Accounting

LGBTQ financial planning for second Trump administration

Financial planners who work with LGBTQ clients are helping them prepare for a potential rollback of civil rights under President-elect Donald Trump’s second administration.

Expressing empathy for

“Being a great listener” and understanding that “people are going to have unease about investments specifically” when they believe that their rights are under attack can go a long way, said Lindsey Young, founder of Baltimore-based registered investment advisory firm

“It’s just recognizing that it could be a hard time,” Young said. “It’s just saying, ‘I’m here to help you.’ Saying that is really important.”

READ MORE:

Marriage rights are rightfully getting “a lot of attention when it comes to the political battle for human rights, and rightfully so,” according to Leighann Miko, founder of Los Angeles- and Portland, Oregon-based RIA firm

“Often as planners, we default to our technical skills to plan the risk away,” Miko said. “While helpful and usually the reason our clients seek us out, it’s equally important to provide a safe space for our clients to express their fears and concerns, especially as it relates to their financial lives. As a marginalized community that has had to fight tooth and nail for basic human rights, LGBTQ clients are exhausted. Be patient, be willing to see things through a different lens, and listen with empathy.”

Even before the election, LGBTQ advocates had been tracking a surge in

For 2.7 million LGBTQ people over the age of 50, the rankings for the best states to retire in vary greatly from a list that doesn’t take their civil liberties into account,

“Including even a minimal consideration of a state’s treatment of LGBTQ people would result in a different ranking of states altogether,” MAP wrote in the report. “MAP’s research team decided to compare Bankrate’s analysis to our publicly available data on state policy to illustrate how state rankings can change dramatically when you incorporate laws and policies that shape the lives and experiences of LGBTQ people. Our findings show strikingly different results and highlight a very different set of considerations for LGBTQ adults deciding where to spend their golden years.”

READ MORE:

As inviting as a new state may seem when considering policies, clients will need to weigh factors such as whether their residence may affect their pension and a possible higher cost of living if they depart from a southern state to a coastal state like California or New York, Young noted. Since fear can lead to

“The big thing is to say, ‘Let’s step back and run the numbers.’ I think there’s a temptation among many people to say, ‘I’m going to move, I’m going to get out and we’ll figure it out when we get there,'” Young said. “If they were to move, it actually makes them feel much more confident with that move, as opposed to just panicking.”

In terms of the possible challenges to same-sex marriage, advisors and their clients could seek second-parent adoptions, update the beneficiaries listed in a will or a trust or purchase life insurance to cover estate taxes if one of the spouses dies, Miko noted. Those possible steps come on top of other necessary ones, if there is a Supreme Court decision overturning same-sex marriage rights or if individual states pass their own restrictions, she said.

“Many of the pre-2015 safeguards will have to be implemented once again, which still don’t quite level the playing field compared to legally recognized marriage rights,” Miko said. “For example, a non-married partner does not automatically inherit assets upon the death of a partner, and, in community property states, the surviving partner would not receive the tax benefit of a full step-up in cost basis on the inherited asset, such as a home.”

READ MORE:

She and Young pointed out how marriage affects the policy of unlimited gifts between spouses without estate taxes and the requirement for clients to get current and valid power of attorney and advanced health care directive documents on file.

“The good thing is that there are many LGBTQ estate attorneys who have been doing this for decades,” Young said. “That provides the best protection against potential changes in the law.”

As CPA firms grow into the $10 million to $100 million revenue range, operational complexity increases, especially during peak periods like tax season. Leadership must prioritize strategies to reduce friction, improve efficiency, and enhance the client and staff experience. Algorithms, defined as systematic processes designed to solve specific problems, are a key enabler in achieving these goals.

By automating repetitive tasks, algorithms can save hundreds of hours during the busiest times, allowing staff to focus on high-value activities and improving client satisfaction.

Four specific examples of areas where algorithms can help firms are described below, but no matter the area, adopting algorithms requires deliberate planning and execution:

1. Identify opportunities

- Assess pain points in tax, audit, scheduling, and advisory workflows.

- Identify routine tasks that consume excessive time during peak periods.

2. Gather and analyze data

- Evaluate the availability of client and internal data to support automation.

- Determine additional data needs and acquisition strategies.

3. Experiment and iterate:

- Pilot small-scale solutions, such as automating a single tax form process or scheduling tool.

- Refine based on results and user feedback.

4. Scale and integrate:

- Implement successful pilots across teams or departments.

- Provide staff training to maximize adoption and effectiveness.

5. Measure and optimize:

- Use key performance indicators such as time savings, error reduction, and client satisfaction to assess the impact.

Quick wins for immediate impact

To build momentum, start with high-impact initiatives:

- Tax workflow automation: Automate the completion, e-signature, and filing of forms like 8879 and 4868, and notify clients of estimated tax payments due via an automated communication system.

- Audit data preparation: Use algorithms to download client data, generate trial balances, and perform risk analysis.

- Scheduling optimization: Implement an algorithm-driven scheduling tool to automate meeting coordination, resource allocation, and deadline tracking.

Conclusion

Algorithms are transformative tools that empower CPA firms to operate more efficiently while delivering enhanced value. By automating routine tasks in tax, audit, scheduling, and advisory services, firms can save significant time, improve accuracy, and foster stronger client relationships. The key to success lies in adopting a strategic roadmap — identifying opportunities, running experiments, and scaling solutions. Mindset is paramount.

