Accounting

Tax Strategy: A syndicated conservation easement update

The long efforts to put in place the enforcement mechanisms to attack syndicated conservation easements appear to at last be finalized. In October 2024, the Internal Revenue Service issued final regulations targeting syndicated conservation easements. The agency first started identifying claims for substantial conservation easement deductions by investors in syndicated partnerships back in 2016, and issued Notice 2017-10 identifying syndicated conservation easements as abusive and requiring reporting by participants. It also sought help from Congress to specifically disallow the abusive aspects of the transactions.

The syndicated conservation easement industry fought back. The industry won a court case on the basis that the notice issued by the IRS failed to meet Administrative Procedure Act requirements for notice and opportunity for comments. Lobbying efforts stymied the progress of congressional action and included efforts to strip the IRS of enforcement funds. Initial efforts to get taxpayers to accept settlement offers were frustrated by funds available for the defense of the transactions built into the deal structures.

The IRS has challenged $21 billion in deductions claimed by 28,000 syndicated conservation easement investors. Even the Land Trust Alliance, which administers traditional conservation easements, became concerned that the syndicated conservation easement activity would result in the complete loss of the conservation easement deduction. The IRS estimated that the number of syndicated conservation easement deductions grew from 249 deals in 2016, generating $6 billion in charitable deductions, to 296 deals in 2018 producing $9.2 billion in deductions. Traditional conservation easement deductions have resulted in around $1 billion in annual deductions.

Statutory action

After several years of frustration in getting Congress to address syndicated conservation easements, success was achieved with the enactment of Code Sec. 170(h)(7) in 2022. Code Sec 170(h)(7) provides that a contribution by a partnership is not treated as a qualified conservation contribution if the amount of such contribution exceeds 2.5 times the sum of each partner’s interest in the partnership. Exceptions are provided for three-year holding periods, contributions made by family pass-through entities, and contributions made to preserve a certified historic building. Reporting requirements apply to partnerships, S corporations, and other pass-through entities. The statute does not apply retroactively, but only to contributions made after Dec. 29, 2022.

Final regulations

In order to overcome the APA challenges to the syndicated conservation easement notice, the IRS began a process of issuing proposed regulations to meet APA requirements. In November 2022 the IRS issued proposed regulations that disallowed deduction for syndicated conservation easement transactions made by a partnership or an S corporation after Dec. 29, 2022, if the amount of the contribution exceeds 2.5 times the sum of each partner’s or S corporation shareholder’s relevant basis. The regulations also imposed new reporting requirements for the members of the entity who are seeking a deduction based on the transaction — IRS Form 8886, “Reportable Transaction Disclosure Statement.”

The final regulations were issued on Oct. 7, 2024, and are effective Oct. 8, 2024. They address three specified classes of abusive syndicated conservation easement transactions and substantially similar transactions:

1. Transactions involving contributions occurring before Dec. 30, 2022;

2. Transactions for which a charitable contribution deduction is not automatically disallowed by Code Sec. 170(h)(7); and,

3. Transactions that substitute the contribution of a fee simple interest in real property for the contribution of a conservation easement.

The final regulations generally adopt the 2022 proposed regulations with clarifications of the meanings of the terms “substantially similar transactions,” the 2.5 times rule, “conservation easement,” and “participant.” The final regulations also clarify that participants and material advisors must report syndicated conservation easement transactions to the IRS that were completed in tax years that are still open. It is possible that taxpayers could be subject to both the requirements of Code Sec. 170(h)(7) and the final regulations.

Lam Yik/Bloomberg

Settlement offers

The IRS initiated its third settlement offer to try to dispose of many of the audits before it in June 2024. The earlier settlement offers had only limited success. However, the final regulations and growing success in the courts may push more syndicated deals into settlement. Only taxpayers who receive a settlement offer letter from the IRS are eligible for the settlement offer. The settlement offers have typically involved agreeing that the deduction for the contribution be disallowed in full; all partners must agree to settle; the partnership must pay the full amount of tax penalties and interest before settlement; partners can deduct the cost of acquiring partnership interests; and penalties can range from 10% to 20% for investor partners and up to 40% for partners active in the transaction. The settlement offers require the cooperation of partners during the resolution of the issue.

