Accounting

FASB plans updates on contract assets and liabilities, and credit losses

The Financial Accounting Standards Board has decided to tweak some of its standards related to contract assets and liabilities for construction contractors in response to recommendations from its Private Company Council, as well as credit losses for financial institutions.

During a meeting last week, according to a

FASB also discussed another PCC project at the meeting on the application of the credit losses standard to current accounts receivable and contract assets arising from revenue transactions. It decided that private companies and not-for-profit entities (except for nonprofit conduit bond obligors) would be eligible for a simplified approach. FASB endorsed the PCC’s decision that the scope of the simplified approach would be current accounts receivable and contract asset balances arising from transactions accounted for under FASB’s revenue recognition standard.

Patrick Dorsman/Financial Accounting Foundation

FASB also backed the PCC’s decision to provide a recognition and measurement practical expedient and, for entities that elect the practical expedient, an accounting policy election designed to simplify the credit loss allowance determination. An entity that opts for the practical expedient wouldn’t be required to adjust historical loss information to reflect changes related to relevant economic data. The entity instead would assume that current economic conditions as of the balance sheet date will persist throughout the forecast period.

An entity that elects the practical expedient would be allowed to make an accounting policy election to consider subsequent cash collection after the balance sheet date but prior to the date the financial statements are available to be issued.

FASB endorsed the PCC’s decision to require an entity to disclose when the practical expedient and accounting policy election have been used, as well as to require a prospective transition method, with the ability for an entity to forgo a preferability assessment the first time it elects the practical expedient and the accounting policy election.

As with the contract assets and liability changes, FASB asked its staff to draft a proposed accounting standards update that can be voted on by written ballot, along with a 45-day comment period for the proposed update.

FASB chair Richard Jones and board member Hillary Salo suggested during the meeting that similar changes might be considered for public companies, although other board members seemed skeptical about the need for it. The board members seem to be open to at least including a question in the proposal about whether public companies want to use the practical expedient.

A Republican attempt to block states from enforcing new artificial intelligence rules over the next decade has drawn growing bipartisan objections, exposing tension in Washington over allowing for more unchecked AI development.

The proposal, buried on pages 278 and 279 in the sweeping tax bill passed by the House last month, has drawn sharp criticism from Republican Representative Marjorie Taylor Greene and Senator Marsha Blackburn, as well as Democratic Senators Ed Markey and Elizabeth Warren. More than 200 state lawmakers from both parties also urged Congress this week to scrap the measure.

“We have no idea what AI will be capable of in the next 10 years,” Greene

Markey and Warren have also been forceful in pushing back against the measure, arguing that it violates Senate rules that bill language included in the budget reconciliation process must relate to spending. “This backdoor AI moratorium is not serious. It’s not responsible. And it’s not acceptable,” Markey said. Meanwhile, Senate Commerce Chair Ted Cruz (R-Texas) has said he’s “not certain if that provision will survive,” though he has expressed support for it.

Since returning to the White House, President Donald Trump has taken steps to

But bipartisan resistance to the proposed moratorium on AI rules highlights a fierce divide in Washington over how much to let the industry regulate itself.

Congress has yet to pass a federal framework on AI, which has effectively left the states to take the lead on figuring out how to set rules around the technology. California, New York, Utah and dozens of others have introduced or enacted AI laws in recent years, including bills to address concerns about data privacy, copyright and bias raised by the technology.

If Congress backs away from the proposal, it would mark a setback for top AI developers. In March, OpenAI asked the White House to

So far, the leading AI companies have largely stayed quiet as the fight over the measure plays out. Meta Platforms Inc. declined to comment. Alphabet Inc.’s Google didn’t respond to a request for comment. OpenAI declined to comment beyond its previous policy suggestions.

TechNet, a trade group representing Google, OpenAI and other tech companies, echoed the ChatGPT maker’s concerns about the “developing patchwork” of state AI bills. “In 2025, over 1000 AI bills have been introduced in state legislatures — many containing incompatible rules and requirements,” Linda Moore, chief executive officer of TechNet, said in a statement to Bloomberg News. “A consistent national approach is critical,” she added, to address AI risks and “ensure America remains the global leader in innovation for generations to come.”

Anthropic, a safety-focused AI startup that has called for more regulation generally,

“Ten years is a long time,” Anthropic CEO Dario Amodei said at the company’s developer conference on May 22, speaking about the moratorium. “It’s one thing to say, ‘We don’t have to grab the steering wheel now.’ It’s another thing to say, ‘We’re going to rip out the steering wheel and we can’t put it back in for 10 years.'”

Some Republican senators have raised doubts that the AI provision can pass through the reconciliation process, but this camp has also expressed support for an interim ban on state rules to avoid an overly fragmented and complex regulatory landscape.

“I wouldn’t put my money on anything right now until it actually passes,” John Curtis, a Republican senator from Utah, previously

State legislators, however, worry that the provision would rob them of the ability to protect their constituents from the rapidly evolving technology.

“Over the next decade, AI will raise some of the most important public policy questions of our time,” state lawmakers from 49 states wrote in a

Enjoy complimentary access to top ideas and insights — selected by our editors.

