Accounting

WNBA standoff pits players who want more pay vs. ex Deloitte CEO

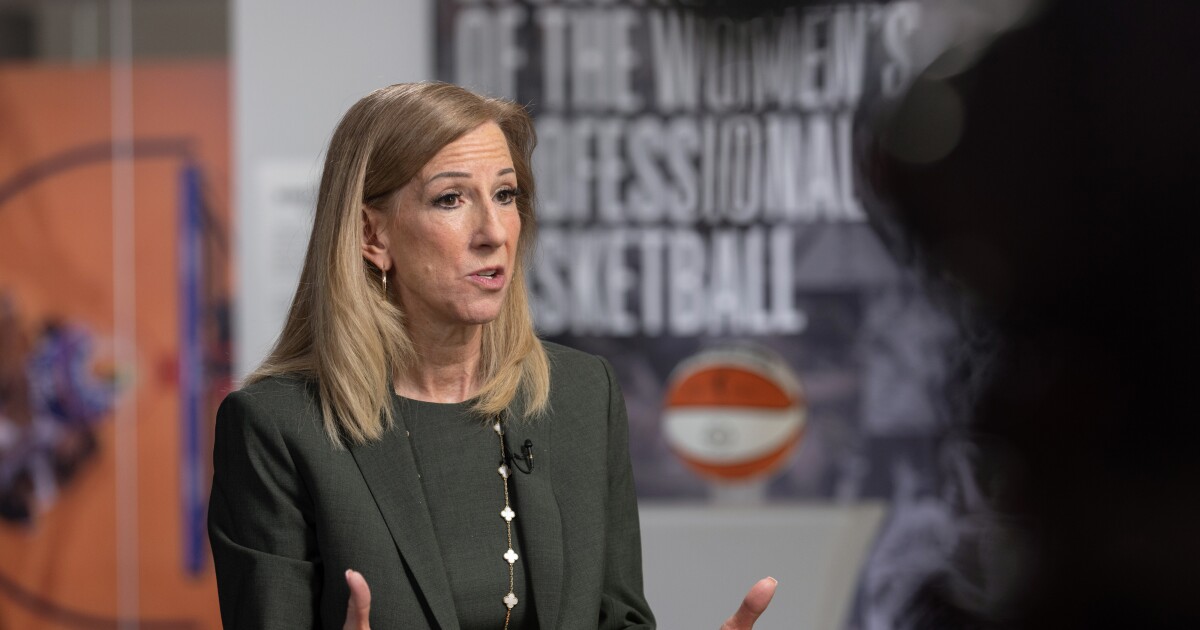

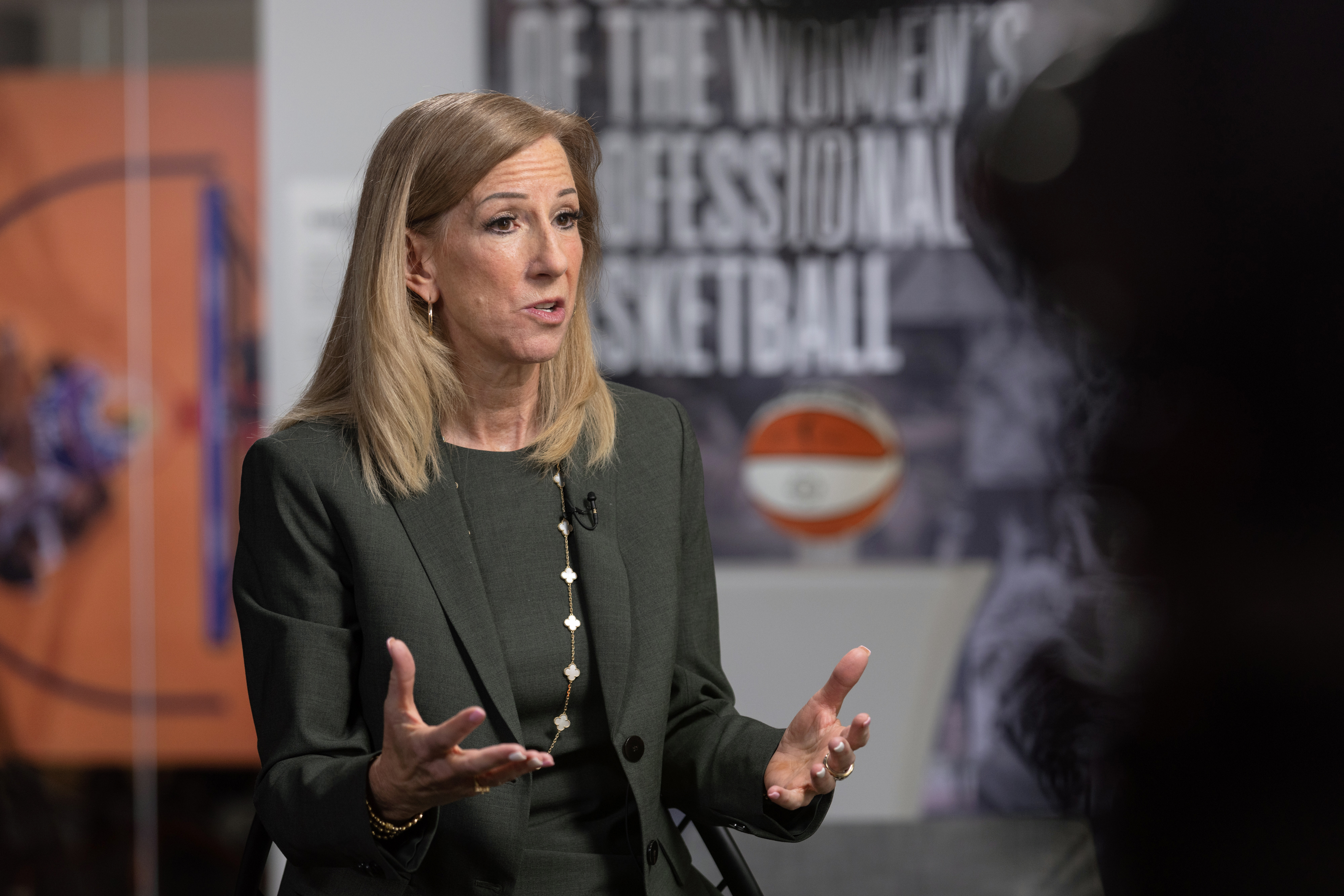

As WNBA Commissioner, Cathy Engelbert has transformed women’s basketball into a business juggernaut — but a standoff over how much players should share in the league’s growth could threaten her leadership, and her legacy.

Engelbert, a 60-year-old former chief executive officer of the accounting giant Deloitte who took the once-struggling league’s top job in 2019, has been widely credited with steering the pro basketball league through the tumult of the COVID-19 pandemic and into a prosperous new era.

Thanks in part to a surge in interest

Engelbert and the WNBA were able to leverage that new popularity to

Yet, having attained its greatest financial and cultural success so far, the WNBA is facing the prospect of the first labor lockout in its 29-year history. The league’s collective bargaining agreement was set to expire on Oct. 31, but the two sides agreed to a 30-day extension with a new deadline of Nov. 30. As part of the agreement, either side can terminate the extension after a two-day notice period.

The biggest point of contention is how much of the WNBA’s windfall should be shared with players. The players union is hoping to lock down between 30% and 40% of all revenue coming to the league, which includes proceeds of the $200 million a year media deal, and to the teams, including merchandise, ticket sales and concessions, among other income streams, according to people familiar with the talks.

For some team owners, sharing more revenue could bite. Those who have been in control of their franchises the longest have experienced lean years that saw other teams fold — and are eager to recoup their losses. Meanwhile, newcomers such as Mark Davis, who bought the Las Vegas Aces in 2021, have indicated that they’re more open to greater revenue sharing.

“I haven’t been consulted, but I think you know what side of the table I’d probably be sitting on,” Davis said

Engelbert also risks alienating the league’s fanbase. Many WNBA fans, like Betsy Carswell, 62, who has been a Washington Mystics season-ticket holder since the club’s first game in 1998, have been along for the ride as the league’s popularity slowly increased. “I’ve lived through the years where me saying I was a WNBA fan or a Mystics fan was a punchline,” she said.

When the team launched, Carswell was among the first to lock down season tickets, buying two lower-bowl, half-court seats for no more than $500 each. Today, Carswell pays about $2,700 a season for both seats. She said many WNBA fans had soured on Engelbert.