For CPA firms navigating the challenges of growth and complexity, algorithms represent a critical investment in operational excellence, enabling staff to focus on what truly matters: delivering exceptional client experiences. Think — plan — grow!

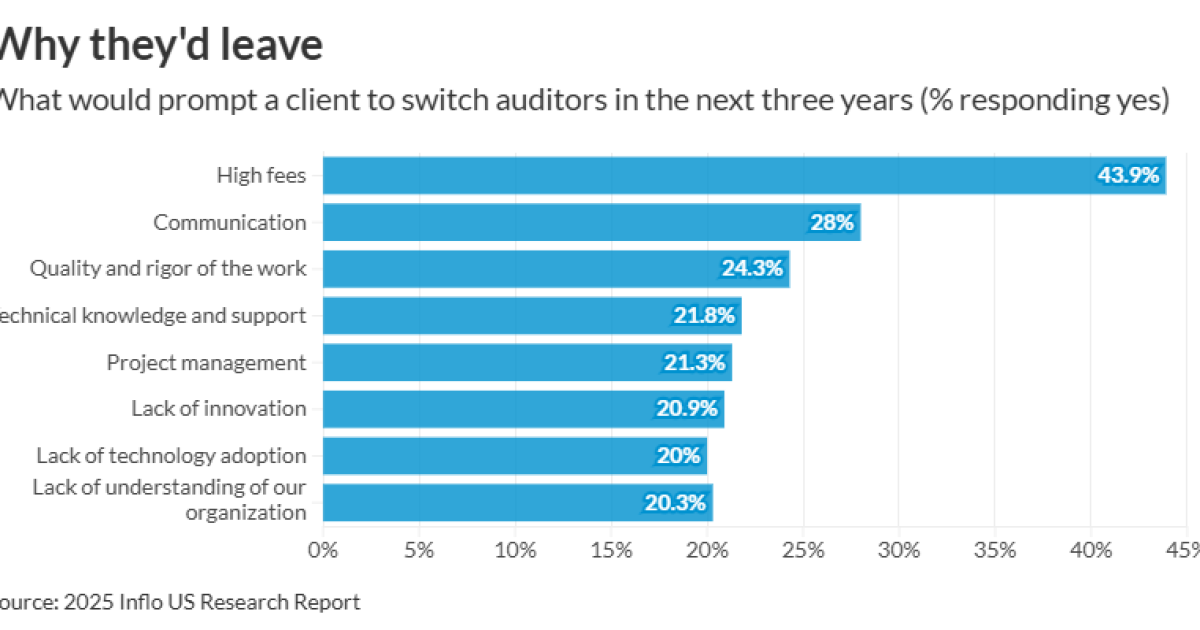

More than two-thirds (70%) of U.S. audit clients are ready to change firms within the next three years, according to a new report.

Inflo’s “Creating a New Audit Experience for U.S. Businesses”

Clients with the most employees (250 employees or more) were the highest to report it was “very likely” they would switch firms. Meanwhile, clients with fewer employees (less than 50 employees) were the highest to report it was “very unlikely” they’d switch firms.

By far the most common reason causing a client to look for a new firm was high fees (44%). When asked how much more clients would be willing to pay for an audit that “gave you more value,” respondents answered 5-10% more (33%), 11-20% (31%) and 21-30% (14%). Five percent of respondents answered “nothing.”

Subsequently, clients said the leading factors influencing their decision to accept or resist fee increases were perceived value and quality of service (42%), relationship with the audit firm (40%), meeting deadlines (39%), level of justifications and transparency regarding an increasing (35%), responsive communication (35%) and the frequency of previous fee increases (34%).

(Read more:

The second most common reason causing a client to switch auditors was communication (28%), followed by quality and rigor of the work (24%), technical knowledge and support (22%), project management (21%), lack of innovation (21%) and lack of technology adoption (20%). Sixteen percent of respondents reported, “We are not experiencing any issues.”

“This research makes one thing clear: U.S. businesses are demanding a better audit experience,” Inflo CEO Mark Edmondson said in a statement. “From high fees based on outdated pricing models to technology that hasn’t changed since the 1990s, the approach of many audit firms is driving business away.”

Additionally, nearly half of respondents (45%) said they’d like auditors to improve on the use of technology to add more value to their audits, followed by the time needed from their team and insights on their organization (38% each).

“The good news is that clients care about their audits. They want them to play a key role in driving operational improvement and consistent business growth,” Edmondson said. “Audit firms that act on the report’s findings will be rewarded with rising fee incomes and a continually growing client base.”

Stocks making the biggest moves midday: WBD, MODG, SATS, AAPL

Inflation fears receded in May as Trump eased some tariff threats, New York Fed survey shows

Walmart taps own fintech firm for credit cards after Capital One exit

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Blog Post1 week ago

Blog Post1 week agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics1 week ago

Economics1 week agoWhy the president must not be lexicographer-in-chief

-

Finance1 week ago

Finance1 week agoThis is why Jamie Dimon is so gloomy on the economy

-

Accounting1 week ago

Accounting1 week agoSteinhoff fraud trial moved to South Africa’s high court

-

Personal Finance7 days ago

Personal Finance7 days agoWhat the national debt, deficit mean for your money

-

Personal Finance1 week ago

Personal Finance1 week agoHow to save on summer travel in 2025

-

Personal Finance1 week ago

Personal Finance1 week agoDenmark raises retirement age to 70; U.S. might follow

-

Finance1 week ago

Finance1 week agoWhy JPMorgan hired NOAA’s Sarah Kapnick as chief climate scientist