Accounting

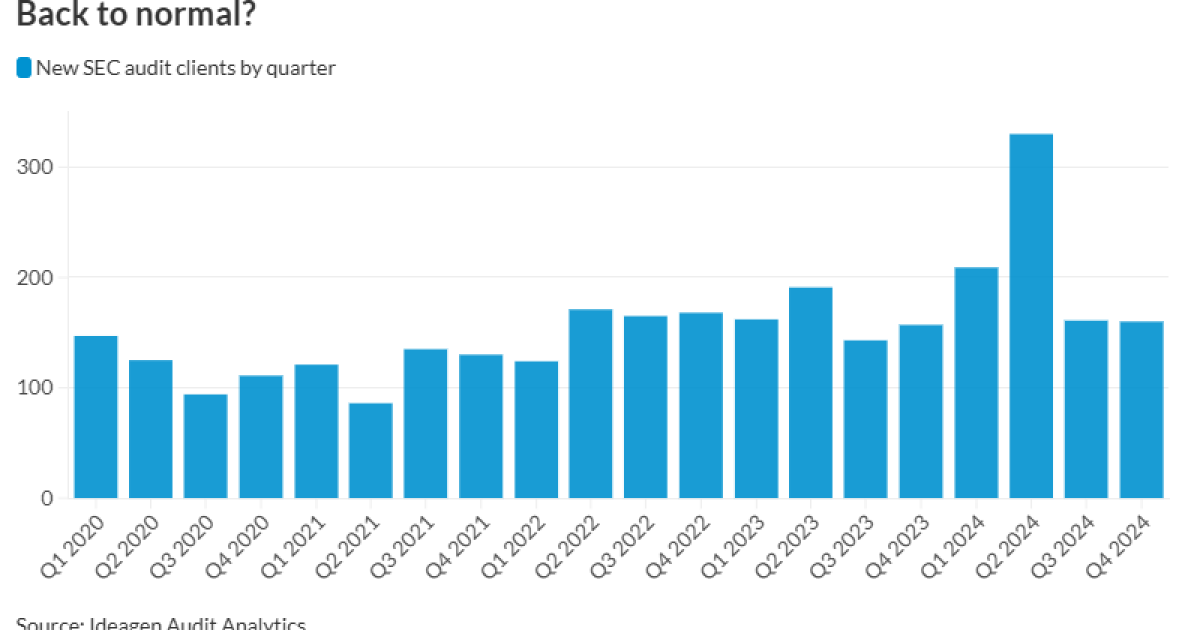

Bush & Associates, KMPG take top spots for new SEC audit clients in 2024

A small firm in Henderson, Nevada, Bush & Associates, topped the list of those with the most new Securities and Exchange Commission audit clients in 2024, followed by Big Four firm KPMG — but the audit firm that had what was likely the biggest impact on the market isn’t on the list at all.

Bush & Associates added 32 new SEC clients and netted 30 over the course of last year, while KPMG added 39 and netted 23. (See “

Almost half of Bush’s new clients — 14 out of 32 — came from one-time star BF Borgers, which was permanently suspended from practice by the commission in May, and whose

A significant number of firms picked up clients that had been with Borgers, including:

- Michael Gillespie & Associates, with 15 Borgers clients;

- Boladale Lawal & Co., with 12;

- Fruci & Associates, with 10;

- Olayinka Oyebola & Co., with 9;

- Astra Audit, BCRG Group, and M&K CPAs, with six each; and,

- BartonCPA and Beckles & Co., with five each.

BF Borgers wasn’t the only firm whose clients were looking for new homes: Astra Audit picked up 13 new engagements in 2024 from Accell Audit & Compliance, which closed down its SEC practice, and the exit of Morison Cogen from the SEC market helped Stephano Slack pick up 11.

