Finance

Klarna scores payment deal with Uber ahead of anticipated IPO

The Swedish “buy now, pay later” pioneer said Tuesday that its new design would help users find the items they want by using more advanced AI recommendation algorithms, while merchants will be able to target customers more effectively.

Rafael Henrique | SOPA Images | LightRocket via Getty Images

Klarna on Wednesday announced a global partnership with Uber to power payments for the ride-hailing giant’s Uber and Uber Eats apps.

The partnership will see the Swedish financial technology firm added as a payment option in the U.S., Germany and Sweden, Klarna said in a statement.

In those countries, Klarna will roll out its “Pay Now” option in the two apps, which lets customers pay off an order instantly in one click. Users will be able to track all their Uber purchases in the Klarna app.

The company will also offer an additional payment option for Uber users in Sweden and Germany, allowing users to bundle purchases into a single, interest-free payment that gets removed from their monthly salary.

Interestingly, the company isn’t rolling out installment-based “buy now, pay later” plans, arguably Uber’s most popular service offering, on its platforms.

Sebastian Siemiatkowski, CEO and co-founder of Klarna, said in a statement Wednesday that the deal represented a “significant milestone” for the company.

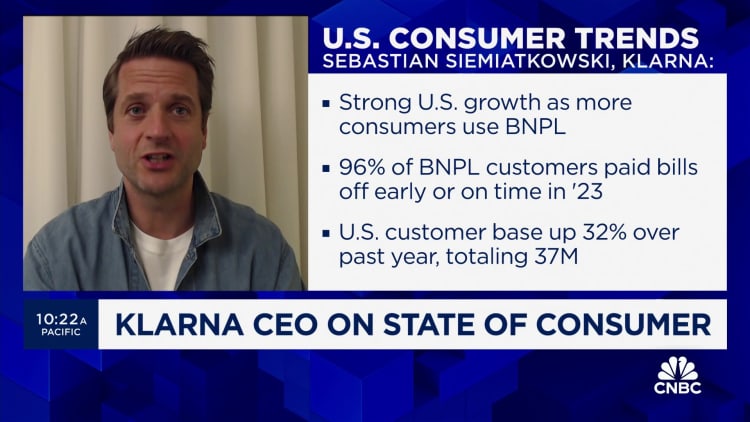

“Consumers can Pay Now quickly and securely in full, which already accounts for over one third of Klarna’s global volumes, and more easily manage their finances in one place,” Siemiatkowski said.

Klarna declined to disclose the financial terms of its deal with Uber.

Big pre-IPO merchant win

The Uber deal marks one of the most significant merchant wins for Klarna as of late and comes as the European fintech giant is rumored to be gearing up for a blockbuster initial public offering that could value the firm at just north of $20 billion.

Klarna began having detailed discussions with investment banks to work on an IPO that could happen as early as the third quarter, Bloomberg News reported in February, citing unnamed sources familiar with the matter.

CNBC could not independently verify the accuracy of the report. Klarna has said that it doesn’t comment on market speculation.

Such a market flotation would mark a turnaround for a company that saw $38.9 billion erased from its valuation in 2022 when deteriorating macroeconomic conditions stoked by Russia’s invasion of Ukraine caused a reset of sky-high tech valuations.

Klarna reached an eye-watering $45.6 billion in a 2021 funding round led by SoftBank, before seeing its market value fall to $6.7 billion the following year in a so-called “down round.”

The firm recently launched a monthly subscription plan in the U.S. to lock in “power users” ahead of its anticipated IPO.

The product is called Klarna Plus and costs $7.99 per month. Klarna Plus enables users to get service fees waived, earn double rewards points and access curated discounts from partners, such as Nike and Instacart.

Last year, Klarna reported its first quarterly profit in four years after cutting its credit losses by 56%.

The company posted an operating profit of 130 million Swedish krona (roughly $11.7 million) in the third quarter of 2023, swinging to a profit for a loss of 2 billion Swedish krona (roughly $183.6 million) in the same period a year earlier.

Buy now, pay later boom

Klarna is one of many “buy now, pay later” services that allow users to pay off their purchases over a period of monthly installments.

The payment method has become increasingly popular among consumers who are making online and in-person shopping purchases. It also can be an alternative to credit cards charging interest and high fees.

However, it has also stoked concerns about the affordability of such services, and whether it is in fact encouraging some consumers — particularly younger people — to spend more than they can afford.

In the U.K., the government has proposed draft laws to regulate the “buy now, pay later” industry.

The U.S. Consumer Financial Protection Bureau has previously said that it plans to subject “buy now, pay later” lenders to the same oversight as credit card companies.

Meanwhile, the European Union last year passed a revised version of its Consumer Credit Directive to include “buy now, pay later” services under the scope of the rules.

For its part, Klarna has defended the “buy now, pay later” model, arguing that it offers customers a cheaper way to access credit compared with traditional credit cards and consumer loans.

The company also said it welcomes regulation of “buy now, pay later” products.

The AICPA’s Mark Koziel: More upside than downside for accountants

Instead adds AI-driven tax reports

Half of accountants expect firms to shrink headcount by 20%

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Blog Post1 week ago

Blog Post1 week agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Personal Finance1 week ago

Personal Finance1 week agoWhat the national debt, deficit mean for your money

-

Personal Finance1 week ago

Personal Finance1 week agoHow to save on summer travel in 2025

-

Personal Finance1 week ago

Personal Finance1 week agoDenmark raises retirement age to 70; U.S. might follow

-

Finance1 week ago

Finance1 week agoWhy JPMorgan hired NOAA’s Sarah Kapnick as chief climate scientist

-

Economics1 week ago

Economics1 week agoPeople cooking at home at highest level since Covid, Campbell’s says

-

Economics1 week ago

Economics1 week agoElon Musk’s failure in government

-

Economics4 days ago

Economics4 days agoJobs report May 2025: