Accounting

Art of Accounting: Building wealth outside your practice

Enjoy complimentary access to top ideas and insights — selected by our editors.

In a

If you are an owner or partner in an accounting practice the chances are you’ve established a 401(k) or similar plan and are making the maximum payments into it, whether pretax or post tax as your circumstances permitted. The tax-sheltered buildup of assets is very important and provides a firm base for your retirement cash flow. You just have to not screw it up with the wrong type of investments or inattention. These retirement accounts will be a core foundation of your wealth and you should not skip payments into these accounts.

When I refer to wealth, I am referring to the base you will establish from which your retirement cash flow, and the security it will provide you with, will come from. It is possible to have substantial net worth, but minimal cash flow. An example is a significant residence and two vacation homes, a boat and a great art collection. By all measures you would be counted among the rich, but none of these would provide cash flow. My concern is how you will pay for your living costs when you stop working. You will do that out of cash flow and not from illiquid assets. Concentrate on building your investment portfolio.

If you are a solo owner or a partner in a practice you likely will be anticipating receiving funds from either the sale of your practice or the buy-out from your remaining partners to provide a further base from which you would receive cash flow from. I suggest that this not be depended on. You can anticipate it and do whatever you can to maximize the future amount, but do not depend on this. Things, circumstances and conditions change as does the economy, the availability of buyers, the retention of clients, the sustainability of fees, lingering health issues of you or a loved one, personal liability litigation and interest rates. Get what you can when the time comes, but do not depend on it.

Other sources of wealth

Your children? It is possible, but I suggest you fuhgeddaboudit.

Sale of your residence. Not likely since you would need to live somewhere else. Further, if you do not use those proceeds to buy another house, you would need to use the income, and perhaps some of the principal, to pay your rent. This doesn’t work.

Social Security. This is a definite to count on. I also suggest you wait until you are age 70 to start your benefits. This will add 24% to your annual benefits and it will be guaranteed to last your entire lifetime. Do not succumb to the fallacious logic that if you died before a certain number of years, you would lose out and should have taken it as soon as you were able to get your full benefits without waiting for the added 24%. If you die beforehand, you will lose nothing since you will be dead! However, if you do not die prematurely, you will receive a 24% greater annual payment that you cannot outlive. The second spurious argument is that you could get the benefits and invest it better. That ain’t so for two reasons. 1) Your benefits would be reduced by income taxes on 85% of the funds thereby reducing your “investable” amounts. 2) It is extremely unlikely you could reasonably invest the after-tax cash flow where you could do better than a 24% added benefit each year.

Investments. This works and would be in addition to your retirement accounts. A suggestion is to start adding funds on a regular basis as you are doing with your retirement accounts. And be smart about your investment decisions. To accomplish this, you might need to earn additional amounts from your practice. Make this a goal and price your services accordingly. Reread my previous article with the link above.

Annuities. These are another form of investing and should be integrated with your investment plan.

Mortgage. Your wealth increase will be hampered by interest payments on any mortgages. Develop a plan to reduce your mortgage as quickly as possible. Just adding a small amount to each payment would work wonders. Unless you have an older mortgage with a very low interest rate, chances are you would not be able to earn more on safe investments than your mortgage interest rate.

Credit cards. Reducing this debt is a no-brainer and should be attacked as quickly as possible. While the mortgage paydown might need some number crunching, credit card debt elimination is a must do.

Kid’s college payments. This is not a wealth-building method but a wealth retardant. If you are facing college costs for your children, make that a priority and do not be overly concerned about anything else, other than fully funding your tax-sheltered retirement accounts. Here is a plan I recommend to clients. Make your children’s college costs a major priority. This will usually have to be paid while you are still making mortgage payments. Do both and do not worry about added funds for your retirement. When your children are finished with college it should also coincide with your mortgage balance being greatly reduced. At that point deposit the amounts you were paying for college and the mortgage into your investment account. 10 to 15 years of continuing this would add up to a pretty decent investment account. My rule (copied from Stephen Covey) is to make the main things the main thing. Do not get overly anxious about not having a built-up investment account. Take care of your kids first.

These are some suggestions to build your wealth and establish a secure cash flow in retirement. Consider what you want, but in any event, the sooner you get started the better off you will end up.

Comment: My Memoirs as a CPA book has been published and is available in Kindle and print editions at amazon.com. Buy it, read it and enjoy it! Do not hesitate to contact me at

An IRS proposal to drop a Biden administration rule targeting basis-shifting strategies by complex partnerships is getting support from key stakeholders, as well as calls for further relief.

