Accounting

GASB aims to align with Financial Data Transparency Act

![]()

The Financial Data Transparency Act has significant implications for the modernization of government financial reporting. Against this backdrop, the latest Governmental Accounting Standards Board meeting on Nov. 13 was particularly exciting due to its focus on advancing the digital financial reporting taxonomy — a transformative initiative poised to shape the future of government financial reporting.

The meeting showcased the board’s progress, deliberations and alignment with emerging regulatory and technological trends, signaling a pivotal moment for the evolution of public sector reporting. GASB senior project manager Paulina Haro presented her report and recommended paths forward in the meeting.

The board discussed progress in the development of a digital financial reporting taxonomy aimed at modernizing and standardizing electronic reporting practices. This initiative builds on seven years of electronic financial reporting monitoring, evolving from observation and exploration to an actionable framework for voluntary implementation. The taxonomy seeks to enhance usability, data accuracy and efficiency for users, preparers and other stakeholders in the government financial reporting ecosystem. Collaboration with internal teams, former fellows and external experts has paved the way for the board to propose a clear path forward.

The project will initially focus on GASB GAAP requirements, with future expansions considered based on stakeholder requests. Haro emphasized that using the term ACFR, or the Annual Comprehensive Financial Report, was problematic and too broad as a starting point. The intent is to start with a foundational structure and move forward from there.

The digital taxonomy will cover key components of financial reporting, including basic financial statements, notes to financial statements and required supplementary information such as management’s discussion and analysis. Phase One will establish a foundational framework for GAAP reporting, avoiding selective prioritization of data points to maintain the integrity and completeness of GASB standards. Haro emphasized it’s important to create the impression the Taxonomy Team is not “picking and choosing what is essential and not.” The users’ voices would be critical to the process. Subsequent phases may incorporate additional elements like supplementary and non-GAAP reporting components, pending stakeholder input and board decisions.

Board members emphasized the importance of retaining GASB’s monitoring activity, which ensures the board remains informed about technological advancements and their implications for government financial reporting. Monitoring provides critical insights into evolving user and preparer needs, as well as the broader impacts of technology on financial reporting processes. This understanding is key to maintaining the relevance of GASB standards and ensuring alignment with modern reporting practices. The monitoring activity will function as an ongoing effort, enabling the board to anticipate and respond to technological shifts effectively.

Stakeholder engagement will play a crucial role in shaping the taxonomy. The board proposed forming a consultative group to guide the project. This group will include representatives from diverse sectors, such as accountants, auditors, data technologists and software vendors. By bringing together expertise from various fields, the group aims to ensure the taxonomy meets the needs of all stakeholders while addressing technical and practical challenges. Board members highlighted the importance of including participants who understand both accounting principles and technological systems to bridge gaps and enhance collaboration.

The board plans to publish an initial exposure document for public comment in 2025. This document will introduce selected components of the taxonomy, including financial statements, notes and required supplementary information, to showcase its architectural design and functionality. These components were chosen to provide a comprehensive but manageable overview, allowing stakeholders to evaluate the taxonomy’s structure and usability. The board acknowledged the challenges of presenting complex technological and accounting concepts in an accessible manner, committing to including explanatory materials tailored to different audiences.

The project’s timeline reflects both ambition and caution. Board members praised the team for exceeding expectations in their progress so far but emphasized the need to balance urgency with thoroughness. The taxonomy’s design must address diverse stakeholder needs while aligning with emerging regulatory frameworks such as the Financial Data Transparency Act. The board committed to monitoring FDTA developments to ensure the taxonomy remains relevant and adaptable to future requirements.

Looking ahead, the board reaffirmed its commitment to the project as a priority initiative, with updates and deliverables integrated into upcoming technical plans. GASB chair Joel Black said this will be a technology project, with its own classification and will not end with a new standard. Beginning in February 2025, the board will receive detailed presentations on taxonomy architecture and design choices, while continuing to refine the framework based on internal deliberations and external feedback. By maintaining a collaborative, phased approach, the board aims to deliver a taxonomy that enhances the accuracy, usability and efficiency of government financial reporting in an increasingly digital landscape.

