Finance

This week’s personal loan rates fall for 3- and 5-year terms

Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as “Credible” below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

The latest trends in interest rates for personal loans from the Credible marketplace, updated weekly. (iStock)

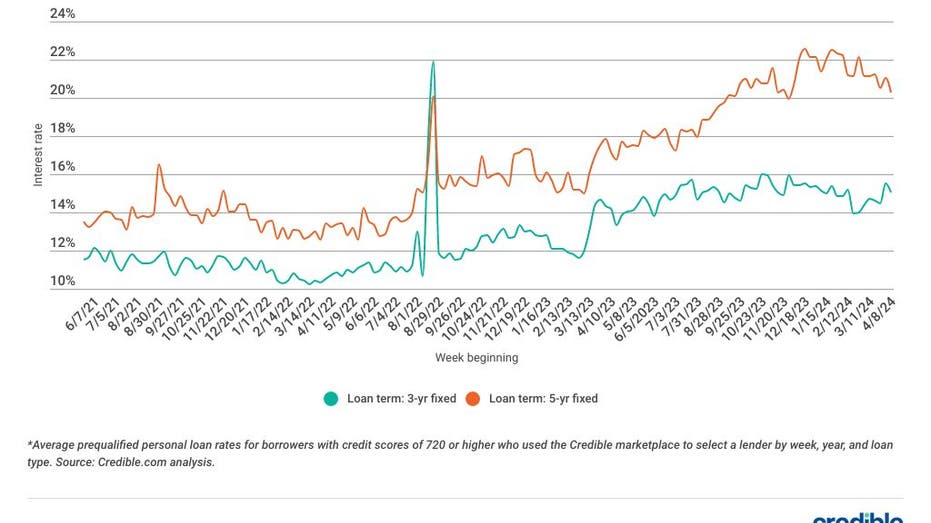

Borrowers with good credit seeking personal loans during the past seven days prequalified for rates that were higher for 3-year loans and lower for 5-year loans when compared to fixed-rate loans for the seven days before.

For borrowers with credit scores of 720 or higher who used the Credible marketplace to select a lender between April 8 and April 15:

- Rates on 3-year fixed-rate loans averaged 15.04%, down from 15.52% the seven days before and up from 14.51% a year ago.

- Rates on 5-year fixed-rate loans averaged 20.28%, down from 21.04% the previous seven days and up from 17.29% a year ago.

Personal loans have become a popular way to consolidate debt and pay off credit card debt and other loans. They can also be used to cover unexpected and emergency expenses like medical bills, take care of a major purchase, or fund home improvement projects.

Average personal loan interest rates

Average personal loan interest rates decreased over the last seven days for 3- and 5-year loans. While 3-year loan rates fell by 0.48 percentage points, rates on 5-year loans fell by 0.76 percentage points. Interest rates for both terms remain significantly higher than they were this time last year, up 0.53 percentage points for 3-year terms and up 2.99 percentage points for 5-year terms.

Still, borrowers can take advantage of interest savings with a 3- or 5-year personal loan, as both loan terms offer lower interest rates on average than higher-cost borrowing options such as credit cards.

But whether a personal loan is right for you depends on multiple factors, including what rate you can qualify for, which is largely based on your credit score. Comparing multiple lenders and their rates helps ensure you get the best personal loan for your needs.

Before applying for a personal loan, use a personal loan marketplace like Credible to comparison shop.

Personal loan weekly rate trends

Here are the latest trends in personal loan interest rates from the Credible marketplace, updated weekly.

The chart above shows average prequalified rates for borrowers with credit scores of 720 or higher who used the Credible marketplace to select a lender.

For the month of March 2024:

- Rates on 3-year personal loans averaged 22.22%, up from 21.68% in February.

- Rates on 5-year personal loans averaged 24.38%, down from 24.88% in February.

Rates on personal loans vary considerably by credit score and loan term. If you’re curious about what kind of personal loan rates you may qualify for, you can use an online tool like Credible to compare options from different private lenders.

All Credible marketplace lenders offer fixed-rate loans at competitive rates. Because lenders use different methods to evaluate borrowers, it’s a good idea to request personal loan rates from multiple lenders so you can compare your options.

