Accounting

Practice Profile: Dreaming up a better tax season

Accounting firm ASE Group does not do taxes on April 15, and its employees don’t work Fridays.

That’s the vision founder Al-Nesha Jones conjured up when she asked herself: “What would tax season look like if we had our way?”

Flexibility was a foundational principle for Jones in establishing her New Jersey-based practice in 2016, after she felt rushed back to work at her corporate job following maternity leave.

tamara fleming photography

By the time the pandemic hit four years later, Jones and her fully remote team of four had already mastered the new working models that COVID would normalize, but that period also inspired her to expand the practice from pure tax preparation to full-service accounting.

“We were catering to client needs — whatever brought the money in,” Jones recalled. “We didn’t get serious about [expanding] until the pandemic, when we realized people wanted more. Providing tax prep work was not enough. In a short period, people became day traders, moved out of state … We needed to pivot in the way we operated. We now offer a full-service solution to clients — accounting, tax prep, advisory. It entirely changed how we feel about the profession, how busy season feels. All good changes came out of it.”

However, Jones acknowledged, there was one bad change: having to cut the clients that did not align with the pivot.

“We like to think of it as finding a place that’s a better fit for them,” she explained.

The firm currently serves about 150 clients — specifically individual small-business owners who live or work in New Jersey, New York or Pennsylvania and are sole proprietors or single-member LLCs — though ASE is “slowly working [its] way down to 100.”

Jones exercises empathy in letting these clients go, explaining that the firm has outgrown their more simple service requirements. “We give them plenty of time to evaluate their options,” she said. “When we are parting ways, we don’t say, ‘You can’t stay anymore,’ we give a one-on-one explanation that, ‘You’d be a one-off to us, and that’d be a disservice to you.”

Jones also gives departing clients references to other accountants that specialize in their industry, with the caveat that ASE gets no commission, and they should do their own due diligence.

“We felt better not just sending them out in the wild,” she said, adding that these conversations often happen right after tax season, “so they have six-plus months to seek another accountant. We also provide one hour of transitional services at no additional charge. We gather documents; we are happy to do that at no additional fee. The intent is to not make it any more difficult than it needs to be. I’m training

my own brain: This is better for everyone. We do what’s best for them, and better for us also. Better for both parties. We get the capacity back to serve the clients we’re best equipped to serve.”

What Jones has also found to be universally beneficial is her team’s four-day work week. While her staff is all women, Jones said that it just “sort of worked out that way” after the interviewing process yielded women (and mothers) as the best candidates.

“What I love about working with moms is they tend to get it done, with an any-means-necessary attitude,” Jones shared. “I don’t condone an environment where you burn yourselves out. Moms are creative in their solutions and pivot well. This team adjusts quickly to change.”

No-email Fridays

It was Jones’ own adjustment period, launching her firm with a newborn in tow after she “didn’t want to be rushed back to work sooner than ready” in her prior job, that inspired her team’s flexibility.

In April 2016, she started renting an office with a security deposit and a promise to the landlord that, although she didn’t currently have the first month’s rent, she soon would.

That June and July, she started paying for the office space in the building where ASE Group still resides, though she is the only one of her virtual team who comes in.

“In the first 20 months of running the business, I was bringing my daughter to work two to three times a week,” Jones shared. “I was on meetings with her, Zoom calls; I nursed during meetings. In hindsight it sounds crazy.”

Jones’ philosophy of balancing work and personal life persists in the way her firm supports colleagues who “all prioritize family,” whether that’s a sick child or caring for a parent, as long as staff is accountable and takes care of their work. Productivity is also expected in ASE’s shorter work weeks, which were born out of COVID.

“With so much going on, as a mom of three children, with remote learning, a husband working from home — it was a challenging time to take a small breather… I felt so unbalanced working five to six days a week,” she explained.

