Finance

Private student loan interest rates spike for 5- and 10-year loans

Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as “Credible” below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

The latest private student loan interest rates from the Credible marketplace, updated weekly. (iStock)

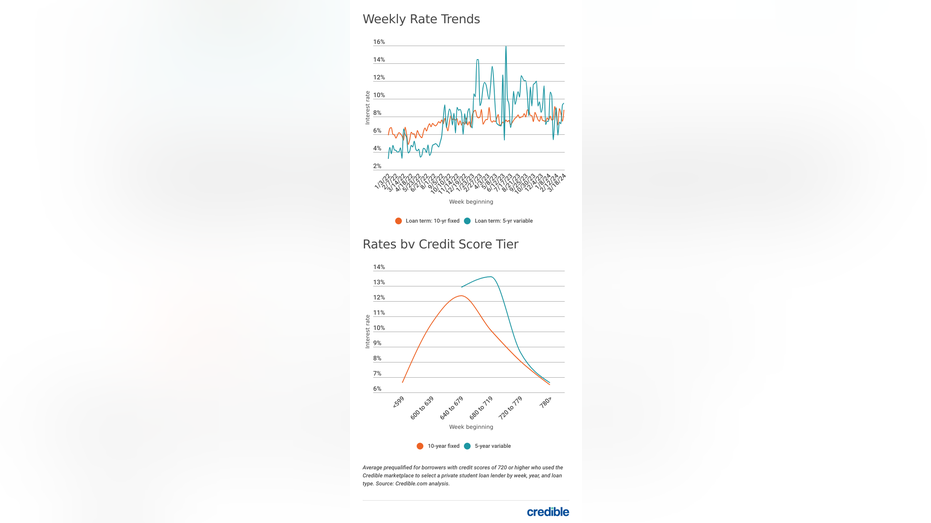

During the week of Mar. 18, 2024, average private student loan rates increased for borrowers with credit scores of 720 or higher who used the Credible marketplace to take out 10-year fixed-rate loans and 5-year variable-rate loans.

- 10-year fixed rate: 8.77%, up from 7.50% the week before, +1.27

- 5-year variable rate: 9.54%, up from 9.29% the week before, +0.25

Through Credible, you can compare private student loan rates from multiple lenders.

For 10-year fixed private student loans, interest rates soared by over one and a quarter percentage points, while 5-year variable student loan interest rates edged up by a quarter of a percentage point.

Borrowers with good credit may find a lower rate with a private student loan than with some federal loans. For the 2023-24 academic school year, federal student loan rates will range from 5.50% to 8.05%. Private student loan rates for borrowers with good to excellent credit can be lower right now.

Because federal loans come with certain benefits, like access to income-driven repayment plans, you should always exhaust federal student loan options first before turning to private student loans to cover any funding gaps. Private lenders such as banks, credit unions, and online lenders provide private student loans. You can use private loans to pay for education costs and living expenses, which might not be covered by your federal education loans.

Interest rates and terms on private student loans can vary depending on your financial situation, credit history, and the lender you choose.

Take a look at Credible partner lenders’ rates for borrowers who used the Credible marketplace to select a lender during the week of March 18:

Private student loan rates (graduate and undergraduate)

Who sets federal and private interest rates?

Congress sets federal student loan interest rates each year. These fixed interest rates depend on the type of federal loan you take out, your dependency status and your year in school.

Private student loan interest rates can be fixed or variable and depend on your credit, repayment term and other factors. As a general rule, the better your credit score, the lower your interest rate is likely to be.

You can compare rates from multiple student loan lenders using Credible.

How does student loan interest work?

An interest rate is a percentage of the loan periodically tacked onto your balance — essentially the cost of borrowing money. Interest is one way lenders can make money from loans. Your monthly payment often pays interest first, with the rest going to the amount you initially borrowed (the principal).

Getting a low interest rate could help you save money over the life of the loan and pay off your debt faster.

What is a fixed- vs. variable-rate loan?

Here’s the difference between a fixed and variable rate:

- With a fixed rate, your monthly payment amount will stay the same over the course of your loan term.

- With a variable rate, your payments might rise or fall based on changing interest rates.

Comparison shopping for private student loan rates is easy when you use Credible.

Calculate your savings

Using a student loan interest calculator will help you estimate your monthly payments and the total amount you’ll owe over the life of your federal or private student loans.

Once you enter your information, you’ll be able to see what your estimated monthly payment will be, the total you’ll pay in interest over the life of the loan and the total amount you’ll pay back.

