Economics

Here’s what to expect from the April jobs report on Friday

A jobseeker takes a flyer at a job fair at Brunswick Community College in Bolivia, North Carolina, on April 11, 2024.

Allison Joyce | Bloomberg | Getty Images

Hiring likely continued at a brisk pace in April as investors look for any cracks in the labor market that could sway the Federal Reserve.

Nonfarm payrolls are expected to show a gain of 240,000 for the month, according to the Dow Jones consensus that also sees the unemployment rate holding steady at 3.8%.

If that top-line number is accurate, it actually would reflect a small step back from the average 276,000 jobs a month created so far in 2024. In addition, such growth could add to the Fed’s reluctance to lower interest rates, with the labor market humming along and inflation still above the central bank’s 2% target.

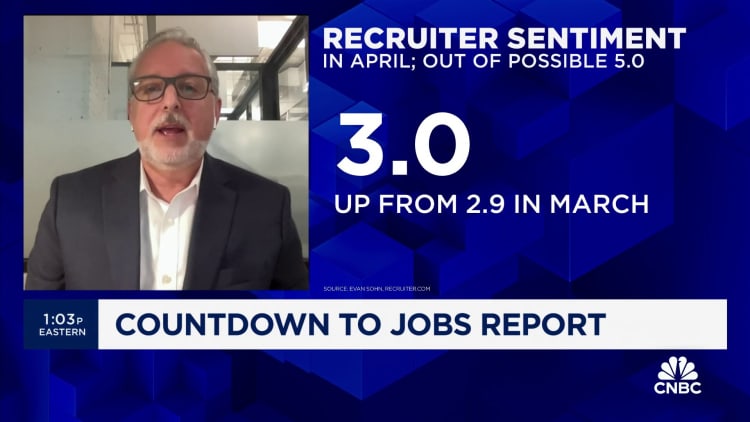

“There are definitely still tailwinds left,” said Amy Glaser, senior vice president of business operations at job staffing site Adecco. “For April, the name of the game is steady-Eddie as resiliency continues, and then we’re looking forward to some of the seasonal trends we would expect going into the summer.”

April’s jobs market featured more strength in health care and leisure and hospitality, Glaser added. Those have been two of the major sectors for employment growth this year, with health care adding about 240,000 jobs so far and leisure and hospitality contributing 89,000 jobs.

However, growth in the coming months could spread to areas such as education, manufacturing and warehousing, part of the usual seasonal trends as educators look for alternative employment in the summer and students head out seeking jobs, she said.

“I don’t expect to see major surprises this month based on what I’m seeing on the ground,” Glaser said. “But we’ve been surprised before.”

Beating expectations

Indeed, the labor market has been full of surprises this year, topping Wall Street estimates at a time when many economists expected hiring to have slowed down. The 303,000 gain in March shattered forecasts and were part of a glut of data showing that the labor economy remains strong, wages continue to rise and inflation has not moved much after receding sharply in 2023.

That has pushed the Fed into a box as officials are reluctant to start cutting interest rates until they get more convincing evidence that inflation is under control.

Policymakers will be watching several pieces in tomorrow’s report for evidence that job growth is not helping fuel price pressures.

If the payrolls growth misses expectations by a little and wage pressures diminish while more people enter the labor force, that would be an ideal scenario for the Fed, said Drew Matus, chief market strategist at MetLife Investment Management.

“The Goldilocks scenario is an unemployment rate rise with a participation rate rise,” Matus said. “What that’s suggesting is there’s a little bit of weakness that should translate into less wage pressure and take some of the concerns about sustained sticky high levels of inflation off the table.”

Investors on the lookout

Markets also will be watching the wage numbers closely.

Consensus estimates put average hourly earnings growth at 0.3% on the month, near the March move, and the yearly increase at 4%, or just below the 4.1% the month before. However, Matus said the wage numbers could be distorted by immigration patterns as well as California’s minimum wage increase this year to $16 an hour.

Fed Chair Jerome Powell said Wednesday that wage pressures have eased over the past year as the labor market has moved into better balance between supply and demand.

“Inflation has eased substantially over the past year, while the labor market has remained strong, and that’s very good news,” he said at his news conference after the central bank’s latest meeting. “But inflation is still too high.”

Markets have been in a state of flux as uncertainty over the Fed’s rate path has grown, though Wall Street was in rally mode Thursday, the day before the Bureau of Labor Statistics report drops at 8:30 a.m. ET.

“What you’re seeing in markets reflects the uncertainty around the path forward. What’s going to be more important to the Fed, unemployment or inflation?” Matus said. “If unemployment starts moving higher, is the Fed going to care as much about inflation as they do today? Or vice versa? And I don’t think even with all the information the Fed’s given us, that we know. I don’t think anyone knows and I think that’s why you’re seeing the market behave the way it is.”

Gen X can’t retire on time as inflation outpaces wages, survey finds

Are you ready for it? 4 steps to successfully integrate AI into your operations

What that means for consumer loans

Armanino adds Strategic Accounting Outsourced Solutions

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations