Accounting

Bessent says Musk’s DOGE isn’t altering Treasury systems

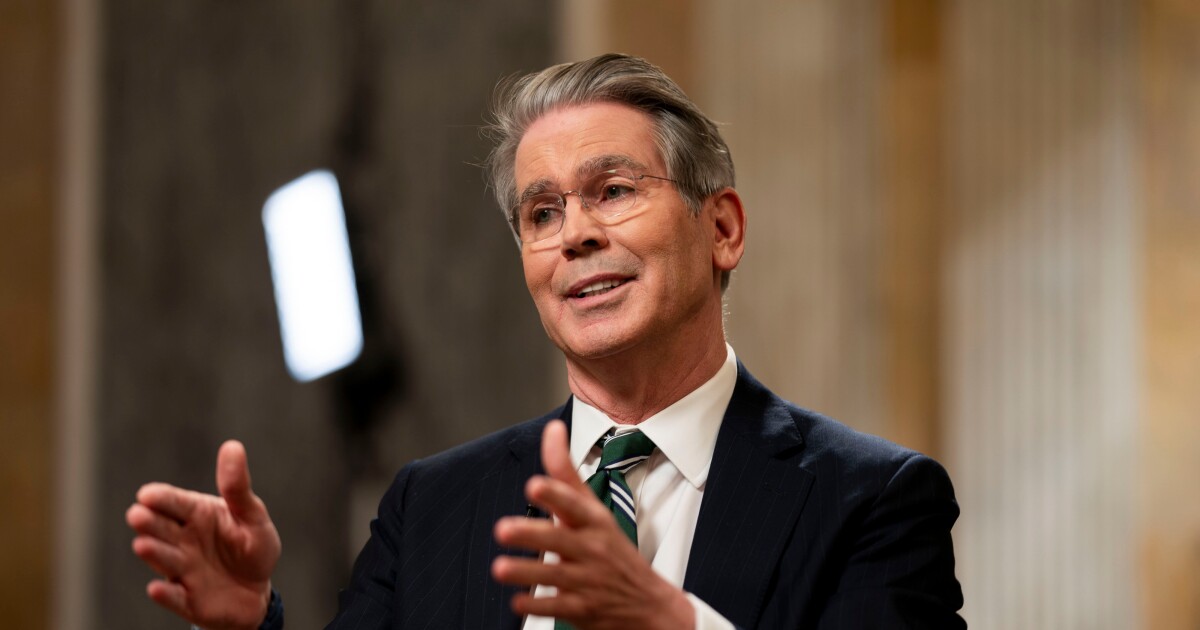

Treasury Secretary Scott Bessent said he personally vetted the Treasury employees on Elon Musk’s government efficiency team who have read-only access to federal payment data, and that there’s been no “tinkering” with the department’s payment systems.

“It is an operational review. It is not an ideological review,” Bessent said in an interview on Bloomberg Television with Saleha Mohsin on Thursday. “The ability to change the system sits over at the Federal Reserve. We don’t even run the system.”

Bessent voiced confidence for Musk’s team. “These are highly trained professionals. This is not some roving band running around doing things. This is methodical and it is going to yield big savings,” he said. not supported.

Bessent’s department has been an early focus of the Department of Government Efficiency, the Musk-led effort to identify wasteful spending and modernize federal technology.

Since President Donald Trump’s inauguration, DOGE has been instrumental in offering a buyout to civilian federal retirees, canceling government leases and contracts, and even dismantling the U.S. Agency for International Development.

But Bessent said the Internal Revenue Service would be largely spared from DOGE’s cost-cutting — at least until after the April 15 filing deadline, with customer-facing employees excluded from the government-wide deferred resignation program until mid-May.

Still, trillions of dollars of federal payments flow through Treasury every year, and DOGE’s access gives Musk visibility into sensitive-but-unclassified information about taxpayers, beneficiaries, contractors and employees.

Members of Congress, federal employee unions and privacy advocates have protested that access, citing the billionaire’s sprawling business interests. Musk, the world’s richest man, is CEO of SpaceX, which has billions in federal contracts to launch rockets, and of Tesla Inc., which is regulated by multiple departments and agencies.

In posts on X, his social media site, Musk has also claimed the ability to stop federal payments, but Bessent said that DOGE’s read-only access doesn’t give him that power.