Most of these firm departures didn’t have much of an impact on the largest auditors (see “

Clients by filing status, and more

In terms of clients by filing status, KPMG led among new large accelerated filers, while Bush & Associates took the lead among non-accelerated filers and small reporting companies. (See “

As you might expect, KPMG topped the league tables for new market capitalization audited, with the biggest contribution coming from Grayscale Bitcoin Trust’s $25.5 billion, as well as for new assets audited, with insurance underwriter Everest Group accounting for $49.3 billion and Grayscale Bitcoin Trust for $26.4 billion. It came in second for new audit fees, energy distribution and services company UGI Corp. the biggest slice, at $9 million, and all the rest of its clients scattered below that. (See “

Deloitte was No. 1 for new audit fees, with dental instrument and supply provider Dentsply Sirona Inc. coming in at $11.8 million and 3D printing company 3D Systems Corp. at $10 million, and all its other clients below that. The firm came in second for new assets audited, with insurance holding company American National Group’s $79.9 billion and cruise line Carnival’s $49 billion standing out.

Finally, PwC took second in new market cap audited, with a big boost from semiconductor manufacturer Global Foundries Inc.’s $32.1 billion.

Data for the quarterly rankings are provided by Ideagen Audit Analytics, a premium online intelligence service delivering audit, regulatory and disclosure analysis. Reach them at (508) 476-7007,

Total postsecondary spring enrollment grew 3.2% year-over-year, according to a report.

The National Student Clearinghouse Research Center published the latest edition of its

The report found that undergraduate enrollment grew 3.5% and reached 15.3 million students, but remains below pre-pandemic levels (378,000 less students). Graduate enrollment also increased to 7.2%, higher than in 2020 (209,000 more students).

(Read more:

Community colleges saw the largest growth in enrollment (5.4%), and enrollment increased for all undergraduate credential types. Bachelor’s and associate programs grew 2.1% and 6.3%, respectively, but remain below pre-pandemic levels.

Most ethnoracial groups saw increases in enrollment this spring, with Black and multiracial undergraduate students seeing the largest growth (10.3% and 8.5%, respectively). The number of undergraduate students in their twenties also increased. Enrollment of students between the ages of 21 and 24 grew 3.2%, and enrollment for students between 25 and 29 grew 5.9%.

For the third consecutive year, high vocational public two-years had substantial growth in enrollment, increasing 11.7% from 2023 to 2024. Enrollment at these trade-focused institutions have increased nearly 20% since pre-pandemic levels.

Jordan Vonderhaar/Photographer: Jordan Vonderhaar/

The Internal Revenue Service has released

The Inflation Reduction Act of 2022 amended Sec. 55 to impose the CAMT based on the “adjusted financial statement income” of an “applicable corporation” for taxable years beginning in 2023.

Among other details, proposed regs provide that “applicable corporation” means any corporation (other than an S corp, a regulated investment company or a REIT) that meets either of two average annual AFSI tests depending on financial statement net operating losses for three taxable years and whether the corporation is a member of a foreign-parented multinational group.

Prior to the publication of any final regulations relating to the CAMT, the Treasury and the IRS will issue a notice of proposed rulemaking. Notice 2025-27 will be in IRB: 2025-26, dated June 23.

Citigroup lifts banking curbs on gun makers and sellers

Total college enrollment rose 3.2%

Stocks making the biggest moves midday: BMBL, DG, SIG, PINS

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Economics1 week ago

Economics1 week agoMAGA: protecting the homeland from Canadian bookworms

-

Economics6 days ago

Economics6 days agoElon Musk says Trump’s spending bill undermines the work DOGE has been doing

-

Personal Finance6 days ago

Personal Finance6 days agoHarvard, Trump international enrollment battle affects college applicants

-

Accounting6 days ago

Accounting6 days agoHighest paid jobs in corporate accounting

-

Personal Finance1 week ago

Personal Finance1 week agoHow to pay college tuition bills with your 529 plan

-

Economics1 week ago

Economics1 week agoHow young voters helped to put Trump in the White House

-

Finance6 days ago

Finance6 days agoGameStop shares rise as retailer meme stock buys first bitcoin batch, scooping up $500 million

-

Personal Finance6 days ago

Personal Finance6 days agoCrypto in 401(k) plans: Trump administration eases rules