“It says a lot that at the end of the championship she got up to get that trophy and was booed not by the players but by the fans,” Carswell said.

The exact mix of team and league revenue that would be shared with players in a new labor pact is still being negotiated, according to the people familiar with the talks, who spoke on condition of anonymity to describe private discussions. Under the National Basketball Association’s collective bargaining agreement, male players receive about 50% of all basketball-related income, including media rights, ticket sales and merchandise.

For its part, the WNBA has proposed tripling player salaries while keeping in place an arrangement that opens up revenue sharing if certain growth targets are reached, according to the people. To date, those benchmarks have never been hit.

Engelbert declined to be interviewed for this story, but she “strongly agrees with the players that they deserve to be paid more and is fully committed to negotiating in good faith and finalizing a new collective bargaining agreement that rewards the players’ significant contributions to the league’s continued success,” a WNBA spokesperson said in a statement.

A spokesman for the players union declined to comment on the talks.

In recent weeks, there have been clear signs that relations between Engelbert and the players are at a low ebb. At a news conference in September, Minnesota Lynx forward Napheesa Collier, a member of the players union’s executive committee, blasted the commissioner and the league.

“We have the best players in the world, the best fans in the world, but right now we have the worst leadership in the world,” Collier said. Days later, Collier called off a meeting with Engelbert. Collier didn’t respond to requests for comment for this article.

In 2015, Engelbert became the first female chief executive at Deloitte — and the first woman to lead one of the Big Four consulting firms. When her four-year term was due to end, the WNBA came calling. For a league hungry for business savvy, the seasoned executive looked like a perfect candidate.

Engelbert faced a tough task. With the league losing money, TV viewership was waning; the 2018 WNBA Finals averaged 481,000 viewers, a 14% decrease from 2017. In 2019, only 381,000 tuned in to the Finals, a 20% plunge.

In spite of those numbers, the WNBA and its players agreed to a new labor deal in 2020 that nearly doubled maximum player salaries from $117,500 to $215,000. The deal guaranteed season-long housing with additional bedrooms for players with children, as well as paid maternity leave.

Then, less than a year into Engelbert’s tenure, the pandemic turned sports inside out. Engelbert made sure a full season could be played by securing the “Wubble” facility at IMG Academy in Florida. She also wooed more corporate sponsors, winning praise from players, union leaders and others.

By the end of the WNBA’s 2020 fiscal year, the league had still

“Cathy was viewed as an innovator, her background in savvy business coming from Deloitte seemed to deserve credit for getting us to and through such a pivotal moment and keeping the season alive,” Monica McNutt, a basketball analyst at ESPN, said in an interview.

By 2021, the WNBA’s fortunes were improving, with its most-watched regular season since 2008. Merchandise sales

“Make no mistake, she has been an incredible business builder for this league,” said one owner. “In every category, player salaries, media, sponsorship and more, we’ve grown, she’s led that.”

The players union saw the $2.2 billion media deal as a missed opportunity to build more cohesion between the league and the players. Terri Jackson, the union’s executive director, said in an interview earlier this year that Engelbert hadn’t included her or the players in the deal talks with broadcasters. Jackson has repeatedly raised concerns about the undervaluation of the WNBA in the media rights deal.

“When you have the professional athlete there relaying the experience and the expectations, you get another insight,” Jackson said, adding that Engelbert said she was open to the idea for the next round of talks with the league’s media partners.

A person familiar with the matter said Engelbert hasn’t followed through with an invitation for players to participate in media deal talks.

Terri Jackson speaks during the Bloomberg Power Players New York event on Sept. 4. Photographer: Victor J. Blue/Bloomberg

In September of last year, Engelbert’s relationship with the players deteriorated in the wake of comments she made about the rivalry between Caitlin Clark of the Indiana Fever and Angel Reese of the Chicago Sky. Both women had become the targets of racist and sexist commentary, especially online.

“It’s a little of that [Larry] Bird and Magic [Johnson] moment, when those two rookies came in from a big college rivalry, one white, one black, and so we have that moment with these two,” Engelbert said. “The one thing I know about sports is you need rivalry, that’s what makes people watch. They don’t want everybody being nice to one another.”

In the ensuing hours, the NBA brought in its crisis communications team to decide how to proceed, according to people familiar with the handling of the situation. Engelbert was encouraged to book an interview with ESPN, the league’s biggest media partner, to rebuke the racism and sexism her players were confronting.