“Most of that happens above us” at federal departments and agencies that manage their own budgets, Bessent said.

The Treasury Department — under both Democratic and Republican administrations — has long maintained it doesn’t have the power to stop or prioritize payments authorized by agencies.

Still, Bessent expressed enthusiasm for Musk’s efforts.

“I think there are gigantic cost savings for the American people here,” he said. “I believe that this DOGE program, in my adult life, is one of the most important audits of government, or changes to government structure, that we have seen.”

The Securities and Exchange Commission is already making plans in the event that the massive tax bill now moving through Congress ends up shifting the Public Company Accounting Oversight Board’s duties to the SEC.

In late May, the House

“I guess as an initial matter, certainly, we are aware of the proposed legislation that is both in the House and the Senate as part of the budget reconciliation bill,” said SEC acting chief accountant Ryan Wolfe during Financial Executives International’s SEC and Financial Reporting Conference at the University of Southern California’s Leventhal School of Accounting. “I think from the staff perspective, where we’re assisting the Commission, it’s important that we are thinking about these issues, are monitoring and are prepared as the potential for these bills to move forward would result in the Commission having new statutory responsibilities. Specifically with respect to standard-setting and inspections, the enforcement authorities would also transfer, but we already have shared jurisdiction with respect to those activities.”

He noted that the SEC has been hearing a great deal of feedback about it across the spectrum.

“I would observe that one thing that I hear, I don’t want to say universally, but quite consistently, is the importance or the overall ecosystem of the three major programs that the PCAOB engages in, being standard-setting for auditors, inspections of auditors to evaluate the compliance with those standards, and similarly, the enforcement function,” said Wolfe. “And so I think that these are incredibly important objectives that will continue regardless, which is just to say, without providing any significant details, that we’re aware of it and we are working on those issues.”

On the other hand, the SEC’s Office of Chief Accountant is prepared in case the provision gets dropped from the final bill.

“But in the event that that would not go forward, the OCA’s assistance with the Commission and the oversight of the PCAOB will continue regardless,” said Wolfe.

He also pointed to the importance of continuing standards such as the

Panel moderator Mark Kronforst, a partner at Ernst & Young, pointed out that SEC chair Paul Atkins said during a recent congressional hearing that despite a recent 15% reduction in staff at the SEC, there would still be room in the budget for the PCAOB under the legislation.

Another SEC official also acknowledged the recent reduction in the staff during a later panel discussion.

“Certainly, there has been a reduction in the federal workforce and the Commission, the SEC, has been no exception to that,” said Gaurav Hiranandani, acting deputy chief accountants at the SEC. “Many of the talented staff at the Commission have decided to retire or have sought opportunities outside of the commission. Within OCA, we have also seen some talent depart, some longstanding staff.” He noted that some of the speakers at last year’s conference are among those who left.

Financial Accounting Standards Board chair Richard Jones also spoke at the conference and discussed the progress that FASB has been making on its standard-setting.

“A couple years ago, we comprehensively reset our agenda,” he said. “We did robust stakeholder output to really ask an open-ended question of what should be the FASB’s priority, and what you’ve seen over the last couple of years is us executing on that revised agenda. If you pull up our technical agenda today, you’ll see there are 12 projects on our technical agenda. Of those 12 projects, five of those have been voted out by our board to proceed to final standards. Five of those are in redeliberations, meaning that we’ve already issued an exposure draft, we’ve gotten great input from our stakeholders, and our board will be redeliberating to decide what direction to go forward on those standards. We voted to move forward with an exposure draft on another standard, so that’s 11 of the 12. If you follow those through, and you follow a plan of execution on those standards, it’s very reasonable that we could complete substantially all the projects on our agenda at or about the end of this year.”

U.S. accountants who advise small and midsized businesses are feeling less confident this year, according to a new survey.

The

Between January and April, the net sentiment among accountants swung from a positive 19% to a negative 39%. Initially, nearly half (47%) of advisors foresaw improving conditions. But by April, only 25% held this view, with nearly two-thirds (64%) expecting worsening economic environments. The shift signifies growing apprehension across Main Street accounting firms serving as advisors on tax, payroll and compliance decisions amid a backdrop of historic tariff actions, continued inflation and unpredictable tax and trade policies.

Accounting advisors pointed to the top issues impacting their clients, with 61% citing inflation, costs and pricing; 60% naming tariffs and trade impacts and uncertainty; 59% pinpointing unease around new tax legislation; 42% identifying ongoing labor supply and wage issues; and 37% citing technology and AI adoption as a priority.

“Accountants are sounding an urgent alarm,” said CPA Trendlines founder Rick Telberg in a statement Wednesday. “They’re advising SMBs to conserve cash, curb discretionary expenses, and resist taking on unnecessary debt. Amid volatility in tariffs, inflation, and complex tax legislation, SMBs face serious barriers to strategic growth and operational stability.”

According to the accountants polled, the biggest challenges facing SMBs are hiring and retaining talent (60%), keeping pace with technology (55%), and managing rising costs (52%). The added strain of tariffs has handicapped SMBs’ adaptability and agility, which is typically their key advantage over larger competitors.

Other challenges include adapting to disruption (35%), meeting evolving customer expectations (32%), and managing product costs (29%).

Accountants feel the most confidence in their professional services sector — including doctors, lawyers and other professionals — with 60% believing this sector will thrive during a downturn. Not far behind that is the technology sector, where 57% of accountants expressed confidence driven by strong demand for digital solutions and AI that boost operational efficiency and resilience. And the oil, energy and mining sectors show 39% of respondents optimistic due to recent spikes in supply and demand for these resources.

On the other hand, farming (6%), franchising (3%), and arts and entertainment (2%) are seen as the most vulnerable sectors. These sectors depend heavily on broader economic performance, and the recent tariffs have further strained their growth and output.

Firms are encouraging clients to monitor their burn rates, cut overhead and avoid unnecessary borrowing. AI and automation are also important as survival tools amid labor shortages and pricing pressure.

“This year’s survey underscores a critical moment for the SMB business sector,” said Sona Akmakjian, head of global strategic accountant partnerships at Avalara, in a statement. “Accountants are urging businesses to fortify themselves against ongoing economic turbulence by sharpening their operational focus, adopting intelligent technology, and carefully managing resources. Clients are, more than ever, relying on the accretive business acumen and advisory skills of their trusted advisor for guidance through historic headwinds and uncertainty.”

The 2025 Accountants Confidence Report

Republican senators are considering placing a $30,000 cap on the state and local tax deduction as a compromise between current law and the more generous limit in the House’s version of President Donald Trump’s tax bill, a key GOP negotiator said.

Senator Thom Tillis, a moderate Republican involved in the talks, said Republican senators are trying to reduce the House-passed $40,000 SALT limit to at least $30,000.

Republican senators are meeting behind closed doors Wednesday afternoon to discuss the details of the bill, which the Senate is aiming to pass later this month.

SALT was a core issue in the House, where Republicans from high-tax states like New York, New Jersey and California threatened to block the bill without a substantial increase to the current $10,000 SALT cap.

House Speaker Mike Johnson has warned senators to make as few changes as possible to the House’s SALT deal. But SALT isn’t a concern in the Senate, where there are no Republicans representing states where the deduction is a political priority.

“It’s hard because we don’t have any senators from SALT states,” said Republican Senator Markwayne Mullin. “We are searching for a compromise.”

Mullin said he has already spoken on the issue with New York Republican Mike Lawler, a key proponent of the increased SALT cap.

GameStop shares tank on convertible bond offering to potentially buy more bitcoin

UK exports to the U.S. plunge by most on record as tariffs bite

The meaning of the protests in Los Angeles

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Personal Finance1 week ago

Personal Finance1 week agoWhat the national debt, deficit mean for your money

-

Economics1 week ago

Economics1 week agoPeople cooking at home at highest level since Covid, Campbell’s says

-

Economics6 days ago

Economics6 days agoJobs report May 2025:

-

Economics1 week ago

Economics1 week agoElon Musk’s failure in government

-

Economics6 days ago

Economics6 days agoDonald Trump has many ways to hurt Elon Musk

-

Finance6 days ago

Finance6 days agoStocks making the biggest moves midday: WOOF, TSLA, CRCL, LULU

-

Economics6 days ago

Donald Trump has many ways to hurt Elon Musk

-

Economics4 days ago

Economics4 days agoSending the National Guard to LA is not about stopping rioting