Finance

This week’s personal loan rates fall for 3-year terms, rise for 5-year terms

Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as “Credible” below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

The latest trends in interest rates for personal loans from the Credible marketplace, updated weekly. (iStock)

Borrowers with good credit seeking personal loans during the past seven days prequalified for rates that were lower for 3-year loans and higher for 5-year loans when compared to fixed-rate loans for the seven days before.

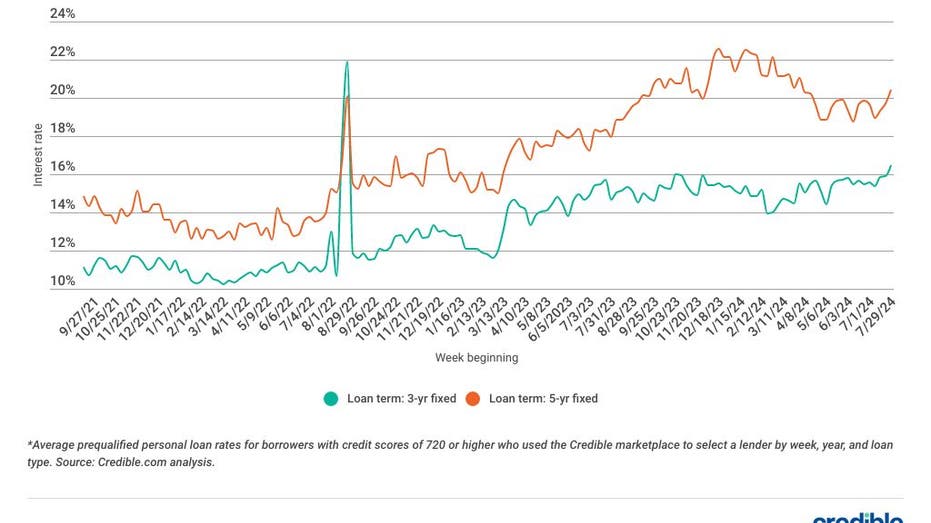

For borrowers with credit scores of 720 or higher who used the Credible marketplace to select a lender between August 1 and August 7:

- Rates on 3-year fixed-rate loans averaged 15.72%, down from 16.19% the seven days before and up from 15.03% a year ago.

- Rates on 5-year fixed-rate loans averaged 20.29%, up from 20.21% the previous seven days and from 18.42% a year ago.

Personal loans have become a popular way to consolidate debt and pay off credit card debt and other loans. They can also be used to cover unexpected and emergency expenses like medical bills, take care of a major purchase, or fund home improvement projects.

Average personal loan interest rates

Average personal loan interest rates have decreased over the last seven days for 3-year loans and increased for 5-year loans. While 3-year loan rates fell by 0.47 percentage points, rates on 5-year loans edged up by 0.08 percentage points. Interest rates for 3- and 5-year terms remain higher than they were this time last year, up 0.69 percentage points for 3-year terms and up 1.87 percentage points for 5-year terms.

Still, borrowers can take advantage of interest savings with a 3- or 5-year personal loan, as both loan terms offer lower interest rates on average than higher-cost borrowing options such as credit cards.

But whether a personal loan is right for you depends on multiple factors, including what rate you can qualify for, which is largely based on your credit score. Comparing multiple lenders and their rates helps ensure you get the best personal loan for your needs.

Before applying for a personal loan, use a personal loan marketplace like Credible to comparison shop.

Personal loan weekly rate trends

Here are the latest trends in personal loan interest rates from the Credible marketplace, updated weekly.

The chart above shows average prequalified rates for borrowers with credit scores of 720 or higher who used the Credible marketplace to select a lender.

For the month of July 2024:

- Rates on 3-year personal loans averaged 23.60%, up from 23.02% in June.

- Rates on 5-year personal loans averaged 25.06%, up from 24.81% in June.

Rates on personal loans vary considerably by credit score and loan term. If you’re curious about what kind of personal loan rates you may qualify for, you can use an online tool like Credible to compare options from different private lenders.

All Credible marketplace lenders offer fixed-rate loans at competitive rates. Because lenders use different methods to evaluate borrowers, it’s a good idea to request personal loan rates from multiple lenders so you can compare your options.