About Credible

Credible is a multi-lender marketplace that empowers consumers to discover financial products that are the best fit for their unique circumstances. Credible’s integrations with leading lenders and credit bureaus allow consumers to quickly compare accurate, personalized loan options – without putting their personal information at risk or affecting their credit score. The Credible marketplace provides an unrivaled customer experience, as reflected by over 4,300 positive Trustpilot reviews and a TrustScore of 4.7/5.

Finance

Trump says ‘extremely hard’ to make a deal with China’s Xi as trade stalemate fuels calls for leaders to talk

Jack Otter and the ‘Barron’s Roundtable’ panelists share their best tips for how to prepare for retirement amid a market concerned with tariffs.

Retirement account balances dipped in the first quarter due to stock market turbulence. Still, people kept socking away money for their retirement, according to new data from Fidelity Investments.

The financial services company analyzed more than 50 million retirement accounts, finding that the average balances of 401(k), IRA and 403(b) accounts all saw small declines during the first three months of 2025.

The average 401(k) account balance decreased 3% quarter over quarter to $127,100, according to Fidelity Investment’s Q1 2025 retirement analysis.

IRA accounts had average balances of $121,983 and 403(b) accounts held $115,424 on average in the first quarter, 4% and 2% lower than the prior quarter, respectively.

THIS MIDWESTERN STATE IS CONSIDERED ONE OF THE BEST PLACES TO RETIRE, NEW STUDY SAYS: SEE THE LIST

Fidelity largely attributed those declines to “market swings.”

The market was turbulent during the first quarter amid uncertainty surrounding tariffs and other policy issues, including popular index funds.

Still, retirement savings rates “stayed consistently high,” according to Fidelity.

For 401(k) accounts, employee contribution rates hit 9.5% during the first quarter, with the employer contribution rate coming in at 4.8%, according to its analysis.

Combined, the 14.3% savings rate for 401(k) accounts marked a “record” and the “closest it’s ever been to Fidelity’s suggested savings rate of 15%,” the company said.

RETIREMENT PLANNING: THE DIFFERENCES BETWEEN A TRADITIONAL AND ROTH IRA

Holders of 403(b) accounts, meanwhile, had a rate of 11.8% on average.

“Although the first quarter of 2025 posed challenges for retirement savers, it’s encouraging to see people take a continuous savings approach which focuses on their long-term retirement goals,” Sharon Brovelli, president of workplace investing at Fidelity, said in a statement. “This approach will help individuals weather any type of market turmoil and stay on track to reach their retirement goals.”

During the first quarter, which was plagued with market volatility, 17.4% of 401(k) holders upped the size of their contributions, while only 4.9% lowered theirs, the report found.

Meanwhile, contribution rates among 14.6% of 403(b) holders went up in the first quarter.

Only a small percentage of people with those types of retirement plans altered their asset allocation during the first quarter, with just 6% of 401(k) users doing so and 4.7% for 403(b), it found.

NEARLY HALF OF GENERATION X IS NOT CONFIDENT ABOUT RETIREMENT, SURVEY FINDS

Fidelity’s analysis also showed that people with IRAs upped the amount of money that they put in those retirement accounts in the first quarter by 4.5% compared to 2024’s first quarter.

A separate survey released Monday by Gallup found 59% of U.S. adults have funds put away in a retirement savings account.

Among those with retirement savings plans that have not yet left the workforce, half reported they “expect to have enough to live comfortably in retirement,” according to Gallup.

Trump bill unlikely to repeal estate tax, Senate leader says

Average 401(k) savings rate hits a record high. See if you’re on track

Progress, long lines and fisticuffs highlight TIGTA report on IRS

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Economics1 week ago

Economics1 week agoMAGA: protecting the homeland from Canadian bookworms

-

Accounting1 week ago

Accounting1 week agoHighest paid jobs in corporate accounting

-

Economics1 week ago

Economics1 week agoElon Musk says Trump’s spending bill undermines the work DOGE has been doing

-

Economics1 week ago

Economics1 week agoHow young voters helped to put Trump in the White House

-

Personal Finance1 week ago

Personal Finance1 week agoHarvard, Trump international enrollment battle affects college applicants

-

Blog Post4 days ago

Blog Post4 days agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics5 days ago

Economics5 days agoWhy the president must not be lexicographer-in-chief

-

Personal Finance1 week ago

Personal Finance1 week agoCrypto in 401(k) plans: Trump administration eases rules