Accounting

What accounting firms can learn about talent management from tech vendors

In a

1. Embrace a meritocracy

A lesson that accounting firms can take from tech vendors is the value of a meritocratic culture, where top talent is promoted and given opportunities to excel based on performance, not tenure or seniority. This is a core value at successful technology companies: rewarding talent based on impact.

During my time working in Google’s finance team, I had the privilege of working with leaders like Sheryl Sandberg, the former COO of Facebook, and Sukhinder Singh Cassidy, the current CEO of Xero. One thing that stood out was their ability to make objective, impact-driven decisions when it came to promotions and talent management. They prioritized the greatest contributors and those who demonstrated the highest potential for the business, regardless of how long they had been at the company.

Historically, CPA practices have been seniority-driven, which worked well when there was a steady pipeline of accountants and workplace stability. But today’s reality is different. The number of new accountants entering the profession is dwindling, and those that do have a wide range of career options that go far beyond the traditional accounting partnership model. This was abundantly clear from a panel at Botkeeper’s conference AI Unchained, where we discussed alternative structures including accounting platforms, franchises and ESOPs.

As firm leaders, you might be concerned that this approach could cause friction among long-standing team members. After all, promoting a newer team member over someone who has been around longer can ruffle feathers. However, the alternative is riskier: If your top performers aren’t recognized or given opportunities to shine, they will leave. A-players attract A-players. Creating a culture where top performers are disengaged or overlooked can lead to talent loss, which is far more damaging in the long run. By embracing a meritocratic approach, you ensure that your firm’s future is powered by those who thrive in this current reality.

2. Make cross-training a foundation of your practice

In the tech world, wearing multiple hats is the norm. When I worked at Siri (yes, the iPhone assistant, which was eventually acquired by Apple), individuals with cross-functional skills were the norm, not the exception.

Engineers didn’t just code; they also created product designs. Product managers didn’t just product manage; they also handled parts of marketing. This kind of cross-training at tech vendors didn’t just build versatility in an era where agility is needed, it also fostered collaboration and innovation.

In accounting, cross-training can be just as impactful. For example, at the Botkeeper conference panel titled “Walking a Tightrope Between Evolving Technologies and Traditional Accounting” with Angie Grissom (Rainmaker), Geni Whitehouse (ITA) and Mike Maksymiw (Aprio Alliance), the group lamented how the accounting curriculum still doesn’t teach future CPAs data literacy or interpretation skills.

Imagine an accounting firm where every accountant is cross-trained in data analytics. Not only would this prepare them for the future, but it would also allow them to deliver higher-value services to clients. Instead of being confined to compliance work, these cross-trained accountants could provide strategic insights that help clients grow their businesses.

Cross-training doesn’t just benefit the firm’s services offerings — it engages and motivates employees. When team members are given the opportunity to develop new skills and wear different hats, they feel more valued and challenged. This sense of empowerment drives higher performance and fosters loyalty. Employees who feel like they are growing and expanding their skill set are far more likely to stay with a firm long-term. Cross-training offers them a sense of progress and personal investment in their career growth, which in turn increases their commitment to the firm.

3. Use both quantitative and qualitative feedback to manage talent

Tech vendors have long been applying business performance management principles to talent management. At my company Aiwyn, we regularly conduct pulse employee engagement surveys where team members rate their satisfaction across different vectors. We gather both qualitative and quantitative feedback, ensuring that we have a clear understanding of how employees feel, where they see room for improvement, and where they feel supported.

Accounting firms can adopt a similar approach. You wouldn’t run your business without tracking financial metrics, so why run your talent management program without tracking employee satisfaction? Regular pulse surveys, engagement metrics and feedback loops give you a real-time understanding of your team’s morale. This allows you to address issues before they become problems and ensure that your employees feel valued, heard and engaged.

Implementing KPIs for talent management helps you identify trends over time. Are certain teams consistently reporting low engagement scores? Is there a department where turnover is unusually high? By analyzing the data, you can take proactive steps to improve your workplace culture and retain top talent.

In conclusion, the traditional methods of managing talent for an accounting practice no longer align with the realities of today’s workplace. By taking lessons from tech vendors, firms can adopt a more meritocratic approach, make cross-training a core part of their culture, and use data-driven insights to improve employee engagement and retention.

Do you want to build a workplace that attracts top talent and helps your team thrive in an era of rapid technological change? By embracing these modern talent management strategies, you’ll position your firm to thrive in a rapidly changing world.

Enjoy complimentary access to top ideas and insights — selected by our editors.

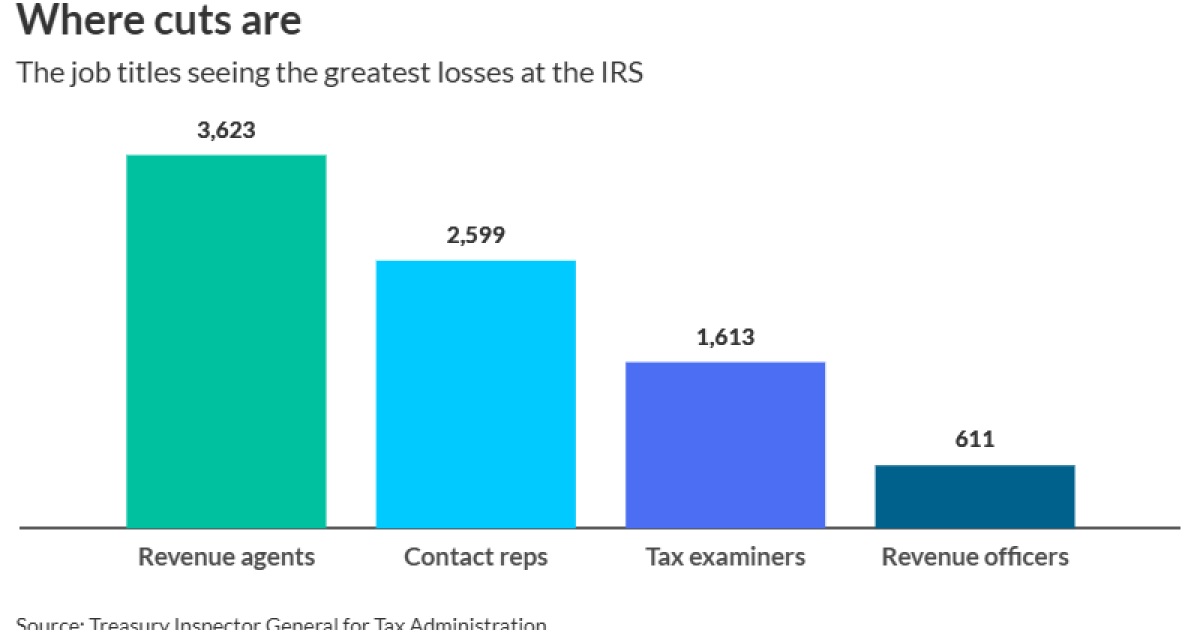

This week’s stats focus in part on the job titles seeing the greatest losses at the IRS during layoffs; as well as the states that have proposed or passed alternatives to the 150-hour rule; the percentage of master’s in accounting program applicants since 2020; the number of PwC employees laid off in May; the projected size of Deloitte’s new New York City headquarters; and the amount of 2026 HSA annual contribution limits, depending on coverage.

CrowdStrike Holdings Inc. said U.S. officials have asked for information related to the accounting of deals it’s made with some customers and said the cybersecurity firm is cooperating with the inquiry.

The Austin, Texas-based company said in a filing Wednesday that it has gotten “requests for information” from the U.S. Department of Justice and the Securities and Exchange Commission “relating to the company’s recognition of revenue and reporting of ARR for transactions with certain customers.” ARR refers to annual recurring revenue, a measure of earnings from subscriptions.

The company said the federal officials have also sought information related to a CrowdStrike update last year that crashed Windows operating systems around the world.

“The company is cooperating and providing information in response to these requests,” the filing states.