Current personal loan rates by credit score

In July, the average prequalified rate selected by borrowers was:

- 13.38% for borrowers with credit scores of 780 or above choosing a 3-year loan

- 32.38% for borrowers with credit scores below 600 choosing a 5-year loan

Depending on factors such as your credit score, which type of personal loan you’re seeking and the loan repayment term, the interest rate can differ.

As shown in the chart above, a good credit score can mean a lower interest rate, and rates tend to be higher on loans with fixed interest rates and longer repayment terms.

Where are interest rates headed?

The Bureau of Labor Statistics (BLS) reported that inflation slowed in May, raising hopes for multiple interest rate cuts in 2024. When the Fed concluded its June meeting, it signaled one cut by the end of the year while holding rates steady. As of now, we anticipate one 25 basis point (0.25 percentage points) cut this year, and a 100 basis point (1 percentage point) cut in 2025.

Currently sitting at 5.25% to 5.50%, the federal funds rate is the highest it’s been since 2001. Sticky inflation and low unemployment had made any cuts seem unlikely as of a week ago. But the news may deliver relief for borrowers burdened with high interest costs and those considering a loan. However, demand for personal loans has increased and all signs point to this trend continuing, while debt levels and delinquency rates have risen as well. This may indicate more consumers will struggle to be approved at low rates or at all — even if we see rates fall.

How to get a lower interest rate

Many factors influence the interest rate a lender might offer you on a personal loan. But you can take some steps to boost your chances of getting a lower interest rate. Here are some tactics to try.

Increase credit score

Generally, people with higher credit scores qualify for lower interest rates. Steps that can help you improve your credit score over time include:

- Pay bills on time: Payment history is the most important factor in your credit score. Pay all your bills on time for the amount due.

- Check your credit report: Look at your credit report to ensure there are no errors on it. If you find errors, dispute them with the credit bureau.

- Lower your credit utilization ratio: Paying down credit card debt can improve this important credit-scoring factor.

- Avoid opening new credit accounts: Only apply for and open credit accounts you actually need. Too many hard inquiries on your credit report in a short amount of time could lower your credit score.

Choose a shorter loan term

Personal loan repayment terms can vary from one to several years. Generally, shorter terms come with lower interest rates, since the lender’s money is at risk for a shorter period of time.

If your financial situation allows, applying for a shorter term could help you score a lower interest rate. Keep in mind the shorter term doesn’t just benefit the lender – by choosing a shorter repayment term, you’ll pay less interest over the life of the loan.

Get a cosigner

You may be familiar with the concept of a cosigner if you have student loans. If your credit isn’t good enough to qualify for the best personal loan interest rates, finding a cosigner with good credit could help you secure a lower interest rate.

Just remember, if you default on the loan, your cosigner will be on the hook to repay it. And cosigning for a loan could also affect their credit score.

Compare rates from different lenders

Before applying for a personal loan, it’s a good idea to shop around and compare offers from several different lenders to get the lowest rates. Online lenders typically offer the most competitive rates – and can be quicker to disburse your loan than a brick-and-mortar establishment.

But don’t worry, comparing rates and terms doesn’t have to be a time-consuming process.

Credible makes it easy. Just enter how much you want to borrow and you’ll be able to compare multiple lenders to choose the one that makes the most sense for you.

About Credible

Credible is a multi-lender marketplace that empowers consumers to discover financial products that are the best fit for their unique circumstances. Credible’s integrations with leading lenders and credit bureaus allow consumers to quickly compare accurate, personalized loan options – without putting their personal information at risk or affecting their credit score. The Credible marketplace provides an unrivaled customer experience, as reflected by over 7,500 positive Trustpilot reviews and a TrustScore of 4.8/5.

Alliance Global Partners chief global strategist Mark Grant discusses his income tax strategy for retirees on ‘Varney & Co.’

For the generation that should be in its “peak savings years,” the prospect of retiring on time has shifted from a plan to a prayer.

A newly released Employee Financial Wellness Survey by PwC found that nearly 50% of Gen X employees are pushing back their retirement dates, citing stagnant wages, rising everyday costs, and a lack of liquid savings.

Additionally, only 38% of Gen Xers believe they can retire when they originally planned, and more than half of this demographic expect to withdraw funds from their retirement accounts early to cover short-term costs.

“For employers, this isn’t a future problem. Financial anxiety during peak career years can affect focus and engagement,” PwC researchers write. “If the risks are clear, the question is why more employees aren’t taking action. It’s not a lack of desire. Most employees want stability, confidence and to feel in control. But many don’t feel equipped to get there.”

