Finance

This week’s personal loan rates rise for 3- and 5-year terms

Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as “Credible” below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

The latest trends in interest rates for personal loans from the Credible marketplace, updated weekly. (iStock)

Borrowers with good credit seeking personal loans during the past seven days prequalified for rates that were higher for 3- and 5-year loans when compared to fixed-rate loans for the seven days before.

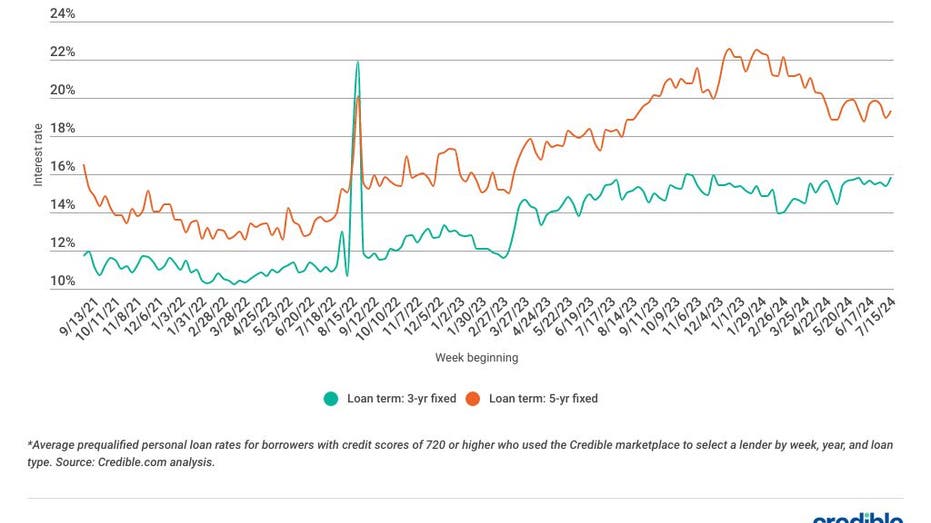

For borrowers with credit scores of 720 or higher who used the Credible marketplace to select a lender between July 18 and July 24:

- Rates on 3-year fixed-rate loans averaged 15.97%, up from 15.36% the seven days before and from 15.45% a year ago.

- Rates on 5-year fixed-rate loans averaged 19.88%, up from 19.02% the previous seven days and from 18.62% a year ago.

Personal loans have become a popular way to consolidate debt and pay off credit card debt and other loans. They can also be used to cover unexpected and emergency expenses like medical bills, take care of a major purchase, or fund home improvement projects.

Average personal loan interest rates

Average personal loan interest rates have increased over the last seven days for 3- and 5-year loans. While 3-year loan rates rose by 0.61 percentage points, rates on 5-year loans spiked by 0.86 percentage points. Interest rates for 3- and 5-year terms remain higher than they were this time last year, up 0.52 percentage points for 3-year terms and up 1.26 percentage points for 5-year terms.

Still, borrowers can take advantage of interest savings with a 3- or 5-year personal loan, as both loan terms offer lower interest rates on average than higher-cost borrowing options such as credit cards.

But whether a personal loan is right for you depends on multiple factors, including what rate you can qualify for, which is largely based on your credit score. Comparing multiple lenders and their rates helps ensure you get the best personal loan for your needs.

Before applying for a personal loan, use a personal loan marketplace like Credible to comparison shop.

Personal loan weekly rate trends

Here are the latest trends in personal loan interest rates from the Credible marketplace, updated weekly.

The chart above shows average prequalified rates for borrowers with credit scores of 720 or higher who used the Credible marketplace to select a lender.

For the month of June 2024:

- Rates on 3-year personal loans averaged 23.02%, up from 22.35% in May.

- Rates on 5-year personal loans averaged 24.81%, up from 24.52% in May.

Rates on personal loans vary considerably by credit score and loan term. If you’re curious about what kind of personal loan rates you may qualify for, you can use an online tool like Credible to compare options from different private lenders.

All Credible marketplace lenders offer fixed-rate loans at competitive rates. Because lenders use different methods to evaluate borrowers, it’s a good idea to request personal loan rates from multiple lenders so you can compare your options.

Current personal loan rates by credit score

In June, the average prequalified rate selected by borrowers was:

- 13.18% for borrowers with credit scores of 780 or above choosing a 3-year loan

- 32.55% for borrowers with credit scores below 600 choosing a 5-year loan

Depending on factors such as your credit score, which type of personal loan you’re seeking and the loan repayment term, the interest rate can differ.