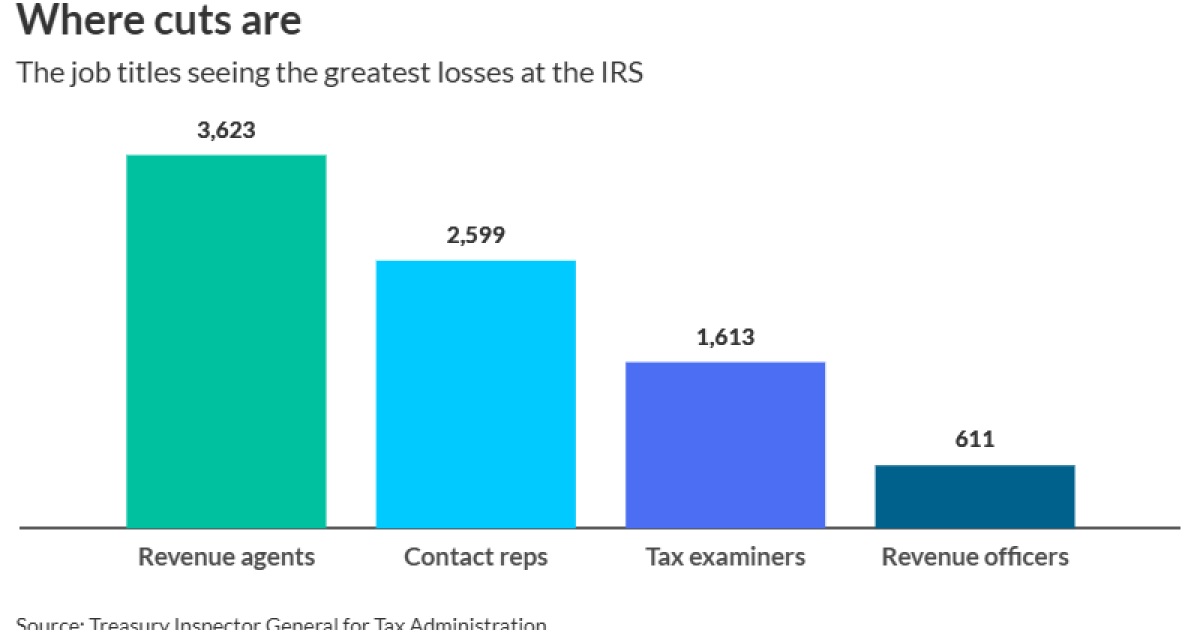

This week’s stats focus in part on the job titles seeing the greatest losses at the IRS during layoffs; as well as the states that have proposed or passed alternatives to the 150-hour rule; the percentage of master’s in accounting program applicants since 2020; the number of PwC employees laid off in May; the projected size of Deloitte’s new New York City headquarters; and the amount of 2026 HSA annual contribution limits, depending on coverage.

CrowdStrike Holdings Inc. said U.S. officials have asked for information related to the accounting of deals it’s made with some customers and said the cybersecurity firm is cooperating with the inquiry.

The Austin, Texas-based company said in a filing Wednesday that it has gotten “requests for information” from the U.S. Department of Justice and the Securities and Exchange Commission “relating to the company’s recognition of revenue and reporting of ARR for transactions with certain customers.” ARR refers to annual recurring revenue, a measure of earnings from subscriptions.

The company said the federal officials have also sought information related to a CrowdStrike update last year that crashed Windows operating systems around the world.

“The company is cooperating and providing information in response to these requests,” the filing states.

U.S. prosecutors and regulators have been investigating a $32 million deal between CrowdStrike and a technology distributor, Carahsoft Technology Corp., to provide cybersecurity tools to the Internal Revenue Service, Bloomberg News first reported in February. The IRS never purchased or received the products, Bloomberg News

The investigators are probing what senior CrowdStrike executives may have known about the $32 million deal and are examining other transactions made by the cybersecurity firm, Bloomberg News

Asked for comment about the filing, CrowdStrike spokesperson Brian Merrill said, “As we have told Bloomberg repeatedly, this is old news and we stand by the accounting of the transaction.”

A lawyer for Carahsoft previously declined to comment on the federal investigations, and representatives didn’t respond to subsequent requests for comment about them.

-

Economics1 week ago

Economics1 week agoElon Musk says Trump’s spending bill undermines the work DOGE has been doing

-

Accounting1 week ago

Accounting1 week agoHighest paid jobs in corporate accounting

-

Blog Post5 days ago

Blog Post5 days agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics1 week ago

Economics1 week agoHow young voters helped to put Trump in the White House

-

Personal Finance1 week ago

Personal Finance1 week agoHarvard, Trump international enrollment battle affects college applicants

-

Economics6 days ago

Economics6 days agoWhy the president must not be lexicographer-in-chief

-

Personal Finance1 week ago

Personal Finance1 week agoCrypto in 401(k) plans: Trump administration eases rules

-

Finance1 week ago

Finance1 week agoVail Resorts, GameStop and more