TEEN INVESTOR BOOM: WHY WALL STREET IS CHASING YOUNGEST GENERATIONS EARLIER THAN EVER

The primary driver of this retirement delay is the inability to save as inflation eats away at monthly expenses, the report notes. Twenty-five percent of the total workforce is living without a buffer, and nearly half cannot meet basic household expenses.

Nearly half of Gen X workers are delaying retirement, PwC reports. (Getty Images)

“[Forty-nine percent] say their compensation isn’t keeping up with costs. As expenses rise faster than income, day-to-day trade-offs are becoming routine. Employees aren’t just feeling squeezed. They’re making difficult financial decisions to stay afloat,” the PwC report continues..

As a result, when Gen Xers cannot afford to leave their current jobs, the entire corporate ladder stalls, creating business risks, with companies facing higher costs as older talent remains on payroll longer than expected.

BlackRock Global Head of Retirement Solutions Nick Nefouse joins ‘Varney & Co.’ to discuss a proposed rule expanding 401(k)s to crypto and real estate.

“When employees dip into retirement funds early or delay retirement altogether, it affects more than personal finances and retirement plan leakage,” the report says. “It may also influence workforce planning, healthcare costs, succession timing and overall organizational stability.”

The findings also show that a significant portion – 41% – of the workforce feel they were never given the tools to manage a crisis of this magnitude, leading to a sense of being “overwhelmed” by financial choices.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

‘The Big Money Show’ breaks down new IRS limits for 401(k)s and IRAs, giving savers more room to invest for retirement.

PwC provided a call to action for employees and their employers, encouraging them to reduce the stigma around financial education, foster trust through human coaches, emphasize skill building and focus on day-to-day finances before long-term goals.

“Employees define financial wellness simply: less stress, fewer surprises and the freedom to make financial choices with confidence. For employers, that’s the opportunity.”

Cybersecurity and enterprise software stocks have been market dogs in 2026, with fears that AI will wipe out a wide range of companies in the enterprise space dominating the narrative. But they snapped a brutal losing streak this past week, joining in the broader market rally that saw all losses from the U.S.-Iran war regained by the Dow Jones Industrial Average and S&P 500.

Cybersecurity has been “a victim of some of the AI-related headlines,” Christian Magoon, Amplify ETFs CEO, said on this week’s “ETF Edge.”

It wasn’t just niche cybersecurity names. Take Microsoft, for example, which was recently down close to 20% for the year. Its shares surged last week by 13%.

A big driver of the pummeling in software stocks was a rotation within tech by investors to AI infrastructure and semiconductors and some other names in large-cap tech, Magoon said, and since cybersecurity stocks and ETFs are heavily weighted towards software companies, they were left behind even as those businesses continue to grow on a fundamental basis.

But Wall Street now has become more bullish with the stocks at lower levels. Brent Thill, Jefferies tech analyst, said last week that the worst may be over for software stocks. “I think that this concept that software is dead, and then Anthropic and OpenAI are going to kill the entire industry, is just over-exaggerated,” he said on CNBC’s “Money Movers” on Wednesday.

“Big Short” investor Michael Burry wrote in a Substack post on Wednesday that he is becoming bullish about software stocks after the recent selloff. “Software stocks remain interesting because of accelerated extreme declines last week arising from a reflexive positive feedback loop between falling software stocks and changes in the market for their bank debt,” he wrote.

The Global X Cybersecurity ETF (BUG), is down about 12% since the beginning of the year, with top holdings including Palo Alto Networks, Fortinet, Akamai Technologies and CrowdStrike. But BUG was up 12% last week. The First Trust NASDAQ Cybersecurity ETF (CIBR) is down 6% for the year, but up 9% in the past week.

Piper Sandler analyst Rob Owens reiterated an “overweight” rating on Palo Alto Networks which helped the stock pop 7% — it is now down roughly 6% on the year. Its peers saw similar moves, including CrowdStrike.

Performance of Global X cybersecurity ETF versus S&P 500 over past one-year period.

Magoon said expectations may have become too high in cybersecurity, and with a crowding effect among investors, solid results were not enough to to push stocks higher. But the down-and-then-back-up 2026 for the sector is also a reminder that when stocks fall sharply in a short period of time, opportunity may knock.

