Personal Finance

There’s still time to meet the IRA contribution deadline for 2023

Damircudic | E+ | Getty Images

The tax deadline is approaching and there’s still time to score a deduction with a pretax individual retirement account contribution — if you qualify.

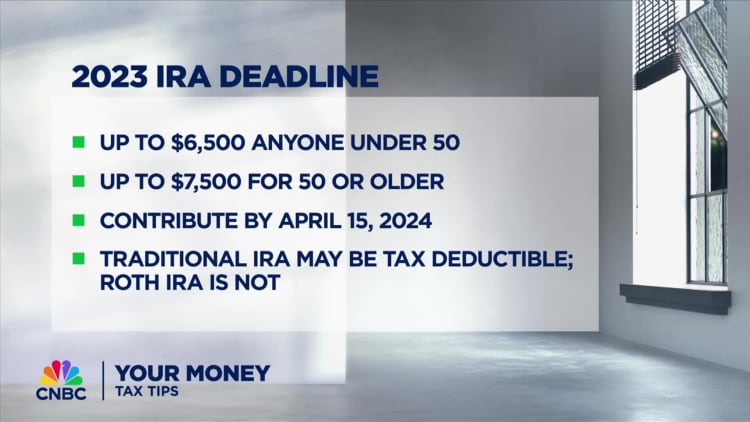

For 2023, the IRA contribution limit was $6,500, plus an extra $1,000 for investors age 50 and older. That increased to $7,000 for 2024, with $1,000 more for catch-up contributions.

You can still add money to your IRA for 2023 before the federal tax deadline, which is April 15 for most taxpayers. But you must designate the deposit for tax year 2023.

More from Personal Finance:

There’s still time to reduce your tax bill or boost your refund before the deadline

An ‘often overlooked’ retirement savings option can lower your tax bill

Some retirement savers can still get a ‘special tax credit,’ IRS says

A last minute pretax IRA contribution for 2023 could qualify for an “above-the-line” deduction, which you can claim even if you don’t itemize tax breaks, and it reduces your adjusted gross income.

However, the IRA deductibility rules can be “very confusing,” according to Mark Steber, chief tax information officer at Jackson Hewitt.

Your eligibility for a pretax IRA deduction depends on three factors: your filing status, modified adjusted gross income and your workplace retirement plan.

Here’s who qualifies for the IRA deduction

If you don’t have a workplace retirement plan, there’s no income limit for IRA deductions, which could be appealing for higher earners, experts say.

But it’s more complicated if you participate in a workplace retirement plan. “Participation” could include employee contributions, company matches, profit-sharing or other employer deposits.

“It’s important to understand there are deductibility limitations,” certified financial planner Malcolm Ethridge, executive vice president of CIC Wealth in Rockville, Maryland, recently told CNBC.

You could deduct all, part, or none of your pretax IRA contributions, depending on your filing status and income. The complete IRS eligibility chart is available here.

For 2023, there’s a full deduction for single filers with a modified adjusted gross income of $73,000 or less, and a partial deduction up to $83,000.

The limits are higher for married couples filing together, with a full deduction at $116,000 or less, and a partial deduction before reaching $136,000.

“Even if you maxed out the plan at your current company, your income could still be low enough to make a tax-deductible [IRA] contribution,” Ethridge said.

Consider your investing goals first

While scoring a last minute deduction with a pretax contribution may be tempting, you need to consider your goals and timeline before proceeding, experts say.

The contribution could offer a benefit this year, only to create a future “tax problem,” said CFP Laura Mattia, CEO of Atlas Fiduciary Financial in Sarasota, Florida.

Plus, you need to weigh your immediate priorities, including major expenses, because “you don’t want to use a retirement vehicle for shorter-term savings,” she said.

Nitat Termmee | Moment | Getty Images

The U.S. job market isn’t looking too hot for recent college graduates and other job seekers, according to economists and labor experts.

“The job market is kind of trash right now,” said Mandi Woodruff-Santos, a career coach and personal finance expert.