As shown in the chart above, a good credit score can mean a lower interest rate, and rates tend to be higher on loans with fixed interest rates and longer repayment terms.

Where are interest rates headed?

The Bureau of Labor Statistics (BLS) reported that inflation slowed in May, raising hopes for multiple interest rate cuts in 2024. When the Fed concluded its June meeting, it signaled one cut by the end of the year while holding rates steady. As of now, we anticipate one 25 basis point (0.25 percentage points) cut this year, and a 100 basis point (1 percentage point) cut in 2025.

Currently sitting at 5.25% to 5.50%, the federal funds rate is the highest it’s been since 2001. Sticky inflation and low unemployment had made any cuts seem unlikely as of a week ago. But the news may deliver relief for borrowers burdened with high interest costs and those considering a loan. However, demand for personal loans has increased and all signs point to this trend continuing, while debt levels and delinquency rates have risen as well. This may indicate more consumers will struggle to be approved at low rates or at all — even if we see rates fall.

How to get a lower interest rate

Many factors influence the interest rate a lender might offer you on a personal loan. But you can take some steps to boost your chances of getting a lower interest rate. Here are some tactics to try.

Increase credit score

Generally, people with higher credit scores qualify for lower interest rates. Steps that can help you improve your credit score over time include:

- Pay bills on time: Payment history is the most important factor in your credit score. Pay all your bills on time for the amount due.

- Check your credit report: Look at your credit report to ensure there are no errors on it. If you find errors, dispute them with the credit bureau.

- Lower your credit utilization ratio: Paying down credit card debt can improve this important credit-scoring factor.

- Avoid opening new credit accounts: Only apply for and open credit accounts you actually need. Too many hard inquiries on your credit report in a short amount of time could lower your credit score.

Choose a shorter loan term

Personal loan repayment terms can vary from one to several years. Generally, shorter terms come with lower interest rates, since the lender’s money is at risk for a shorter period of time.

If your financial situation allows, applying for a shorter term could help you score a lower interest rate. Keep in mind the shorter term doesn’t just benefit the lender – by choosing a shorter repayment term, you’ll pay less interest over the life of the loan.

Get a cosigner

You may be familiar with the concept of a cosigner if you have student loans. If your credit isn’t good enough to qualify for the best personal loan interest rates, finding a cosigner with good credit could help you secure a lower interest rate.

Just remember, if you default on the loan, your cosigner will be on the hook to repay it. And cosigning for a loan could also affect their credit score.

Compare rates from different lenders

Before applying for a personal loan, it’s a good idea to shop around and compare offers from several different lenders to get the lowest rates. Online lenders typically offer the most competitive rates – and can be quicker to disburse your loan than a brick-and-mortar establishment.

But don’t worry, comparing rates and terms doesn’t have to be a time-consuming process.

Credible makes it easy. Just enter how much you want to borrow and you’ll be able to compare multiple lenders to choose the one that makes the most sense for you.

About Credible

Credible is a multi-lender marketplace that empowers consumers to discover financial products that are the best fit for their unique circumstances. Credible’s integrations with leading lenders and credit bureaus allow consumers to quickly compare accurate, personalized loan options – without putting their personal information at risk or affecting their credit score. The Credible marketplace provides an unrivaled customer experience, as reflected by over 7,500 positive Trustpilot reviews and a TrustScore of 4.8/5.

XcelLabs launches to help accountants use AI

Accounting is changing, and the world can’t wait until 2026

Republicans push Musk aside as Trump tax bill barrels forward

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Blog Post6 days ago

Blog Post6 days agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics1 week ago

Economics1 week agoElon Musk says Trump’s spending bill undermines the work DOGE has been doing

-

Accounting1 week ago

Accounting1 week agoHighest paid jobs in corporate accounting

-

Economics1 week ago

Economics1 week agoWhy the president must not be lexicographer-in-chief

-

Personal Finance1 week ago

Personal Finance1 week agoHarvard, Trump international enrollment battle affects college applicants

-

Personal Finance1 week ago

Personal Finance1 week agoCrypto in 401(k) plans: Trump administration eases rules

-

Accounting1 week ago

Accounting1 week agoTrump to pardon stars of reality show ‘Chrisley Knows Best’

-

Finance1 week ago

Finance1 week agoVail Resorts, GameStop and more