Accounting

Tax Fraud Blotter: Severe and widespread

Speedy decision; trouble in paradise; diplomatic imbecility; and other highlights of recent tax cases.

Waxahachie, Texas: Tax preparer Bachary Rushid McGruder, 45, has been sentenced to three years in prison and ordered to pay more than $6.7 million in restitution to the IRS.

McGruder, owner of M&M Enterprises and Consulting, pleaded guilty in November to aiding and assisting in the preparation of false returns.

During tax years 2015 through 2018, he prepared more than 1,000 fraudulent returns for clients, using fictitious Schedule A deductions such as gifts to charity, unreimbursed employee expenses and home mortgage interest, false Schedule C business losses and false residential energy credits. He included the statements on returns without clients’ knowledge and had clients sign forms justifying the deductions and credits without explaining the forms’ contents.

McGruder charged exorbitant fees that were deducted from the refunds — as much as $2,800 for preparing a return.

The fraud resulted in a tax loss of $6.73 million.

Detroit: A federal court has permanently barred Annetta Powell and her seven tax prep-related businesses — Alliance Tax Services, Nationwide Tax Services, Tax Expert Stores, United Tax Services, Top Financial Specialists, United Financial Team Corporation and Speedy Tax Stores Corp. — from preparing federal returns for others and from owning or operating a prep business.

According to the court’s order, Powell, through her companies, operated up to five tax prep stores in Detroit and in Pontiac and Flint, Michigan, first under the name The Tax Experts and then, since 2021, under Speedy Tax Stores. The court found that the “harm caused by defendants’ fraudulent tax preparation scheme was severe and widespread, occurring across five stores for nearly a decade.” The court concluded that the defendants “prepared too many fraudulent tax returns with similar issues … for the pattern to have been random.”

The court noted that Powell refused to cooperate with the IRS investigation and took active steps to thwart the investigation by altering clients’ files and returns and manipulating the use of an EFIN. She could not obtain an EFIN because of her criminal record, so her stores used EFINs under someone else’s name. This misconduct, along with other past fraudulent conduct, led the court to determine that Powell “would likely find new ways to prepare fraudulent returns” if she were not permanently barred.

The court also ordered the defendants to disgorge $689,797.91 to the U.S., representing the ill-gotten gains from 2019 through 2021.

Honolulu: Former resident Sook Young Jung has pleaded guilty to conspiring to defraud the IRS by fraudulently obtaining a refund and then thwarting efforts by the agency to recoup it.

Jung conspired to file a false 2015 individual income tax return in her name. Jung’s co-conspirators created a fake tax form purportedly issued by a mortgage lender, which Jung attached to her return. The form falsely reported that Jung withheld more than $1.7 million in taxes. As a result, the IRS paid Jung a refund of $1,147,036.

After filing the false return and submitting the fake form, Jung tried to prevent the IRS from recovering the refund. For example, she deposited the refund check into a newly opened bank account and immediately withdrew most of the funds in cashier’s checks. She also paid, through nominees, one of her co-conspirators $500,000 for the co-conspirator’s assistance in obtaining the fraudulent refund.

Jung faces up to five years in prison as well as a period of supervised release, restitution and monetary penalties.

Rochester, New York: Resident Melanie Armstrong has pleaded guilty to wire fraud involving national emergency benefits, filing false claims against a government agency and transfer of a means of identification.

Between July 2020 and August 2021, Armstrong falsely applied for state unemployment benefits under the identities of others and fraudulently collected benefits in their names. She also collected unemployment benefits in her own name by falsely representing that she had no source of income. Armstrong received $131,400.10 in benefits unlawfully. She also applied for but did not receive additional benefits, resulting in a total intended loss of $250,916.

Between January 2019 and April 2023, Armstrong filed 19 false federal income tax returns for herself, family members and associates claiming false and inflated wages and false and inflated federal income tax withholdings. The IRS issued refunds to Armstrong and to others totaling $101,255.

Between January 2020, and April 2023, she also filed 17 false returns for herself, family members and associates with the New York State Department of Taxation and Finance, claiming false and inflated wages and false and inflated state income tax withholdings. Armstrong attempted to obtain $45,363 in fraudulent refunds but received only $18,758.

