Finance

Private student loan interest rates fall for 5- and 10-year terms

Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as “Credible” below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

The latest private student loan interest rates from the Credible marketplace, updated weekly. (iStock)

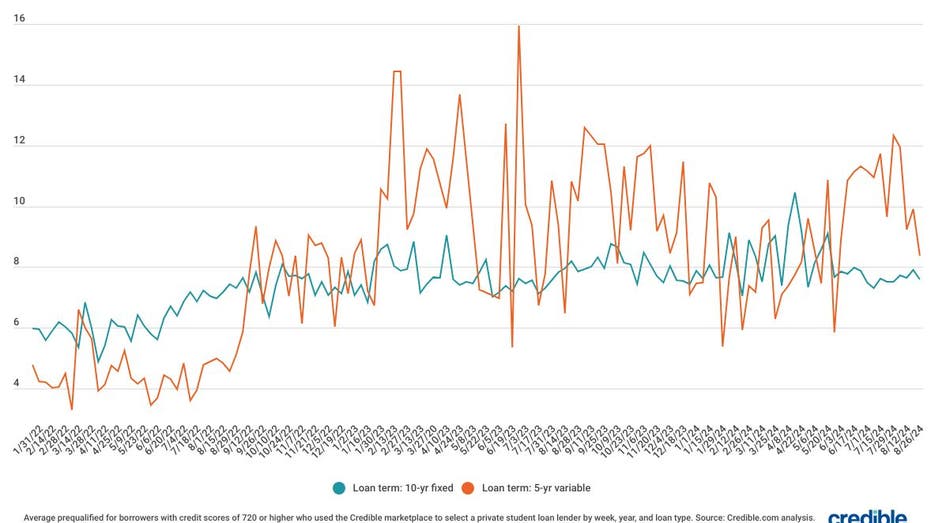

During the week of Aug. 26, 2024, average private student loan rates decreased for borrowers with credit scores of 720 or higher who used the Credible marketplace to take out 5-year variable-rate loans and 10-year fixed-rate loans.

- 10-year fixed rate: 7.59%, down from 7.89% the week before, -0.30

- 5-year variable rate: 8.38%, down from 9.92% the week before, -1.54

Through Credible, you can compare private student loan rates from multiple lenders.

For 10-year fixed private student loans, interest rates fell by 0.30 percentage points, while 5-year variable student loan interest plummeted by 1.54 percentage points.

Borrowers with good credit may find a lower rate with a private student loan than with some federal loans. For the 2024-25 academic school year, federal student loan rates will range from 6.53% to 9.08%. Private student loan rates for borrowers with good-to-excellent credit can be lower right now.

Because federal loans come with certain benefits, like access to income-driven repayment plans, you should always exhaust federal student loan options first before turning to private student loans to cover any funding gaps. Private lenders such as banks, credit unions, and online lenders provide private student loans. You can use private loans to pay for education costs and living expenses, which might not be covered by your federal education loans.

Interest rates and terms on private student loans can vary depending on your financial situation, credit history, and the lender you choose.

Private student loan rates (graduate and undergraduate)

Who sets federal and private interest rates?

Congress sets federal student loan interest rates each year. These fixed interest rates depend on the type of federal loan you take out, your dependency status and your year in school.

Private student loan interest rates can be fixed or variable and depend on your credit, repayment term and other factors. As a general rule, the better your credit score, the lower your interest rate is likely to be.

You can compare rates from multiple student loan lenders using Credible.

How does student loan interest work?

An interest rate is a percentage of the loan periodically tacked onto your balance — essentially the cost of borrowing money. Interest is one way lenders can make money from loans. Your monthly payment often pays interest first, with the rest going to the amount you initially borrowed (the principal).

Getting a low interest rate could help you save money over the life of the loan and pay off your debt faster.

What is a fixed- vs. variable-rate loan?

Here’s the difference between a fixed and variable rate:

- With a fixed rate, your monthly payment amount will stay the same over the course of your loan term.

- With a variable rate, your payments might rise or fall based on changing interest rates.

Comparison shopping for private student loan rates is easy when you use Credible.

Calculate your savings

Using a student loan interest calculator will help you estimate your monthly payments and the total amount you’ll owe over the life of your federal or private student loans.

Once you enter your information, you’ll be able to see what your estimated monthly payment will be, the total you’ll pay in interest over the life of the loan and the total amount you’ll pay back.

About Credible

Credible is a multi-lender marketplace that empowers consumers to discover financial products that are the best fit for their unique circumstances. Credible’s integrations with leading lenders and credit bureaus allow consumers to quickly compare accurate, personalized loan options – without putting their personal information at risk or affecting their credit score. The Credible marketplace provides an unrivaled customer experience, as reflected by over 7,700 positive Trustpilot reviews and a TrustScore of 4.8/5.

Donald Trump’s new travel ban is coming into effect

Sending the National Guard to LA is not about stopping rioting

China’s EV race to the bottom leaves a few possible winners

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Blog Post1 week ago

Blog Post1 week agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics1 week ago

Economics1 week agoWhy the president must not be lexicographer-in-chief

-

Finance1 week ago

Finance1 week agoThis is why Jamie Dimon is so gloomy on the economy

-

Personal Finance1 week ago

Personal Finance1 week agoU.S. birth rate drop outpaces policy response, raising future concerns

-

Accounting1 week ago

Accounting1 week agoSteinhoff fraud trial moved to South Africa’s high court

-

Economics1 week ago

Economics1 week agoGerman inflation May 2025

-

Personal Finance6 days ago

Personal Finance6 days agoWhat the national debt, deficit mean for your money

-

Personal Finance1 week ago

Personal Finance1 week agoHow to save on summer travel in 2025