“Once you’re down over 10% in some of these subsectors, you start to see the contrarians start to say, ‘well, maybe I’ll take a look at this,'” Magoon said.

He said AI does add both opportunity and uncertainty to the cybersecurity equation, increasing demand but also introducing new competition. But he added, “I think the dip is good to buy in an AI-driven world,” specifically because the risks to companies may lead to more M&A in cyber names that benefits the stocks.

For now, investors may look for opportunity on the margins rather than rush back into beaten-up tech names. “I think investors are still going to remain underweight software,” Thill said.

But Magoon advises investors to at least take the reminder to keep an eye on niches in the market during pronounced downturns. “The best-performing are often the least bought and do the best over the next 12 months versus late-in-the-game piling on,” he said.

While that may have been a mindset that worked against the last investors into cybersecurity and enterprise software in mid-2025 when the negative sentiment started building, at least for now, it’s started working for the stocks in the sector again.

Meanwhile, this year’s biggest winner is also a good example of what can be an extended trade in either a bullish or bearish direction. Last year, institutional ownership of energy was at multi-year lows, Magoon said, referencing Bank of America data. “Reverse sentiment can be a great indicator,” he said.

But he cautioned that any selective buying of stocks that have dipped does have to contend with the risk that there is a potentially bigger drawdown in the market yet to come in 2026. That is because midterm election years historically have been marked by large drawdowns. “If you think it is bad right now, it could get a lot worse,” Magoon said. But he added that there’s a silver-lining in that data, too, for the patient investor. The market has posted very strong 12-month returns after midterm election drawdowns end. So, for investors with a longer-term time horizon and no need for short-term liquidity, Magoon said, “stick in there.”

Sign up for our weekly newsletter that goes beyond the livestream, offering a closer look at the trends and figures shaping the ETF market.

New innovation in the exchange-traded fund industry could come at a cost to investors during extreme conditions.

According to MFS Investment Management’s Jamie Harrison, ETFs involved in increasingly complex derivatives and less transparent markets may be in uncharted territory when it comes to violent downturns.

“Those would be something that you’d want to keep an eye on as volatility ramps up,” the firm’s head of ETF capital markets told CNBC’s “ETF Edge” this week. “As innovation continues to increase at a rapid pace within the ETF wrapper, [it’s] definitely something that we advise our clients to be really front-footed about… Lack of transparency could absolutely be an issue if we’re going to start seeing some deep sell-offs.”

His firm has been around since 1924 and is known for inventing the open-end mutual fund. Last year, ETF.com named MFS Investment Management as the best new ETF issuer.

“It’s important to do due diligence on the portfolio,” he said. “Having a firm that has deep partnerships, deep bench of subject matter experts that plays with the A-team in terms of the Street and liquidity providers available [are] super important.”

Liquidity as the real issue?

Harrison suggested the real issue is liquidity, particularly during a steep sell-off.

“We’ve all seen the news and the headlines around potential private credit ETFs. That picture becomes much more murky,” he added. “It’s up to advisors, to investors [and] to clients to really dig in and look under the hood and engage with their issuers.”

He noted investors will have to ask some tough questions.

“What does this look like in a 20% drawdown? How does this liquidity facility work? Am I going to be able to get in? Am I going to be able to get out? And if I’m able to get out, am I able to get out at a price that’s tight to NAV [net asset value], and what’s the infrastructure at your shop in terms of managing that consideration for me,” said Harrison.

Amplify ETFs’ Christian Magoon is also concerned about these newer ETF strategies could weather a monster drawdown. He listed private credit as a red flag.

“If your ETF owns private credit, I think it’s worth taking a look at, kind of what the standards are around liquidity and how that ETF is trading, because that should be a bit of a mismatch between the trading pace of ETFs and the underlying asset,” the firm’s CEO said in the same interview.

Magoon also highlighted potential issues surrounding equity-linked notes. The notes provide fixed income security while offering potentially higher returns linked to stocks or equity indexes.

“Those could potentially be in stress due to redemptions and the underlying credit risk. That’s another kind of unique derivative,” Magoon said. “I would very closely look at any ETF that has equity-linked notes should we get into a major drawdown or there be a contagion in private credit or something related to the banking system.”

Gen X can’t retire on time as inflation outpaces wages, survey finds

Are you ready for it? 4 steps to successfully integrate AI into your operations

What that means for consumer loans

Armanino adds Strategic Accounting Outsourced Solutions

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations