Finance1 week agoReal estate and gold vs. stocks: Best long-term investment

-

Economics1 week ago

Economics1 week agoAndrew Bailey on why UK-U.S. trade deal won’t end uncertainty

-

Economics1 week ago

Economics1 week agoTrump knocks down a controversial pillar of civil-rights law

-

Economics1 week ago

Economics1 week agoA social history of America in a warehouse

-

Accounting1 week ago

Accounting1 week agoEssential Strategies for Maintaining Data Security in Modern Bookkeeping

-

Economics1 week ago

Economics1 week agoHarvard has more problems than Donald Trump

-

Finance1 week ago

Finance1 week agoAmerica failing its young investors, warns financial guru Ric Edelman