Accounting

Republicans eye $25K SALT cap as Trump’s tax cuts take shape

Republicans are in the process of drafting a tax bill behind closed doors that includes an increase of the state and local tax deduction to as high as $25,000 for an individual, according to people familiar with the plan.

A sizable increase to the current $10,000 limit on SALT write-offs would represent a major political victory for a crucial group of swing-district House Republicans representing the New York City area and southern California, who have made their votes for a broader tax cut bill contingent upon securing a bigger deduction.

The plan, which is still in the process of being drafted and is not final, also includes a renewal of President Donald Trump’s 2017 tax reductions for individuals and closely held businesses as well as some of his campaign tax pledges, the people said, requesting anonymity to discuss private matters.

Republicans are considering offsetting the increase to the SALT cap by reducing the deductions corporations can claim on the state and local taxes they pay, the people said.

The president has not yet been briefed on this proposal, but the draft represents progress on the top legislative agenda item for Republicans. The party is aiming to pass the legislation by August at the latest, as lawmakers rush to provide a counterweight to the potential economic damage and market downturn from the White House’s tariff policies.

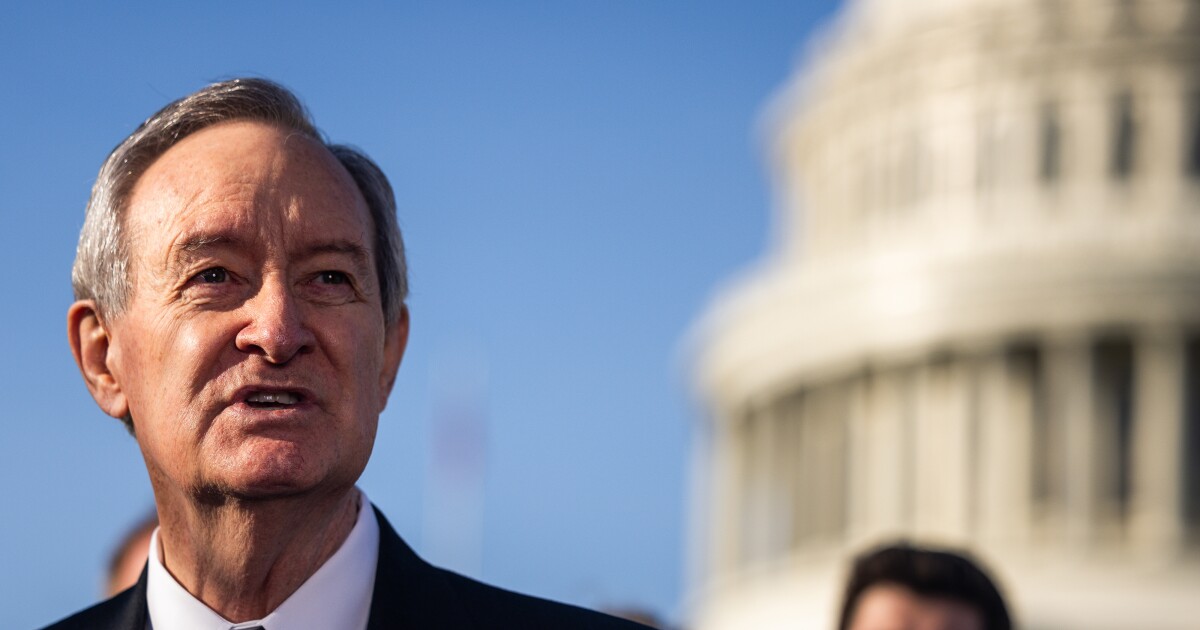

Trump administration aides and Senate Finance Chairman Mike Crapo’s team are taking the lead on writing the plan, the people said.

Crapo has cautioned that “until the bill is drafted, everything is on the table and nothing’s on the table.”

The White House and the Treasury Department did not immediately respond to requests for comment.

On the campaign trail, Trump promised to eliminate taxes on tipped income, overtime pay and Social Security benefits. The plan will aim to deliver on at least two of those pledges, according to the people familiar.

If Republicans end up including Trump’s Social Security idea, they’ll limit the tax breaks to only apply to incomes below a certain threshold, the people said. Senate rules also limit tax reductions related to payroll levies, so Republicans may need to develop a workaround for seniors that does not directly eliminate income taxes on benefit checks.

Trump’s no-taxes-on-tips idea is the most fleshed-out policy, the people said.

The Senate is still in the process of negotiating a resolution that will dictate the overall size of the tax cuts and any spending reductions in the final bill. Both chambers of Congress will need to pass identical versions of that measure before official negotiations on the tax cuts can begin.

Crapo’s staff and administration aides are compiling a draft of the tax bill now so that Republicans will largely be on the same page after Congress approves the budget resolution. The Senate plans to vote on the budget, which will also include an increase to the debt ceiling, in the coming days, with the House following next week.