But critics argue that dropping the regulation would let wealthy tax cheats off the hook. Even those who advocate getting rid of the rule say the IRS must take more action to remove enforcement risks around partnership basis-shifting strategies.

The

These transactions enable businesses to transfer tax basis out of assets where it was not generating savings to affiliated entities where it could gain benefits, such as moving it from stock or land holdings to the partnership’s equipment infrastructure and its depreciation capabilities. In its final days, the Biden administration

The fact that the Trump administration’s proposal wouldn’t also cancel the revenue ruling memo caught the attention of some antitax advocacy groups and industry professionals.

“Given that Revenue Ruling 2024-14 was not withdrawn, continued diligence is required in identifying any transactions that may fall within the scope of the revenue ruling or otherwise be subject to potential challenges under the economic substance doctrine, or other common law principles such as the substance-over-form doctrine or step transaction doctrine,”

READ MORE:

The business backdrop

Regardless of their view of the proposal, President Trump, DOGE or tax-dodging efforts by wealthy households in general, advisors can provide value to clients by keeping abreast of IRS regulations, according to Jason Smith, CEO of Westlake, Ohio-based advisory practice

Smith’s firm evolved from referring tax services to outside certified public accountants to hiring them and enrolled agents as a means of providing what he called the “trilogy” of tax planning, management and preparation.

“You could sit there and tout investment performance, but it’s not about what you make, it’s about what you keep,” Smith said. “I just don’t know how you can really say that you’re doing true wealth management without connecting those two, the investments and the taxes.”

READ MORE:

Reactions to repeal

For some business owners, the complex basis-shifting maneuvers among affiliated entities in a partnership provide substantial savings — although the last administration’s Treasury Department argued that verifying the economic substance of the transactions would save taxpayers

“This is a ridiculous loophole that allows the ultra-rich to dodge taxes by shifting assets around on paper while adding zero value to our economy whatsoever,” Wyden said in

However, groups supporting the withdrawal of the rule include

“The previous administration’s near-obsessive focus on partnerships was driven by the belief that vast revenue collection potential exists in some sectors of our economy if only the IRS were handed sufficiently intimidating enforcement tools,” National Taxpayers Union President Pete Sepp wrote. “Unfortunately, history has shown that there are no gold mines leading to such easy riches for the government. Instead, the pursuit of the ‘shiny object’ leaves many innocent taxpayers harmed along the way, while distracting the Service’s attention from top-notch customer service and clear, consistent, guidance that provide the basis of respect for the law.”

READ MORE:

Stay tuned, advisors and tax pros

An upcoming IRS notice of proposed rulemaking could address the full scope of the agency’s withdrawal of the prior regulation and its current stance on the economic substance of basis-shifting transactions by partnerships.

The Biden administration’s regulation would have exerted greater enforcement oversight in “tax-free transfers, distributions and liquidations of partnership interests to partners and other related parties or transferees, in which a basis increase provides related parties with an opportunity to decrease their taxable income through increased cost recovery deductions, including as property depreciation deductions, and decreased taxable gains (or increased taxable losses),” according to a blog

“This essentially provides taxpayers and their material advisors with immediate relief from retroactive reporting requirements and any related penalties for noncompliance,” Kenelby wrote. “The IRS is expected to issue a notice of proposed rulemaking in the coming months to finalize the details of repealing the basis-shifting regulations.”