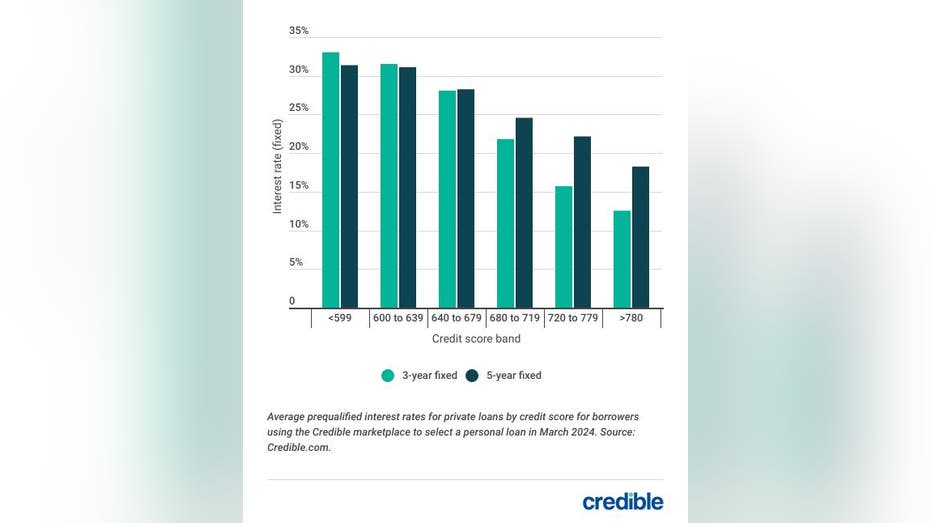

Current personal loan rates by credit score

In March, the average prequalified rate selected by borrowers was:

- 12.58% for borrowers with credit scores of 780 or above choosing a 3-year loan

- 31.39% for borrowers with credit scores below 600 choosing a 5-year loan

Depending on factors such as your credit score, which type of personal loan you’re seeking and the loan repayment term, the interest rate can differ.

As shown in the chart above, a good credit score can mean a lower interest rate, and rates tend to be higher on loans with fixed interest rates and longer repayment terms.

How to get a lower interest rate

Many factors influence the interest rate a lender might offer you on a personal loan. But you can take some steps to boost your chances of getting a lower interest rate. Here are some tactics to try.

Increase credit score

Generally, people with higher credit scores qualify for lower interest rates. Steps that can help you improve your credit score over time include:

- Pay bills on time: Payment history is the most important factor in your credit score. Pay all your bills on time for the amount due.

- Check your credit report: Look at your credit report to ensure there are no errors on it. If you find errors, dispute them with the credit bureau.

- Lower your credit utilization ratio: Paying down credit card debt can improve this important credit-scoring factor.

- Avoid opening new credit accounts: Only apply for and open credit accounts you actually need. Too many hard inquiries on your credit report in a short amount of time could lower your credit score.

Choose a shorter loan term

Personal loan repayment terms can vary from one to several years. Generally, shorter terms come with lower interest rates, since the lender’s money is at risk for a shorter period of time.

If your financial situation allows, applying for a shorter term could help you score a lower interest rate. Keep in mind the shorter term doesn’t just benefit the lender – by choosing a shorter repayment term, you’ll pay less interest over the life of the loan.

Get a cosigner

You may be familiar with the concept of a cosigner if you have student loans. If your credit isn’t good enough to qualify for the best personal loan interest rates, finding a cosigner with good credit could help you secure a lower interest rate.

Just remember, if you default on the loan, your cosigner will be on the hook to repay it. And cosigning for a loan could also affect their credit score.

Compare rates from different lenders

Before applying for a personal loan, it’s a good idea to shop around and compare offers from several different lenders to get the lowest rates. Online lenders typically offer the most competitive rates – and can be quicker to disburse your loan than a brick-and-mortar establishment.

But don’t worry, comparing rates and terms doesn’t have to be a time-consuming process.

Credible makes it easy. Just enter how much you want to borrow and you’ll be able to compare multiple lenders to choose the one that makes the most sense for you.

About Credible

Credible is a multi-lender marketplace that empowers consumers to discover financial products that are the best fit for their unique circumstances. Credible’s integrations with leading lenders and credit bureaus allow consumers to quickly compare accurate, personalized loan options – without putting their personal information at risk or affecting their credit score. The Credible marketplace provides an unrivaled customer experience, as reflected by over 6,500 positive Trustpilot reviews and a TrustScore of 4.7/5.

Finance

Stocks making the biggest moves midday: Brown-Forman, Five Below, Ciena, PVH, Planet Labs and more

Two graduate students research chemical products in a laboratory in Xiwangzhuang Town, Zaozhuang City, Shandong province of China, on Dec. 26, 2023.

Nurphoto | Nurphoto | Getty Images

BEIJING — For all the attention on U.S.-China competition in artificial intelligence, new studies point to China’s rapid rise in biotechnology, especially for drug and agricultural development.

Out of five critical tech sectors, “China has the most immediate opportunity to overtake the United States in biotechnology,” the Harvard Belfer Center for Science and International Affairs said Thursday in its release of a “Critical and Emerging Technologies Index,” covering AI, biotech, semiconductors, space and quantum.