The proposal will also roll back parts of the Inflation Reduction Act, signed by President Joe Biden, as a means to offset some of the cuts.

During the early days of the COVID-19 pandemic, the turbulence felt unprecedented. Fast forward to 2025, and turbulence is now the norm rather than the exception.

Whether it’s the impact of economic policies on

From entrepreneurs building a growing business to enterprise leaders charting a path forward, this constant turbulence does not offer ideal business conditions.

In this era of uncertainty, leaders can focus instead on building resilience in the one area they can control: internal operations.

Let’s explore why automated accounting controls are the unsung heroes of business resilience.

Business continuity is a must in 2025

Despite the ongoing wave of external challenges, the unfortunate reality for business leaders is that there is no pause button.

Whatever headline-grabbing turn occurs, companies must continue paying suppliers and employees, upgrading infrastructure and serving customers.

While this is true across all areas of operations, accounting controls stand out as an often-overlooked domain—straightforward to implement and highly impactful for improving business resilience and continuity.

For instance, the rise of gen AI has sparked excitement about saving time and money on marketing campaigns and revolutionizing reach on social media. However, this area is full of external variables, making true automation complex to achieve. Moreover, results rely heavily on continuous human input to ensure alignment with organizational priorities.

In contrast, accounting systems and processes are far more formulaic, making them ideal candidates for automation. A company can project critical dates years in advance—such as tax deadlines, supplier payment schedules, and invoice due dates.

These tasks also fall into the quadrant of being both urgent and important. Failing to submit a tax return or file an invoice can have serious negative consequences. That’s why automating this area of operations is a strategic move for business resilience.

Why manual accounting puts resilience at risk

In this era of uncertainty, agility and capital preservation are critical. Digital solutions are helping businesses manage accounting controls more efficiently, enabling stable and reliable access to capital while keeping the business solvent.

Yet data shows that accounting teams still rely on manual processes. To illustrate,

From a resilience standpoint, this introduces significant risk. Excel files can become corrupted or may store vital financial data on an individual employee’s desktop, making it difficult to track progress or ensure financial solvency.

It also increases the risk of missed tasks, such as sending invoices to suppliers—potentially delaying income. Automated accounting should form the backbone of a resilient business in 2025.

The contractual nature of B2B agreements may reduce the urgency for real-time settlements, but digitization is accelerating. Many suppliers may welcome faster settlement if it guarantees quicker access to capital.

Applying automation software reduces risk, ensures reliable access to capital, and allows companies to manage year-end reporting more efficiently. Modern accounting automation systems offer tools for repetitive tasks such as invoicing, bank reconciliation, data entry and tax calculations. These features save time, reduce human error, and increase the speed and accuracy of financial processes.

Put simply, automating your accounting controls yields an outsized impact on business resilience—making this area of operations one of the best in terms of ROI.

The strategic role of accounting and finance

Today’s finance leaders are more than number crunchers—they are strategic partners guiding the company through turbulent times. With uncertainty narrowing margins and challenging growth, the CFO holds critical oversight of the company’s financial health.

From this vantage point, CFOs can anticipate risks that may threaten undercapitalized businesses or those in vulnerable stages of growth. Strong accounting controls and digital tools ensure CFOs have access to accurate, real-time insights.

By embracing modern solutions, optimizing the office of the CFO, and investing in secure, trustworthy partnerships, businesses can better navigate the challenges of today’s economy.

A recent report from

This was one of the findings of

What’s more, the report said that simple tax compliance tasks will likely be next, as new solutions can, theoretically, reduce preparation time from hours to minutes— extracting, analyzing and completing returns with high accuracy, requiring minimal human intervention except for final review. Some firms, said the report, are reporting over 80% automation of individual return preparation.

Елена Бутусова – stock.adobe.com

This development has had several second effects, such as an increasing shift in focus from tax compliance to tax strategy for firms. With machines taking over more and more of tax prep and return processing, humans increasingly are concentrating on broader strategic consulting for tax clients.

“As automation is able to absorb increasingly more prep and review tasks, CPAs are reallocating time toward strategic tax planning, scenario modeling and client coaching. Firms are upskilling staff to interpret AI output and provide deeper guidance,” said the report.

The rising automation of tax return prep has also shifted hiring priorities. The report noted that “AI fluency” is now commonly required for even entry-level positions, and that firms are developing “AIready associate” programs that combine technical accounting training with AI tools mastery. They’re also partnering with schools to create specialized pre-employment certifications that validate both domain knowledge and technological competency.

Once they are hired, early career professionals are also focusing less on the execution of routine tasks as their predecessors were. Whereas before a firm might have a small army of entry-level associates to fill out 1099s assembly line style, today’s early career professionals focus more on developing “AI oversight” capabilities. Similarly, they’re increasingly being evaluated not on task completion to value-added analysis, client communication and effective AI collaboration.