The charges carry a maximum of 30 years in prison and a $1 million fine.

Albuquerque, New Mexico: Resident Arturo Archuleta, 50, has been sentenced to two years in prison for tax evasion.

Between 2014 and 2018, Archuleta was the office manager for a chiropractic practice. During that time, he failed to report more than $200,000 in income to the IRS and diverted more than $500,000 in payments to the practice to a nominee bank account that he controlled; he did not report that income to the IRS.

Archuleta, who pleaded guilty in May, paid some $140,000 in outstanding tax obligations to the IRS before sentencing. He was also ordered to pay some $90,000 in restitution to Medicaid for expenses covered by Medicaid while he was evading income tax.

The judge also imposed a fine of $75,000 and ordered Archuleta to perform 100 hours of community service after he is released from prison and to enroll in a state self-exclusion program for gambling.

Houston: Jonathan Louis Lepow, manager of his father’s dental practice, has pleaded guilty for failing to pay taxes withheld from employee wages.

Jonathan Louis Lepow managed the clinic Kenneth A. Lepow DDS Inc., which had some 51 employees from 2015 to 2017. He was involved in financial decision-making at the clinic and oversaw accounting for and paying federal employment taxes. Lepow admitted that during the first quarter of 2015 he failed to pay $544,272 in IRS trust fund taxes collected from employees.

Lepow used the money to pay vendors and transferred funds to accounts of other entities he was establishing.

He has agreed to repay $495,847.

Urbana, Illinois: A jury has returned guilty verdicts on three offenses against Larry Dean Gibbs, of Pembroke Township, Illinois, for filing false federal returns.

In January 2017, Gibbs filed three federal income tax returns for the tax years 2012, 2013 and 2014, each falsely claiming that he had earned $10 million in annual income from the “Larry Dean Gibbs Estate.” He further claimed that the IRS withheld more than $3 million annually from his earnings and that he was entitled to refunds totaling more than $6.8 million.

Gibbs also claimed that he had changed his name to Mulumbua Humraukn El Taikem Bey and that he was the ambassador for the Al Moroccan Empire National Republic, which is not officially recognized by the U.S. At the time Gibbs filed the three false returns, he had just been released from prison for a prior conviction for filing a false federal tax return in 2005, when he had obtained an undeserved $66,282 refund.

Sentencing is July 17. Gibbs faces up to three years in prison and a $100,000 fine on each of the three counts.