While the U.S. is still the leader in all five, “the narrow U.S.-China gap [in biotech] suggests that future developments could quickly shift the global balance of power,” the report said.

The assessment echoes growing concerns in Washington. In fact, the U.S. National Security Commission on Emerging Biotechnology struck a more urgent tone in an April report, citing two years of research.

“There will be a ChatGPT moment for biotechnology, and if China gets there first, no matter how fast we run, we will never catch up,” the bipartisan Congressional commission said in the report, referring to the transformative chatbot released by U.S.-based OpenAI.

“Our window to act is closing. We need a two-track strategy: make America innovate faster, and slow China down,” the commission said. It recommends that the U.S. government spend at least $15 billion over the next five years to support the domestic biotech sector.

China’s biotech industry has evolved to the point that U.S. and European pharmaceutical giants in the last several months have spent billions to acquire China-developed drugs that could treat cancer if commercialized with regulatory approval. In March, British pharmaceutical giant AstraZeneca announced it will invest $2.5 billion in a research and development center in Beijing.

The Harvard Belfer Center pointed out that China’s biotech strengths stem from its “dominance in pharmaceutical production and manufacturing,” in addition to having more human talent than the U.S.

China also has a “more flexible regulatory regime and the ability to push things out faster,” Cynthia Y. Tong, one of the Harvard report’s authors, told CNBC in an interview Thursday. She noted that the U.S. tends to have a longer approval process, as well as more drawn out research and development period.

And just as China is developing its biotech sector, reports from the U.S. biotech hub of Cambridge and Boston are revealing layoffs and empty labs.

A big strategy

China has long used multi-year plans and preferential state policies to encourage the development of key technologies. Biotech is no different, gaining high-level support back in 2007.

“Currently, the U.S. government has no cohesive, intentional biotechnology strategy, while China is gaining ground thanks to its aggressive and carefully coordinated state-led initiatives,” the U.S. security commission said.

The worry is that just as Chinese restrictions on rare earths start to hit car manufacturers, Chinese dominance in biotech could become yet another form of leverage for Beijing over the U.S. and other countries.

“The likelihood there’s going to be cooperation [between the] U.S. and China on anything is very low, in some ways least likely on biotech and AI” because of the congressional report, said Eric Rosenbach, director of the defense, emerging technology, and strategy program at Harvard’s Belfer Center. He was chief of staff at the U.S. Department of Defense from 2015 to 2017.

He expects more U.S. pressure on China.

Subscribe now

It remains to be seen what that would mean in practice for businesses — though some say the future of biotech development is inherently global.

Insilico Medicine, a startup using AI to cut drug discovery costs, relies on a global team spread across China, North America and the Middle East, according to its founder and CEO Alex Zhavoronkov. On Tuesday, the company announced with a paper in Nature Medicine that it was the first to see successful clinical testing with an AI-discovered drug.

While Insilico’s AI work typically happens in Canada and Abu Dhabi, the chemical testing and experiments are done in China, Zhavoronkov said, adding that the head of clinical development is in Boston. He declined to comment on a commercialization timeline in light of conversations with regulators.

Other data shows that China has surpassed the U.S. in the number of clinical trials conducted, seen significant patent growth and boasts the most life sciences construction activity in the world.

China-based Capital O venture partner Yang Fan, who previously worked in the pharmaceutical industry, said he expects the best biotech companies of the future will navigate different countries’ regulations and use resources across the globe, if not benefit from arbitrage opportunities given different requirements and cost of entry in various markets.

“The Chinese market is like a big supermarket for anything that can be commoditized, AI or biotechnology,” he said, adding that new startups in China have to be “really good” to stand out. As AI drives innovation costs down, Fan predicts that in biotech, “the real DeepSeek moment is probably going to happen in five years.”

-

Blog Post5 days ago

Blog Post5 days agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics1 week ago

Economics1 week agoHow young voters helped to put Trump in the White House

-

Economics1 week ago

Economics1 week agoElon Musk says Trump’s spending bill undermines the work DOGE has been doing

-

Personal Finance1 week ago

Personal Finance1 week agoHarvard, Trump international enrollment battle affects college applicants

-

Accounting1 week ago

Accounting1 week agoHighest paid jobs in corporate accounting

-

Economics7 days ago

Economics7 days agoWhy the president must not be lexicographer-in-chief

-

Personal Finance1 week ago

Personal Finance1 week agoCrypto in 401(k) plans: Trump administration eases rules

-

Finance1 week ago

Finance1 week agoVail Resorts, GameStop and more