“I mean, it’s really difficult,” she added. “It’s really difficult for people who have many years of experience, so it’s going to be difficult for college kids.”

‘Tough summer’ for job seekers

That may seem counterintuitive.

The national unemployment rate in May was relatively low, at 4.2%. The layoff rate has also been historically low, suggesting employers are holding on to their workers.

Yet, hiring has been anemic. The pace of employer hiring in April was the lowest in more than 10 years, since August 2014, excluding the early months of the Covid pandemic.

More from Personal Finance:

Millions would lose health insurance under GOP megabill

Average 401(k) balances drop 3% due to market volatility

Trump administration asks Supreme Court to lift ban on Education Department layoffs

The rate at which workers are quitting — a barometer of worker confidence about their job prospects — has also plummeted to below pre-pandemic levels, a stark reversal from the “great resignation” in 2021 and 2022.

“It will be a tough summer for anyone looking for full-time work,” Heather Long, chief economist at Navy Federal Credit Union, wrote in an e-mail Friday.

“This is an ‘abundance of caution economy’ where businesses are only filling critical positions and job seekers, especially recent graduates, are struggling to find employment,” she said.

Steady job market erosion ‘cannot continue forever’

While the job market may be limping along by some measures, Long also said a recession doesn’t seem “imminent.”

Businesses added more jobs than expected in May, for example. But those gains have slowed significantly — a worrisome sign, economists said.

Employers appear reluctant to hire in an uncertain economy.

CEO confidence plummeted in the second quarter of 2025, seeing its largest quarterly decline on record dating to 1976, according to a survey by The Conference Board. Uncertainty around geopolitical instability, trade and tariff policy were the largest business risks, according to Roger Ferguson Jr., the group’s chair emeritus.

The share of CEOs expecting to expand their workforce fell slightly, to 28% in Q2 from 32% in Q1, and the share planning to cut their workforce rose 1 point, to 28%.

“The steady erosion in the US job market cannot continue forever — at some point, there will just not be much left to give,” Cory Stahle, an economist at the Indeed Hiring Lab, wrote in an analysis Friday.

“In a low-hiring, slow-growth environment, employers can only hold onto their existing employees for so long before they too will have to be let go — increasing unemployment even as job opportunities continue to shrink,” Stahle wrote.

Don’t underestimate personal connections

Don’t underestimate the “power of personal connections” to help get noticed in a competitive job market like this one, said Woodruff-Santos, the career coach.

Her No. 1 piece of advice: Make yourself “uncomfortable” in order to network and build professional relationships.

“You need to put yourself in situations where you may not know everybody, you may not know one person, where you may actually need someone to give you a bit of a helping hand, and to feel confident and OK doing that,” Woodruff-Santos said.

If you’re pushed to accept a job you don’t love to make ends meet, make a plan to keep current in the field to which you aspire, she said.

In other words, build the skills that will eventually help you get that job, perhaps by taking a training course, getting a certificate or doing contract work, she said. Also, consider joining a professional organization, putting yourself in the same room as people in your desired field and with whom you can connect, she said.

These steps raise your chances of getting attention from future employers and keeping your skills sharp, Woodruff-Santos said.

She also had some words of encouragement.

“The job market has been trash before,” she said. “It’ll be trash again. This probably won’t be your first trash job market. And you’re going to be OK.”

WASHINGTON DC, UNITED STATES – MAY 30: United States President Donald Trump departs at the White House to U.S. Steel’s Irvin Works in West Mifflin, Pennsylvania in Washington D.C May 30, 2025.

Celal Gunes | Anadolu | Getty Images

As the Senate weighs President Donald Trump‘s multi-trillion-dollar spending package, a lesser-known provision tucked into the House-approved bill has pushback from Wall Street.

The House measure, known as Section 899, would allow the U.S. to add a new tax of up to 20% on foreigners with U.S. investments, including multinational companies operating in the U.S.

Some analysts call the provision a “revenge tax” due to its wording. It would apply to foreign entities if their home country imposes “unfair foreign taxes” against U.S. companies, according to the bill.