As CPA firms grow into the $10 million to $100 million revenue range, operational complexity increases, especially during peak periods like tax season. Leadership must prioritize strategies to reduce friction, improve efficiency, and enhance the client and staff experience. Algorithms, defined as systematic processes designed to solve specific problems, are a key enabler in achieving these goals.

By automating repetitive tasks, algorithms can save hundreds of hours during the busiest times, allowing staff to focus on high-value activities and improving client satisfaction.

Four specific examples of areas where algorithms can help firms are described below, but no matter the area, adopting algorithms requires deliberate planning and execution:

1. Identify opportunities

- Assess pain points in tax, audit, scheduling, and advisory workflows.

- Identify routine tasks that consume excessive time during peak periods.

2. Gather and analyze data

- Evaluate the availability of client and internal data to support automation.

- Determine additional data needs and acquisition strategies.

3. Experiment and iterate:

- Pilot small-scale solutions, such as automating a single tax form process or scheduling tool.

- Refine based on results and user feedback.

4. Scale and integrate:

- Implement successful pilots across teams or departments.

- Provide staff training to maximize adoption and effectiveness.

5. Measure and optimize:

- Use key performance indicators such as time savings, error reduction, and client satisfaction to assess the impact.

Quick wins for immediate impact

To build momentum, start with high-impact initiatives:

- Tax workflow automation: Automate the completion, e-signature, and filing of forms like 8879 and 4868, and notify clients of estimated tax payments due via an automated communication system.

- Audit data preparation: Use algorithms to download client data, generate trial balances, and perform risk analysis.

- Scheduling optimization: Implement an algorithm-driven scheduling tool to automate meeting coordination, resource allocation, and deadline tracking.

Conclusion

Algorithms are transformative tools that empower CPA firms to operate more efficiently while delivering enhanced value. By automating routine tasks in tax, audit, scheduling, and advisory services, firms can save significant time, improve accuracy, and foster stronger client relationships. The key to success lies in adopting a strategic roadmap — identifying opportunities, running experiments, and scaling solutions. Mindset is paramount.

For CPA firms navigating the challenges of growth and complexity, algorithms represent a critical investment in operational excellence, enabling staff to focus on what truly matters: delivering exceptional client experiences. Think — plan — grow!