It may be difficult for some partnerships to get the consent of all partners in a deal to participate in the settlement and to be willing to cooperate in the resolution.

Criminal and civil enforcement

With Code Sec. 170(h)(7) in place, as well as now the final regulations, the Tax Court has set aside APA concerns and started to deny overvaluation of conservation easements. For example, in Mill Road 36 Henry LLC v. Commissioner, U.S.T.C. Oct. 26, 2023, the court limited the LLC’s deduction to its tax basis and added an accuracy-related penalty. A circuit court case has also rejected the claimed deductions.

Some of the key promoters of syndicated conservation easements, as well as one of the appraisers utilized by the promoters, have been convicted of fraud and falsification of documents and some have already received substantial prison sentences.

Summary

The tools now seem to be in place to curtail the syndicated conservation easement industry. There remains a lot of work for the IRS to resolve all of the transactions still under audit. It remains to be seen how helpful settlement offers will be in disposing of some of these audits.

As CPA firms grow into the $10 million to $100 million revenue range, operational complexity increases, especially during peak periods like tax season. Leadership must prioritize strategies to reduce friction, improve efficiency, and enhance the client and staff experience. Algorithms, defined as systematic processes designed to solve specific problems, are a key enabler in achieving these goals.

By automating repetitive tasks, algorithms can save hundreds of hours during the busiest times, allowing staff to focus on high-value activities and improving client satisfaction.

Four specific examples of areas where algorithms can help firms are described below, but no matter the area, adopting algorithms requires deliberate planning and execution:

1. Identify opportunities

- Assess pain points in tax, audit, scheduling, and advisory workflows.

- Identify routine tasks that consume excessive time during peak periods.

2. Gather and analyze data

- Evaluate the availability of client and internal data to support automation.

- Determine additional data needs and acquisition strategies.

3. Experiment and iterate:

- Pilot small-scale solutions, such as automating a single tax form process or scheduling tool.

- Refine based on results and user feedback.

4. Scale and integrate:

- Implement successful pilots across teams or departments.

- Provide staff training to maximize adoption and effectiveness.

5. Measure and optimize:

- Use key performance indicators such as time savings, error reduction, and client satisfaction to assess the impact.

Quick wins for immediate impact

To build momentum, start with high-impact initiatives:

- Tax workflow automation: Automate the completion, e-signature, and filing of forms like 8879 and 4868, and notify clients of estimated tax payments due via an automated communication system.

- Audit data preparation: Use algorithms to download client data, generate trial balances, and perform risk analysis.

- Scheduling optimization: Implement an algorithm-driven scheduling tool to automate meeting coordination, resource allocation, and deadline tracking.

Conclusion

Algorithms are transformative tools that empower CPA firms to operate more efficiently while delivering enhanced value. By automating routine tasks in tax, audit, scheduling, and advisory services, firms can save significant time, improve accuracy, and foster stronger client relationships. The key to success lies in adopting a strategic roadmap — identifying opportunities, running experiments, and scaling solutions. Mindset is paramount.

For CPA firms navigating the challenges of growth and complexity, algorithms represent a critical investment in operational excellence, enabling staff to focus on what truly matters: delivering exceptional client experiences. Think — plan — grow!

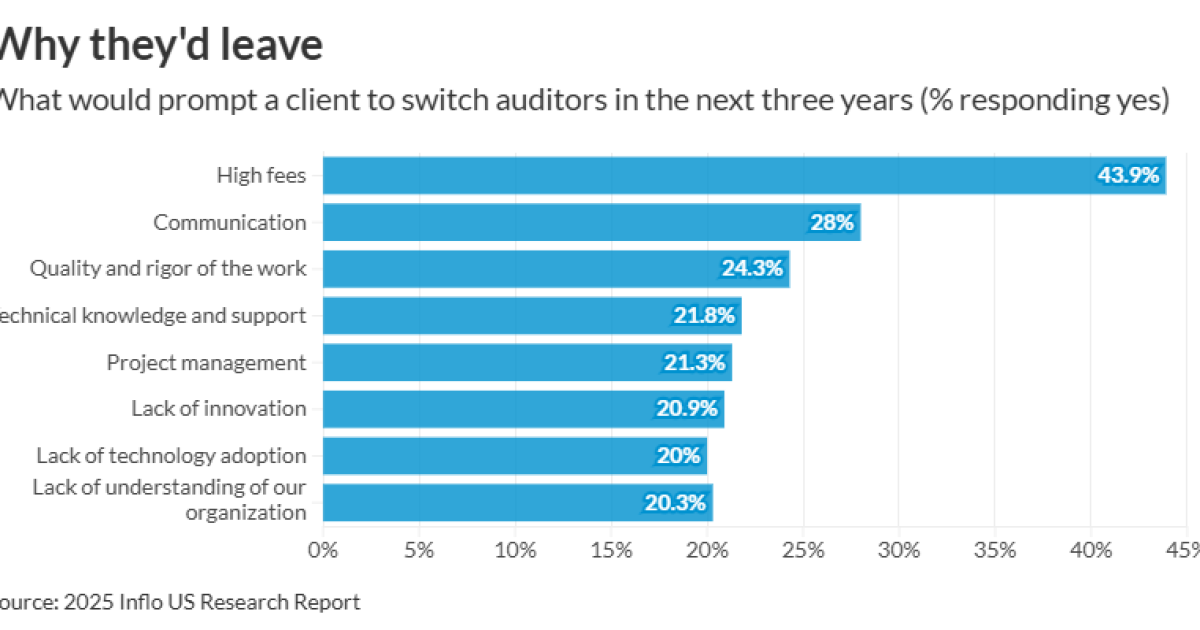

More than two-thirds (70%) of U.S. audit clients are ready to change firms within the next three years, according to a new report.

Inflo’s “Creating a New Audit Experience for U.S. Businesses”

Clients with the most employees (250 employees or more) were the highest to report it was “very likely” they would switch firms. Meanwhile, clients with fewer employees (less than 50 employees) were the highest to report it was “very unlikely” they’d switch firms.

By far the most common reason causing a client to look for a new firm was high fees (44%). When asked how much more clients would be willing to pay for an audit that “gave you more value,” respondents answered 5-10% more (33%), 11-20% (31%) and 21-30% (14%). Five percent of respondents answered “nothing.”

Subsequently, clients said the leading factors influencing their decision to accept or resist fee increases were perceived value and quality of service (42%), relationship with the audit firm (40%), meeting deadlines (39%), level of justifications and transparency regarding an increasing (35%), responsive communication (35%) and the frequency of previous fee increases (34%).

(Read more:

The second most common reason causing a client to switch auditors was communication (28%), followed by quality and rigor of the work (24%), technical knowledge and support (22%), project management (21%), lack of innovation (21%) and lack of technology adoption (20%). Sixteen percent of respondents reported, “We are not experiencing any issues.”

“This research makes one thing clear: U.S. businesses are demanding a better audit experience,” Inflo CEO Mark Edmondson said in a statement. “From high fees based on outdated pricing models to technology that hasn’t changed since the 1990s, the approach of many audit firms is driving business away.”

Additionally, nearly half of respondents (45%) said they’d like auditors to improve on the use of technology to add more value to their audits, followed by the time needed from their team and insights on their organization (38% each).

“The good news is that clients care about their audits. They want them to play a key role in driving operational improvement and consistent business growth,” Edmondson said. “Audit firms that act on the report’s findings will be rewarded with rising fee incomes and a continually growing client base.”

Boomer’s Blueprint: 4 ways algorithms can improve your accounting firm

Two-thirds of clients ready to change auditors

Student loan borrower in SAVE forbearance says interest growing

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Blog Post1 week ago

Blog Post1 week agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics1 week ago

Economics1 week agoWhy the president must not be lexicographer-in-chief

-

Finance1 week ago

Finance1 week agoThis is why Jamie Dimon is so gloomy on the economy

-

Accounting1 week ago

Accounting1 week agoSteinhoff fraud trial moved to South Africa’s high court

-

Personal Finance7 days ago

Personal Finance7 days agoWhat the national debt, deficit mean for your money

-

Personal Finance1 week ago

Personal Finance1 week agoHow to save on summer travel in 2025

-

Personal Finance1 week ago

Personal Finance1 week agoDenmark raises retirement age to 70; U.S. might follow

-

Finance1 week ago

Finance1 week agoWhy JPMorgan hired NOAA’s Sarah Kapnick as chief climate scientist