Engelbert was resistant to that idea, insisting she’d handle the situation her way, according to the people. The next evening, Engelbert clarified her remarks, saying in a

Ahead of the 2025 WNBA Draft, Engelbert said the league formed a task force to monitor hateful comments toward players.

After the union opted out of the previous labor deal in October 2024, the two sides began negotiating that December, and met many times in the following months. The players hired a raft of high-profile advisers, including Nobel-Prize winning Harvard economist Claudia Goldin. Engelbert acknowledged the union sent a proposal at the WNBA Draft in April.

At the same time, Engelbert was closing deals. On June 30, the league said that it would add three expansion teams by 2030 in Detroit, Philadelphia and Cleveland. The expansion fee for each franchise was a record $250 million, a 400% increase from two years earlier.

In June, on the eve of the league’s All-Star Weekend, the league offered its first counterproposal, and the two sides met for talks on July 17. At a news conference the next day, Engelbert described the conversations as “constructive” and said she was optimistic that a “transformational” deal would get done.

But the night before, players, who had been seething over what they saw as a paltry counterproposal from the league had been plotting a public demonstration of their anger. Thirty minutes after Engelbert was done speaking, players unzipped their warmup jackets and revealed shirts that read “pay us what you owe us.”

When Collier was presented with the MVP trophy at the end of the game, fans chanted, “pay them.”

A fan holds a sign saying “Pay the players” during the 2025 WNBA All-Star Game. Photographer: Steph Chambers/Getty Images

Engelbert had started planning to step down from the commissioner’s role as early as January 2024 and began telling team presidents and league executives that “she had more days behind her than she did in front,” according to a person familiar with Engelbert’s planning and communications with other officials. Engelbert has denied reports that she plans to leave the commissioner’s job.

Some WNBA players have wondered how much power Engelbert has and have pushed for NBA Commissioner Adam Silver to get involved in the labor talks. On a union Zoom call in October, Collier said, “we should just go to Adam,” according to people who were on the call who declined to be named.

Silver has indicated some skepticism toward comparing how men and women in the two basketball leagues are paid. On the Today show on Oct. 21, when asked if players should be receiving a bigger piece of revenue, he said “yes,” adding, “I think share isn’t the right way to look at it, because there’s so much more revenue in the NBA. I think you should look at absolute numbers in terms of what they are making.”

Silver has been at the NBA since before the WNBA launched and has navigated multiple collective bargaining negotiations. Engelbert said at a news conference following this year’s WNBA Finals that Silver has been “very supportive of how we’re thinking about the substantial increase in player salaries and benefits.”

Still, Silver has signaled his own wariness about the topic, noting that the tenor of the talks between Engelbert and Collier had gone off-piste.

“It’s become too personal,” he said at an NBC Sports event on Oct. 6. “We’re going to have to work through those issues.”

UK Has a New Prime Minister Without a General Election

Adaptive Governance in Volatile Markets

Navigating Sovereign Data Residency Mandates in the Age of AI

Armanino adds Strategic Accounting Outsourced Solutions

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

Tax Strategy: Employee Retention Credit update

-

Economics4 days ago

Economics4 days agoGlobal Trade Realignment and Supply Chains in 2026

-

Economics5 days ago

Economics5 days agoThe Warsh Shift: How the New Fed Chair Is Balancing War Drags and Tech Winds

-

Economics4 days ago

Economics4 days agoLabor Market Calibration: Analyzing the Shift Toward Skill-Based Allocation in 2026

-

Finance6 days ago

Finance6 days agoSouth Korea Raises Interest Rates to 2.75% for the First Time in More Than Three Years

-

Leaders6 days ago

Leaders6 days agoBerkshire Hathaway Chairman Reshapes His Long-Term Philanthropic Strategy

-

Finance4 days ago

Finance4 days agoTokenized Real-World Assets: Institutional Ledger Adoption Achieves Scale in July 2026

-

Economics6 days ago

Economics6 days agoGlobal Stock Market Weekly Recap: Tech Sell-Off Sparks International Rout

-

Accounting4 days ago

Accounting4 days agoStandardizing Global ESG Reporting: Key Compliance Imperatives for Mid-Year 2026