U.S. prosecutors and regulators have been investigating a $32 million deal between CrowdStrike and a technology distributor, Carahsoft Technology Corp., to provide cybersecurity tools to the Internal Revenue Service, Bloomberg News first reported in February. The IRS never purchased or received the products, Bloomberg News

The investigators are probing what senior CrowdStrike executives may have known about the $32 million deal and are examining other transactions made by the cybersecurity firm, Bloomberg News

Asked for comment about the filing, CrowdStrike spokesperson Brian Merrill said, “As we have told Bloomberg repeatedly, this is old news and we stand by the accounting of the transaction.”

A lawyer for Carahsoft previously declined to comment on the federal investigations, and representatives didn’t respond to subsequent requests for comment about them.

Tech titan Elon Musk ratcheted up his offensive against Donald Trump’s signature tax bill on Wednesday, urging that Americans contact their lawmakers to “KILL” the legislation.

“Call your Senator, Call your Congressman,” Musk wrote in a

The post came one day after Musk lashed out at the tax bill, describing it as a budget-busting “disgusting abomination” as Republican fiscal hawks stepped up criticism of the massive fiscal package.

Trump hasn’t publicly responded to Musk’s comments, but the White House put out a statement Wednesday saying the legislation “unleashes an era of unprecedented economic growth.”

And House Speaker Mike Johnson told reporters that Musk is “dead wrong” about the bill and that the tax cuts will pay for themselves through economic growth.

Musk’s public condemnation pits him against the president at a critical time as Trump is personally lobbying holdouts on the bill. His campaign against the legislation threatens to stiffen resistance and delay enactment of the tax cuts and debt ceiling increase.

Musk has attacked the legislation days after leaving a temporary assignment leading the administration’s Department of Government Efficiency initiative to cut federal spending. The Tesla Inc. chief executive officer’s high-profile role in the Trump administration eroded his business brand and sales of his company’s electric vehicles plunged.

The House-passed version of the tax and spending bill would add $2.4 trillion to U.S. budget deficits over the next decade, according to an

The CBO’s calculation reflects a $3.67 trillion decrease in expected revenues and a $1.25 trillion decline in spending over the decade through 2034, relative to baseline projections. The score doesn’t account for any potential boost to the economy from the bill, which Johnson and Trump argue would offset the revenue losses.

Musk, the world’s richest man with a net worth of about $377 billion according to the Bloomberg Billionaires Index, has become a crucial financial backer of the Republican party. After making modest donations most years, Musk became the biggest U.S. political donor in 2024, giving more than $290 million.

Johnson said Musk had promised to help reelect Republicans just a day before savaging Trump’s bill. Musk did not respond to a request for comment.

Most of Musk’s giving was aimed at electing Trump but he also supported congressional candidates. America PAC, the super political action committee that Musk largely funded, spent $18.5 million in 17 separate House races. Though that total pales in comparison to the roughly $255 million he spent backing Trump, the spending means a lot in a congressional election, where challengers on average raise less than $1 million.

Control of the House will likely be decided by the outcome of fewer than two dozen close races in the 2026 midterm elections. The GOP’s chances of holding their majority would suffer a major blow if Musk were to withdraw his financial support.

Personal finance expert tackles ‘widespread’ financial misconceptions

How to review your insurance policy

Accountants on IRS and PwC layoffs, accounting students and more

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Economics1 week ago

Economics1 week agoElon Musk says Trump’s spending bill undermines the work DOGE has been doing

-

Accounting1 week ago

Accounting1 week agoHighest paid jobs in corporate accounting

-

Blog Post5 days ago

Blog Post5 days agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics1 week ago

Economics1 week agoHow young voters helped to put Trump in the White House

-

Personal Finance1 week ago

Personal Finance1 week agoHarvard, Trump international enrollment battle affects college applicants

-

Economics6 days ago

Economics6 days agoWhy the president must not be lexicographer-in-chief

-

Personal Finance1 week ago

Personal Finance1 week agoCrypto in 401(k) plans: Trump administration eases rules

-

Finance1 week ago

Finance1 week agoVail Resorts, GameStop and more