This, in turn, will be part of a broader anticipated shift in a firm’s strategic priorities. The focus today on automating tasks, the report said, will lead to comprehensive systems that coordinate across the entire accounting workflow, with the emphasis being not on task execution (that’s what the machine is for) but “ecosystem orchestration.” The idea is that the solutions within the firm’s ecosystem will manage the interplay between client data, regulatory requirements and team capabilities, optimizing resource allocation and process design in real time.

Under such conditions, annual, quarterly and monthly cadences the profession is accustomed to will give way to a world of continuous operations that adjust instantly to new information. Workflows will reconfigure themselves based on changing priorities, emerging risks and resource availability, ideally creating responsive practices that scale efficiency without sacrificing quality.

Audit and advisory a little slower

While bookkeeping tasks can now be completely automated, and tax compliance not far behind, the report said progress was a little slower on automating audit and risk analysis tasks, describing its status as “slow but strategic adoption.” New tools are making inroads, helping firms focus on higher conceptual matters that require their professional judgment, but due to regulatory and liability complexity, innovation in this area is more methodical.

Meanwhile, AI in advisory is considered “the next frontier.” The report noted the emergence of things like AI-driven forecasting, budgeting and KPI modeling tools, and that firms are blending human intuition with AI-generated what-if scenarios to deepen value-based client conversations. The blending of machine insight with human expertise will likely continue, with the binary choice between automation and human judgment eventually dissolving into fluid partnerships where AI handles routine analysis while elevating professionals’ capacity for strategic thinking.

Our

ROI still elusive

The report said that, as of the first quarter of 2025, it is still too early for most firms to quantify the full return on investment (ROI) from their AI initiatives. While firms are reporting clear productivity gains, the specific financial impact is still developing. Regardless of whether or not the gains can be quantified in revenue terms, the report said that firms that have embraced AI are beginning to see meaningful operational gains, including up to 70% reduction in time spent on manual tasks, five times faster review cycles for tax prep and audits, and a two to three times increase in client capacity without additional headcount.

Top 50 Firm Elliott Davis announced today it is taking a private equity investment from Flexpoint Ford to accelerate the firm’s growth and expand its service offerings and geographic reach.

The firm also announced it selected John Otten as its next CEO, effective July 1. Otten succeeds Rick Davis, who held the role for over 18 years and will stay at the firm in an advisory role.

Picasa

“The future is bright with John at the helm,” Davis said in a statement. “He has long been a trusted advisor to our clients and a respected leader within our firm. John lives our values, embraces our mission, and is fully prepared to guide Elliott Davis into its next chapter.”

As is common among many accounting firms taking PE capital, Elliott Davis will operate in an alternative practice structure. Elliott Davis, a licensed CPA firm, will continue to provide attest services. Elliott Davis Advisory, will operate as a separate entity and provide business advisory and non-attest services.

(Read more:

“This marks an important milestone for Elliott Davis,” Otten said in a statement. “We are making significant investments in people, technology and services to meet the evolving needs of our clients and ensure we remain a destination employer. Our partnership with Flexpoint Ford positions us well for continued expansion through both organic growth as well as through strategic acquisitions.”

“Elliott Davis stands out for its client-first approach and one firm culture — hallmarks of an exceptional professional services platform,” Flexpoint Ford’s managing director Dominic Hood said in a statement. “We are excited to partner with John and the broader leadership team as they build on the firm’s legacy and drive its next phase of growth.”

Flexpoint Ford principal Jennifer Kim added, “We look forward to supporting Elliott Davis’s expansion through the continued recruitment and development of exceptional talent, alongside a disciplined and strategic M&A strategy designed to enhance capabilities and extend market reach.”

Guggenheim Securities, LLC and Koltin Consulting Group advised Elliott Davis, and Nelson Mullins Riley & Scarborough LLP and Vedder Price P.C. served as its legal counsel. William Blair & Company, LLC advised Flexpoint Ford, and Simpson Thacher & Bartlett LLP and Hunton Andrews Kurth LLP served as its legal counsel.

U.S. budget deficit hit $316 billion in May, with annual shortfall up 14% from a year ago

Donald Trump can call in the troops

Social Security cost-of-living adjustment may be 2.5% in 2026: estimates

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Personal Finance1 week ago

Personal Finance1 week agoWhat the national debt, deficit mean for your money

-

Economics1 week ago

Economics1 week agoPeople cooking at home at highest level since Covid, Campbell’s says

-

Economics5 days ago

Economics5 days agoJobs report May 2025:

-

Economics1 week ago

Economics1 week agoElon Musk’s failure in government

-

Economics5 days ago

Economics5 days agoDonald Trump has many ways to hurt Elon Musk

-

Economics5 days ago

Donald Trump has many ways to hurt Elon Musk

-

Economics3 days ago

Economics3 days agoSending the National Guard to LA is not about stopping rioting

-

Finance5 days ago

Finance5 days agoStocks making the biggest moves midday: WOOF, TSLA, CRCL, LULU