“I explored four-day work weeks during the summer to see how clients would adjust,” she continued. “They were the easiest. Then to see how we adjust. What efficiencies of a normal work day can get done in four days instead of five days. I absolutely work some Fridays because of travel and school schedules. But we schedule no meetings or calls on Fridays, with no exceptions.”

While employees can of course still get work done as necessary, instituting the no-email and no-calls rule is so staff “don’t create unnecessary expectations,” Jones explained. “Friday is all of our days off — no one sends messages to anybody. You get to enjoy your Friday off.”

Both this policy and ASE’s mandate to get clients’ tax preparation work done well before the Internal Revenue Service deadline requires planning and adjusting client messaging.

“We revamped the process and changed the way we communicate with clients,” Jones said. “We had to start from scratch and reverse-engineer how it would work. It started with what we wanted it to look like, not the systems or software, but blue-sky thinking, what tax season would look like if we had our way. What it would look like was: no surprises, talking to clients during the year. We talk to clients at least four times a year. We call 30 days before the estimated tax deadline.”

ASE Group works under internal deadlines. “We don’t care about the April 15 deadline for tax,” Jones said. “We only operate under our own deadlines, which tend to be at least two weeks before external deadlines. If, God forbid, we can’t meet internal deadlines, we can breathe easy with a buffer in place.”

ASE staff meet these self-imposed deadlines with more frequent client communication and weekly team calls internally.

Jones said it’s OK if two or three clients end up falling closer to the April or October deadlines, but “if half of clients go on extension or wait until October, there’s panic. It doesn’t have to be that way, and if the client likes to operate like that, it’s not a good fit.”

Advisory is the cure

Jones was not even sure the accounting profession was a fit for her until she participated in the Goldman Sachs 10,000 Small Businesses program and learned to conceptualize a new future for her career.

“I was thinking, ‘I’m not a good accountant, I can’t do this, it’s way too stressful,'” she explained. “It was realizing it’s not tax I hated, but the constant working toward deadlines, doing things last minute, all a surprise. But it’s not. It’s one of the easiest, most predictable industries. You can plan due dates. Operating with blue-sky thinking, I could step away from what I’m doing now, and it taught me what it could be like and how to make that a reality.”

ASE Group’s lower-stress tax seasons involve scheduled phone calls to check in on clients’ current financial needs and lean more into the advisory side of tax planning.

“What you need first, is advisory all throughout the year,” she said. “So that at the end of the year it’s not a pop quiz — what am I going to do on my taxes? It doesn’t have to be a surprise. I hate delivering bad news, and I also hate surprises. It’s like Groundhog Day, telling people [what to do on their taxes] … having the same conversations over and over again. People expected that they did all they needed all year, then dump it on their accountant. I’m not a magician. I felt so anxiety-ridden. The cure for that suffering is advisory.”

ASE’s regular client calls — scheduled six months out — also alleviate other common ailments, like financial anxiety and procrastination.

“It’s getting us in the position to help them reduce surprises,” Jones explained. “By the time tax season rolls around, it’s just filing season. Not strategizing season, not planning season. When a child has a test, like the SATs, they don’t show up on test day ready to study. When they show up to the test, they make sure they had a good night’s sleep, they ate breakfast, and they sharpened their pencils. All year is study season.”

The phone calls are mandatory, whether or not clients have updates. “Some clients don’t have anything new to tell you. Those clients don’t have to use all the time — if they get on the phone and tell me absolutely nothing … I’m happy to end the phone call early. The beauty is creating a routine, the consistency of it.”

Often, however, clients who think they have nothing new to report realize that they do when Jones and her colleagues engage them in more casual conversation leading to relevant life updates.

“Sometimes they struggle with financial anxiety, and don’t always want to tell you things aren’t great,” Jones shared. “The conversation is relaxed, and those conversations become more fluid and open.”