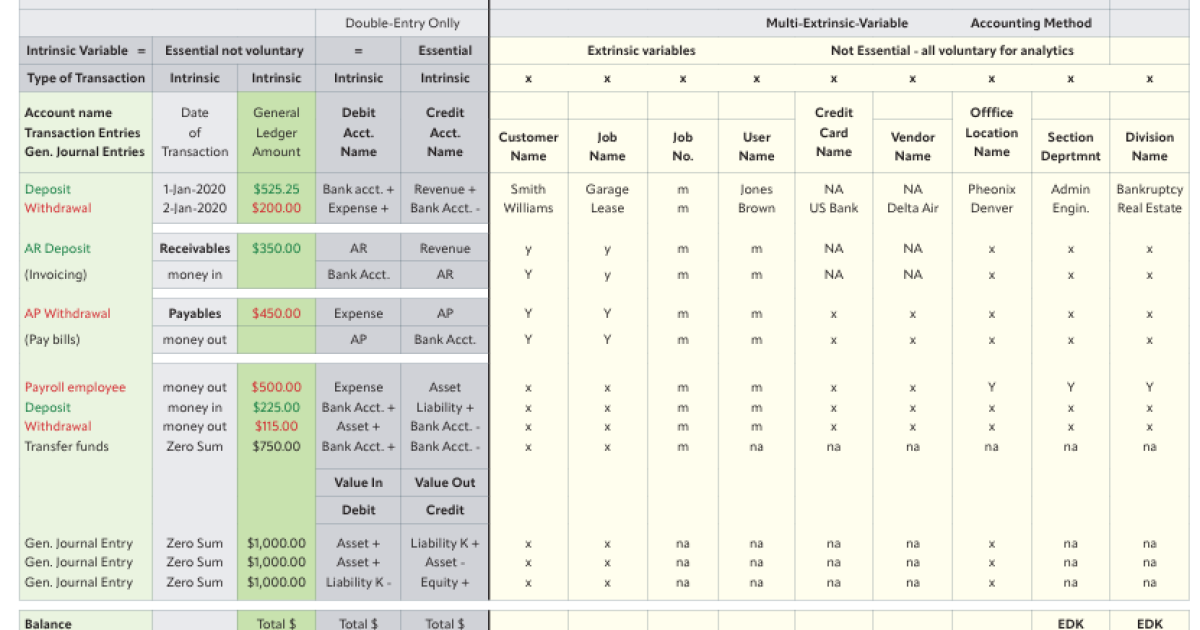

Edward Kellman, CEO and chief design engineer of Trakker Apps, holds two U.S. patents for an innovative take on double-entry accounting

The system, known as the Double-Entry Multi-Extrinsic-Variable Accounting Method Database, aims to modernize financial tracking while preserving the essence of the traditional accounting system that was first described by Luca Pacioli back in 1494. It leverages artificial intelligence while generating and reconciling multiple financial ledgers by account, user, customer, job and vendor.

“I made a representation of the current double entry database, which basically collects a date, amount, a debit and a credit account, and that’s about as much of that calculation as you can do by hand,” said Kellman. “It’s been done by hand for hundreds of years. It’s very tedious, but nobody ever thought to expand the database now that you can use a computer to solve for these enormously complex database solutions.”

He expanded the database with new variables, which he calls extrinsic variables, and now it can track financial transactions by customer, job, user and vendor. “By doing that, I’ve created an enormous amount of new financial solutions that can be plucked from the database that never existed, and these are all financial analytics for your company, because the variables are the things that matter in your company: which jobs make the most money, which users produce the most income and expenses, and things of this nature,” said Kellman. “But because I expanded that database, and nobody thought to do this since 1494 when this system was first published. It’s totally modernized double entry accounting.”

He offers them as apps that can be downloaded from the Apple and Android app stores, along with a browser-based version through the

The system leverages artificial intelligence to automate data entry. “I didn’t want it to become a tedious process for entering data, so we basically wrote these AI data entry algorithms that collect the data and fill in the data when it knows it right away,” said Kellman. “You can enter these transactions really just as quickly, if not quicker, on a smartphone than you can on any other accounting system, because of the data entry algorithms that just collect the data really quickly. And once you hit Enter and record that transaction, that’s all stored in the cloud. All your business is digitized.”

He did beta testing for a year on the app stores, where the program had around 6,000 downloads. But then he shut down the program because he didn’t want to be the cloud host responsible for storing thousands of people’s financial data so he is searching for a banking partner to host it securely. The system provides a kind of ERP platform that combines banking and accounting.

“Instead of printing profit and loss reports and balance sheet reports and trial balance summary reports just for the whole company, I can print them individually, for each individual user or each individual job,” said Kellman. “Or if you have multiple users, like in a law firm on one job, you can select the job and the user and print just the transactions that apply to those variables that you’ve selected, and now you’ve got a wealth of information about your company that never existed before.”

Trakker Apps’ BaaS fintech platform includes Business Trakker, Invoice 4 Business, Expense Trakker, Balance Sheet Trakker and Escrow Trakker for Lawyers.

It took four years before Kellman was able to patent the technology. “Normally, when you apply for a patent, they spend a lot of time on a patent search, where they investigate all the previous patents to see if you’re in violation of any other patents, or any other art that exists,” he said. “My patents are the only patents ever issued for a double entry accounting system, and there was no prior art. It took about four years to get it, and then I got a second one after that.”

Kellman isn’t planning to challenge other accounting software companies now that he has the

The Committee of Sponsoring Organizations of the Treadway Commission and the National Association of Corporate Directors have released an

Last May,

The Corporate Governance Framework is designed to complement and align with COSO’s longstanding Internal Control and Enterprise Risk Management frameworks. It includes practices to help organizations improve their governance effectiveness, manage risks proactively and create long-term value. COSO is jointly sponsored by the American Accounting Association, the American Institute of CPAs, Financial Executives International, the Institute of Management Accountants and the Institute of Internal Auditors.