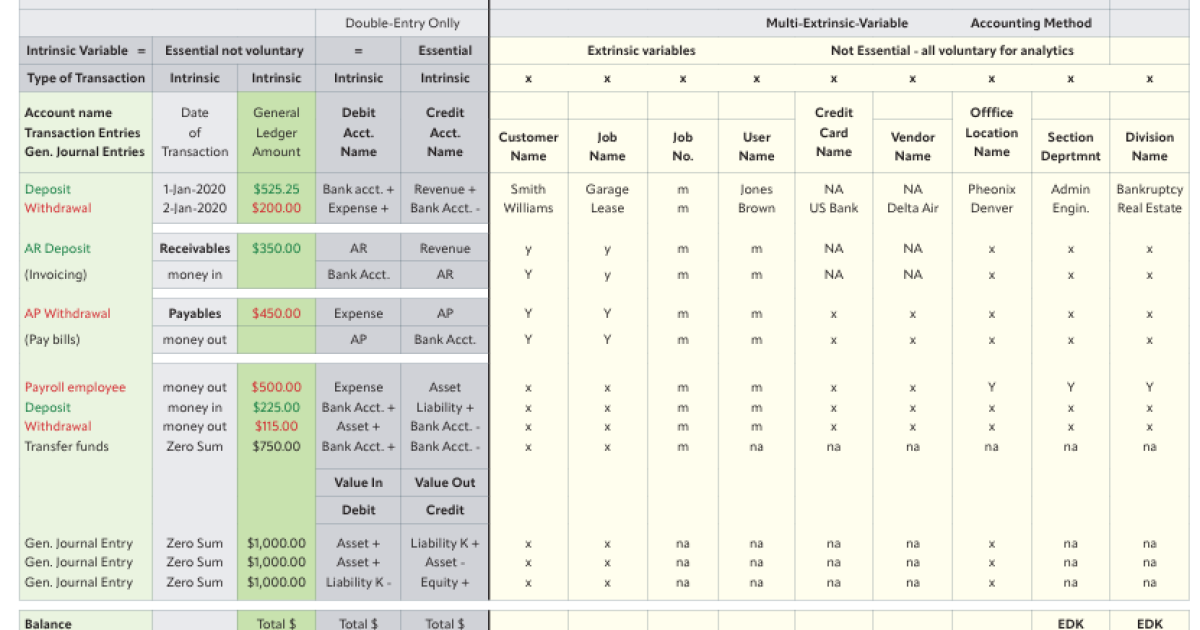

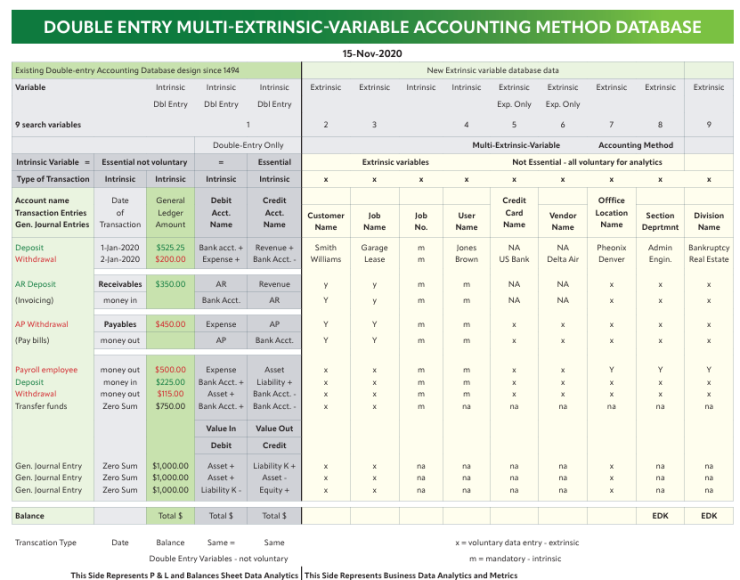

Edward Kellman, CEO and chief design engineer of Trakker Apps, holds two U.S. patents for an innovative take on double-entry accounting

The system, known as the Double-Entry Multi-Extrinsic-Variable Accounting Method Database, aims to modernize financial tracking while preserving the essence of the traditional accounting system that was first described by Luca Pacioli back in 1494. It leverages artificial intelligence while generating and reconciling multiple financial ledgers by account, user, customer, job and vendor.

“I made a representation of the current double entry database, which basically collects a date, amount, a debit and a credit account, and that’s about as much of that calculation as you can do by hand,” said Kellman. “It’s been done by hand for hundreds of years. It’s very tedious, but nobody ever thought to expand the database now that you can use a computer to solve for these enormously complex database solutions.”

He expanded the database with new variables, which he calls extrinsic variables, and now it can track financial transactions by customer, job, user and vendor. “By doing that, I’ve created an enormous amount of new financial solutions that can be plucked from the database that never existed, and these are all financial analytics for your company, because the variables are the things that matter in your company: which jobs make the most money, which users produce the most income and expenses, and things of this nature,” said Kellman. “But because I expanded that database, and nobody thought to do this since 1494 when this system was first published. It’s totally modernized double entry accounting.”