“Wall Street investors are shocked by [Section] 899 and apparently did not see it coming,” James Lucier, Capital Alpha Partners managing director, wrote in a June 5 analysis.

More from Personal Finance:

The average 401(k) savings rate hit a record high. See if you’re on track

On-time debt payments aren’t a magic fix for your credit score. Here’s why

With ‘above normal’ hurricane forecasts, check your home insurance policy

If enacted as written, the provision could have “significant implications for the asset management industry,” including cross-border income earned by hedge funds, private equity funds and other entities, Ernst & Young wrote on June 2.

Passive investment income could be subject to a higher U.S. withholding tax, as high as 50% in some cases, the company noted. Some analysts worry that could impact future investment.

The Investment Company Institute, which represents the asset management industry serving individual investors, warned in a May 30 statement that the provision is “written in a manner that could limit foreign investment to the U.S.”

But with details pending as the Senate assesses the bill, many experts are still weighing the potential impact — including who could be affected.

Here’s what investors need to know about Section 899.

How the ‘revenge tax’ could work

As drafted, Section 899 would allow the U.S. to hike existing levies for countries with “unfair foreign taxes” by 5% per year, capped at 20%.

Several kinds of tax fall under “unfair foreign taxes,” according to the provision. Those include the undertaxed profits rule, which is associated with part of the global minimum tax negotiated by the Biden administration. The term would also apply to digital services taxes and diverted profits taxes, along with new levies that could arise, according to the bill.

The second part of the measure would expand the so-called base erosion and anti-abuse tax, or BEAT, which aims to prevent corporations from shifting profits abroad to avoid taxes.

“Basically, all businesses that are operating in the U.S. from a foreign headquarters will face that,” said Daniel Bunn, president and CEO of the Tax Foundation. “It’s pretty expansive.”

The retaliatory measures would apply to most wealthy countries from which the U.S. receives direct foreign investment, which could threaten or harm the U.S. economy, according to Bunn’s analysis.

Notably, the proposed taxes don’t apply to U.S. Treasuries or portfolio interest, according to the bill.

‘Strong priority’ for House Republicans

Section 899 still needs Senate approval, and it’s unclear how the provision could change amid alarm from Wall Street.

But the measure has “strong support” from others in the business community, and it’s a “strong priority” for Republican House Ways and Means Committee members, Capital Alpha Partners’ Lucier wrote.

House Ways and Means Committee Chairman Jason Smith, R-Mo., first floated the idea in a May 2023 bill, and has been outspoken, along with other Republicans, against the global minimum tax.

If enacted as drafted, Section 899 could raise an estimated $116 billion over 10 years, according to the Joint Committee on Taxation.

That could help fund other priorities in Trump’s mega-bill, and if removed, lawmakers may need to find the revenue elsewhere, Bunn said.

However, House Ways and Means Republicans may ultimately want foreign countries to adjust their tax policies before the new tax is imposed.

“If these countries withdraw these taxes and decide to behave, we will have achieved our goal,” Smith said in a June 4 statement.

Warner Bros. Discovery, Tesla, Robinhood, IonQ and more

Robinhood shares drop after the online brokerage fails to get the nod to join the S&P 500

Job market is ‘trash’ right now, career coach says — here’s why

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Blog Post1 week ago

Blog Post1 week agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics1 week ago

Economics1 week agoWhy the president must not be lexicographer-in-chief

-

Finance1 week ago

Finance1 week agoThis is why Jamie Dimon is so gloomy on the economy

-

Personal Finance1 week ago

Personal Finance1 week agoU.S. birth rate drop outpaces policy response, raising future concerns

-

Accounting1 week ago

Accounting1 week agoSteinhoff fraud trial moved to South Africa’s high court

-

Personal Finance7 days ago

Personal Finance7 days agoWhat the national debt, deficit mean for your money

-

Personal Finance1 week ago

Personal Finance1 week agoHow to save on summer travel in 2025

-

Personal Finance1 week ago

Personal Finance1 week agoDenmark raises retirement age to 70; U.S. might follow