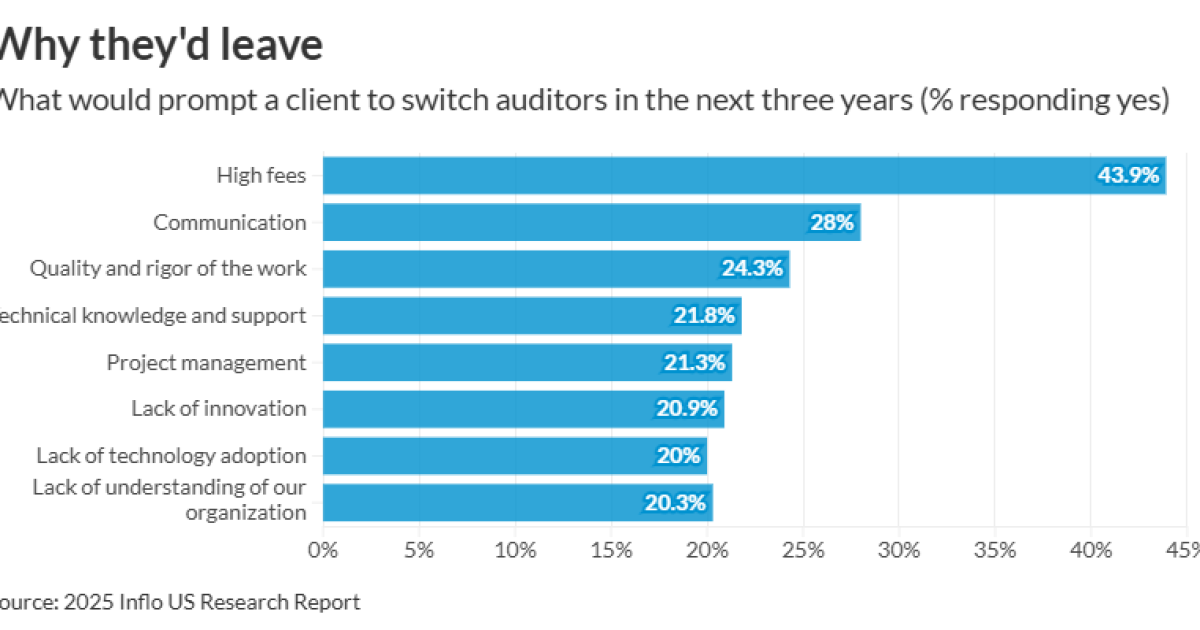

More than two-thirds (70%) of U.S. audit clients are ready to change firms within the next three years, according to a new report.

Inflo’s “Creating a New Audit Experience for U.S. Businesses”

Clients with the most employees (250 employees or more) were the highest to report it was “very likely” they would switch firms. Meanwhile, clients with fewer employees (less than 50 employees) were the highest to report it was “very unlikely” they’d switch firms.

By far the most common reason causing a client to look for a new firm was high fees (44%). When asked how much more clients would be willing to pay for an audit that “gave you more value,” respondents answered 5-10% more (33%), 11-20% (31%) and 21-30% (14%). Five percent of respondents answered “nothing.”

Subsequently, clients said the leading factors influencing their decision to accept or resist fee increases were perceived value and quality of service (42%), relationship with the audit firm (40%), meeting deadlines (39%), level of justifications and transparency regarding an increasing (35%), responsive communication (35%) and the frequency of previous fee increases (34%).

(Read more:

The second most common reason causing a client to switch auditors was communication (28%), followed by quality and rigor of the work (24%), technical knowledge and support (22%), project management (21%), lack of innovation (21%) and lack of technology adoption (20%). Sixteen percent of respondents reported, “We are not experiencing any issues.”

“This research makes one thing clear: U.S. businesses are demanding a better audit experience,” Inflo CEO Mark Edmondson said in a statement. “From high fees based on outdated pricing models to technology that hasn’t changed since the 1990s, the approach of many audit firms is driving business away.”

Additionally, nearly half of respondents (45%) said they’d like auditors to improve on the use of technology to add more value to their audits, followed by the time needed from their team and insights on their organization (38% each).

“The good news is that clients care about their audits. They want them to play a key role in driving operational improvement and consistent business growth,” Edmondson said. “Audit firms that act on the report’s findings will be rewarded with rising fee incomes and a continually growing client base.”

Stocks making the biggest moves midday: WBD, MODG, SATS, AAPL

Inflation fears receded in May as Trump eased some tariff threats, New York Fed survey shows

Walmart taps own fintech firm for credit cards after Capital One exit

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Blog Post1 week ago

Blog Post1 week agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics1 week ago

Economics1 week agoWhy the president must not be lexicographer-in-chief

-

Finance1 week ago

Finance1 week agoThis is why Jamie Dimon is so gloomy on the economy

-

Accounting1 week ago

Accounting1 week agoSteinhoff fraud trial moved to South Africa’s high court

-

Personal Finance7 days ago

Personal Finance7 days agoWhat the national debt, deficit mean for your money

-

Personal Finance1 week ago

Personal Finance1 week agoHow to save on summer travel in 2025

-

Personal Finance1 week ago

Personal Finance1 week agoDenmark raises retirement age to 70; U.S. might follow

-

Finance1 week ago

Finance1 week agoWhy JPMorgan hired NOAA’s Sarah Kapnick as chief climate scientist