He offers them as apps that can be downloaded from the Apple and Android app stores, along with a browser-based version through the

The system leverages artificial intelligence to automate data entry. “I didn’t want it to become a tedious process for entering data, so we basically wrote these AI data entry algorithms that collect the data and fill in the data when it knows it right away,” said Kellman. “You can enter these transactions really just as quickly, if not quicker, on a smartphone than you can on any other accounting system, because of the data entry algorithms that just collect the data really quickly. And once you hit Enter and record that transaction, that’s all stored in the cloud. All your business is digitized.”

He did beta testing for a year on the app stores, where the program had around 6,000 downloads. But then he shut down the program because he didn’t want to be the cloud host responsible for storing thousands of people’s financial data so he is searching for a banking partner to host it securely. The system provides a kind of ERP platform that combines banking and accounting.

“Instead of printing profit and loss reports and balance sheet reports and trial balance summary reports just for the whole company, I can print them individually, for each individual user or each individual job,” said Kellman. “Or if you have multiple users, like in a law firm on one job, you can select the job and the user and print just the transactions that apply to those variables that you’ve selected, and now you’ve got a wealth of information about your company that never existed before.”

Trakker Apps’ BaaS fintech platform includes Business Trakker, Invoice 4 Business, Expense Trakker, Balance Sheet Trakker and Escrow Trakker for Lawyers.

It took four years before Kellman was able to patent the technology. “Normally, when you apply for a patent, they spend a lot of time on a patent search, where they investigate all the previous patents to see if you’re in violation of any other patents, or any other art that exists,” he said. “My patents are the only patents ever issued for a double entry accounting system, and there was no prior art. It took about four years to get it, and then I got a second one after that.”

Kellman isn’t planning to challenge other accounting software companies now that he has the

The Committee of Sponsoring Organizations of the Treadway Commission and the National Association of Corporate Directors have released an

Last May,

The Corporate Governance Framework is designed to complement and align with COSO’s longstanding Internal Control and Enterprise Risk Management frameworks. It includes practices to help organizations improve their governance effectiveness, manage risks proactively and create long-term value. COSO is jointly sponsored by the American Accounting Association, the American Institute of CPAs, Financial Executives International, the Institute of Management Accountants and the Institute of Internal Auditors.

“Resilient and well-structured corporate governance is the foundation of trust in capital markets, ethical business practices, and sustainable financial performance,” said COSO executive director and chair Lucia Wind in a statement Tuesday. “This framework provides organizations with a structured yet flexible approach to governance, ensuring they can navigate today’s complex regulatory and risk landscape with confidence, enable organizational effectiveness, while building long term value for its shareholders.”

Public comments will be accepted until July 11, 2025. The

COSO and the NACD are encouraging a holistic approach to defining corporate governance, extending beyond the boardroom to encompass the practices, information channels, and processes that govern how an entity is being directed, managed and controlled.

“Strong corporate governance creates a competitive advantage for organizations of all sizes, stages of maturity, and growth strategies,” said NACD president and CEO Peter Gleason in a statement. “This framework will help boards and management align on the importance and scope of governance in a time of tremendous complexity and disruption. When adapted to fit an organization’s specific needs, the framework will help drive better business outcomes and higher-quality board and management performance.”

COSO and the NACD see corporate governance as involving the oversight and processes by which an informed board and management team steers an entity toward executing its strategies and goals while maximizing long-term shareholder value in an ethical manner and within the relevant legal and regulatory environment.

“By providing a common language and practical guidance, it empowers boards, management, and employees to work together in building resilient, accountable organizations that can adapt, compete, and deliver long-term value to shareholders and other key stakeholders,” said Lillian Borsa and Brian Schwartz, PwC US principals and co-leads of the COSO Corporate Governance Framework, in a joint statement.

-

Accounting7 days ago

Accounting7 days agoHouse tax bill includes provision eliminating PCAOB

-

Economics1 week ago

Economics1 week agoWhat happens if the Inflation Reduction Act goes away?

-

Personal Finance7 days ago

Personal Finance7 days agoWhat House Republican ‘big beautiful’ budget bill means for your money

-

Accounting7 days ago

Accounting7 days agoTrump tax bill faces Senate’s arcane rules, desire for changes

-

Finance6 days ago

Finance6 days agoPersonal finance app Monarch raises $75 million

-

Economics1 week ago

Economics1 week agoJoe Biden did not decline alone

-

Economics7 days ago

Economics7 days agoHow much worse could America’s measles outbreak get?

-

Economics7 days ago

Economics7 days agoA court resurrects the United States Institute of Peace