“We don’t want you to go on Google and Tiktok trying to be your own advisor,” she continued. “We ask that you allow us to prepare you for what creates an issue versus what doesn’t. We are talking in conversations about kids, family trips. In those conversations we have an agenda of listening to what they are saying … . If [for example] they are thinking of starting a new job, ‘We can help you complete a W-4.’ Something we can support you in.” AT

As CPA firms grow into the $10 million to $100 million revenue range, operational complexity increases, especially during peak periods like tax season. Leadership must prioritize strategies to reduce friction, improve efficiency, and enhance the client and staff experience. Algorithms, defined as systematic processes designed to solve specific problems, are a key enabler in achieving these goals.

By automating repetitive tasks, algorithms can save hundreds of hours during the busiest times, allowing staff to focus on high-value activities and improving client satisfaction.

Four specific examples of areas where algorithms can help firms are described below, but no matter the area, adopting algorithms requires deliberate planning and execution:

1. Identify opportunities

- Assess pain points in tax, audit, scheduling, and advisory workflows.

- Identify routine tasks that consume excessive time during peak periods.

2. Gather and analyze data

- Evaluate the availability of client and internal data to support automation.

- Determine additional data needs and acquisition strategies.

3. Experiment and iterate:

- Pilot small-scale solutions, such as automating a single tax form process or scheduling tool.

- Refine based on results and user feedback.

4. Scale and integrate:

- Implement successful pilots across teams or departments.

- Provide staff training to maximize adoption and effectiveness.

5. Measure and optimize:

- Use key performance indicators such as time savings, error reduction, and client satisfaction to assess the impact.

Quick wins for immediate impact

To build momentum, start with high-impact initiatives:

- Tax workflow automation: Automate the completion, e-signature, and filing of forms like 8879 and 4868, and notify clients of estimated tax payments due via an automated communication system.

- Audit data preparation: Use algorithms to download client data, generate trial balances, and perform risk analysis.

- Scheduling optimization: Implement an algorithm-driven scheduling tool to automate meeting coordination, resource allocation, and deadline tracking.

Conclusion

Algorithms are transformative tools that empower CPA firms to operate more efficiently while delivering enhanced value. By automating routine tasks in tax, audit, scheduling, and advisory services, firms can save significant time, improve accuracy, and foster stronger client relationships. The key to success lies in adopting a strategic roadmap — identifying opportunities, running experiments, and scaling solutions. Mindset is paramount.

For CPA firms navigating the challenges of growth and complexity, algorithms represent a critical investment in operational excellence, enabling staff to focus on what truly matters: delivering exceptional client experiences. Think — plan — grow!