“Resilient and well-structured corporate governance is the foundation of trust in capital markets, ethical business practices, and sustainable financial performance,” said COSO executive director and chair Lucia Wind in a statement Tuesday. “This framework provides organizations with a structured yet flexible approach to governance, ensuring they can navigate today’s complex regulatory and risk landscape with confidence, enable organizational effectiveness, while building long term value for its shareholders.”

Public comments will be accepted until July 11, 2025. The

COSO and the NACD are encouraging a holistic approach to defining corporate governance, extending beyond the boardroom to encompass the practices, information channels, and processes that govern how an entity is being directed, managed and controlled.

“Strong corporate governance creates a competitive advantage for organizations of all sizes, stages of maturity, and growth strategies,” said NACD president and CEO Peter Gleason in a statement. “This framework will help boards and management align on the importance and scope of governance in a time of tremendous complexity and disruption. When adapted to fit an organization’s specific needs, the framework will help drive better business outcomes and higher-quality board and management performance.”

COSO and the NACD see corporate governance as involving the oversight and processes by which an informed board and management team steers an entity toward executing its strategies and goals while maximizing long-term shareholder value in an ethical manner and within the relevant legal and regulatory environment.

“By providing a common language and practical guidance, it empowers boards, management, and employees to work together in building resilient, accountable organizations that can adapt, compete, and deliver long-term value to shareholders and other key stakeholders,” said Lillian Borsa and Brian Schwartz, PwC US principals and co-leads of the COSO Corporate Governance Framework, in a joint statement.

Elon Musk expressed dissatisfaction with President Donald Trump’s giant tax bill, saying it undercut his efforts to slash government spending.

Musk, who has announced he’s stepping back from his Department of Government Efficiency — a body that quickly became an exponent of the second Trump administration’s vision — told CBS News in an interview that he was “disappointed to see the massive spending bill, frankly, which increases the budget deficit, not just decreases it, and undermines the work that the DOGE team is doing.”

The legislation, which Trump calls his “big, beautiful bill” and includes an array of tax cuts, will go to the Senate after it narrowly passed the House last week. Musk, the billionaire chief executive officer of Tesla Inc. and SpaceX, seemed to echo the concerns of some Republicans in the House and Senate who believe the legislation costs too much and demand more spending reductions.

“We are so far away from an acceptable bill, it’s hard to say,” said Senator Ron Johnson, a Wisconsin Republican, when asked when his chamber could complete its work.

Other Republicans, however, not only oppose further cuts, but object to provisions already in the House version, such as restricting Medicaid benefits and the swift elimination of clean-energy tax incentives.

“I think a bill can be big or it can be beautiful,” Musk said in an excerpt of the interview released on Tuesday night before its broadcast on CBS Sunday Morning this weekend. “But I don’t know if it can be both. My personal opinion.”

Inventor patents variation on double-entry accounting

Palantir teams up with Fannie Mae in AI push to sniff out mortgage fraud

Fed worried it could face ‘difficult tradeoffs’ if tariffs reaggravate inflation, minutes show

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Accounting6 days ago

Accounting6 days agoHouse tax bill includes provision eliminating PCAOB

-

Economics1 week ago

Economics1 week agoWhat happens if the Inflation Reduction Act goes away?

-

Personal Finance6 days ago

Personal Finance6 days agoWhat House Republican ‘big beautiful’ budget bill means for your money

-

Accounting6 days ago

Accounting6 days agoTrump tax bill faces Senate’s arcane rules, desire for changes

-

Economics1 week ago

Economics1 week agoJoe Biden did not decline alone

-

Finance5 days ago

Finance5 days agoPersonal finance app Monarch raises $75 million

-

Economics6 days ago

Economics6 days agoCalifornia has got really good at building giant batteries

-

Economics6 days ago

Economics6 days agoHow much worse could America’s measles outbreak get?