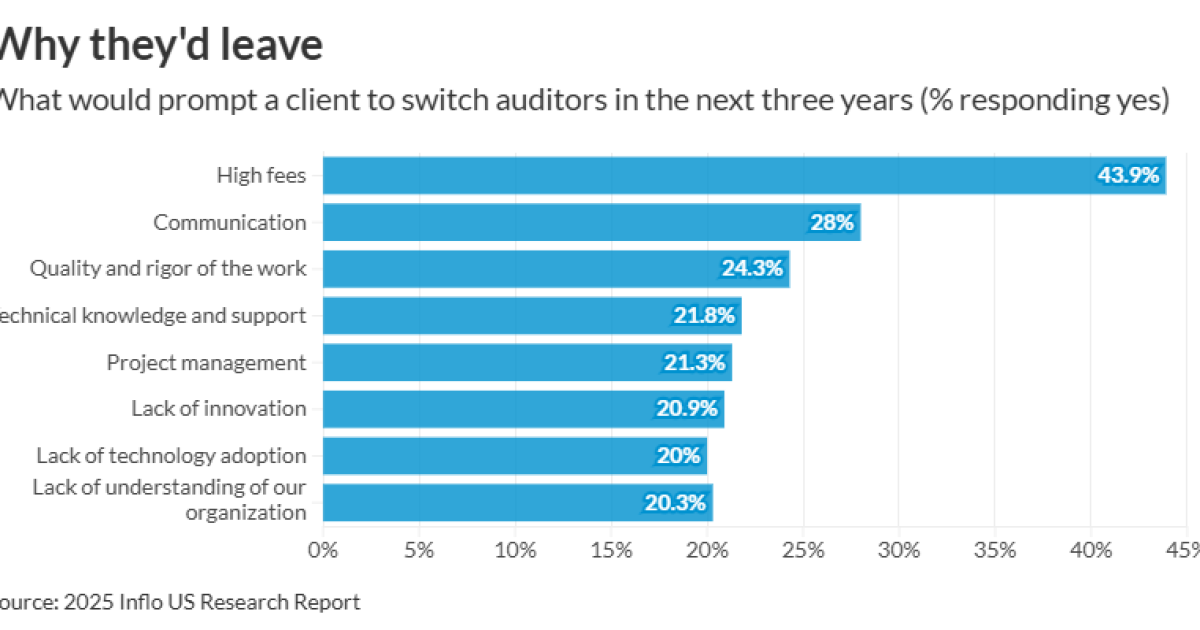

More than two-thirds (70%) of U.S. audit clients are ready to change firms within the next three years, according to a new report.

Inflo’s “Creating a New Audit Experience for U.S. Businesses”

Clients with the most employees (250 employees or more) were the highest to report it was “very likely” they would switch firms. Meanwhile, clients with fewer employees (less than 50 employees) were the highest to report it was “very unlikely” they’d switch firms.

By far the most common reason causing a client to look for a new firm was high fees (44%). When asked how much more clients would be willing to pay for an audit that “gave you more value,” respondents answered 5-10% more (33%), 11-20% (31%) and 21-30% (14%). Five percent of respondents answered “nothing.”

Subsequently, clients said the leading factors influencing their decision to accept or resist fee increases were perceived value and quality of service (42%), relationship with the audit firm (40%), meeting deadlines (39%), level of justifications and transparency regarding an increasing (35%), responsive communication (35%) and the frequency of previous fee increases (34%).

(Read more:

The second most common reason causing a client to switch auditors was communication (28%), followed by quality and rigor of the work (24%), technical knowledge and support (22%), project management (21%), lack of innovation (21%) and lack of technology adoption (20%). Sixteen percent of respondents reported, “We are not experiencing any issues.”

“This research makes one thing clear: U.S. businesses are demanding a better audit experience,” Inflo CEO Mark Edmondson said in a statement. “From high fees based on outdated pricing models to technology that hasn’t changed since the 1990s, the approach of many audit firms is driving business away.”

Additionally, nearly half of respondents (45%) said they’d like auditors to improve on the use of technology to add more value to their audits, followed by the time needed from their team and insights on their organization (38% each).

“The good news is that clients care about their audits. They want them to play a key role in driving operational improvement and consistent business growth,” Edmondson said. “Audit firms that act on the report’s findings will be rewarded with rising fee incomes and a continually growing client base.”

Walmart taps own fintech firm for credit cards after Capital One exit

Remaking the partnership model for young accountants

Boomer’s Blueprint: 4 ways algorithms can improve your accounting firm

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Blog Post1 week ago

Blog Post1 week agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics1 week ago

Economics1 week agoWhy the president must not be lexicographer-in-chief

-

Finance1 week ago

Finance1 week agoThis is why Jamie Dimon is so gloomy on the economy

-

Accounting1 week ago

Accounting1 week agoSteinhoff fraud trial moved to South Africa’s high court

-

Personal Finance7 days ago

Personal Finance7 days agoWhat the national debt, deficit mean for your money

-

Personal Finance1 week ago

Personal Finance1 week agoHow to save on summer travel in 2025

-

Personal Finance1 week ago

Personal Finance1 week agoDenmark raises retirement age to 70; U.S. might follow

-

Finance1 week ago

Finance1 week agoWhy JPMorgan hired NOAA’s Sarah Kapnick as chief climate scientist