Listen to this story.Enjoy more audio and podcasts on iOS or Android.

Your browser does not support the <audio> element.

Kaleigh Long believed there had to be an American fix. As an Oklahoman working on political campaigns in the Democratic Republic of Congo she saw all too closely the bloodiness of the critical-mineral trade. Militias killed her flatmate’s siblings, burnt homes on resource-rich land and forced children to dig in the mines—as Chinese companies tolerated the abuses.

Back home the 28-year-old single mother reckoned that getting into the mineral business was the best way to clean up the supply chain and ease China’s chokehold on cobalt and other minerals vital to a greener economy. America had no nickel-cobalt refineries of its own. In early 2022 Ms Long set out to build its first. She raised $50m for her startup, Westwin Elements, and recruited oil-and-gas tycoons, a former intelligence officer and the longtime boss of Boeing, an aerospace company, to sit on her board. In her Oklahoma City headquarters the self-described libertarian touched her necklace, the pendant a silhouette of Africa, as she spoke about the $185m grant Westwin next hopes to win from the Department of Energy.

Westwin’s ambitions show the promise of the largesse doled out by the Inflation Reduction Act (IRA), Joe Biden’s signature bill to catalyse America’s clean-energy transition. Subsidies for electric cars attracted $110bn in investments in green manufacturing and battery-making within a year of the IRA’s passage in 2022. But as firms boosted production it became clear that China’s grip on the world’s mineral mines and refineries could prove perilous for its political foes. If China decides not to export refined metals tomorrow, as it has threatened to do, dozens of brand-new American gigafactories could soon sit idle.

Even with subsidies, mining and refining in America are not for the faint of heart. Regulations can make both activities uncompetitive. But the maths flipped in refiners’ favour in December 2023 when the tax agencies charged with implementing the IRA made it more protectionist. Their new rules clarified that companies selling electric cars made with materials processed by firms with at least 25% Chinese ownership are ineligible for subsidies. For makers of batteries and cars this was bad news—their inputs got pricier overnight. But for Ms Long it meant that her higher-cost product would have a market.

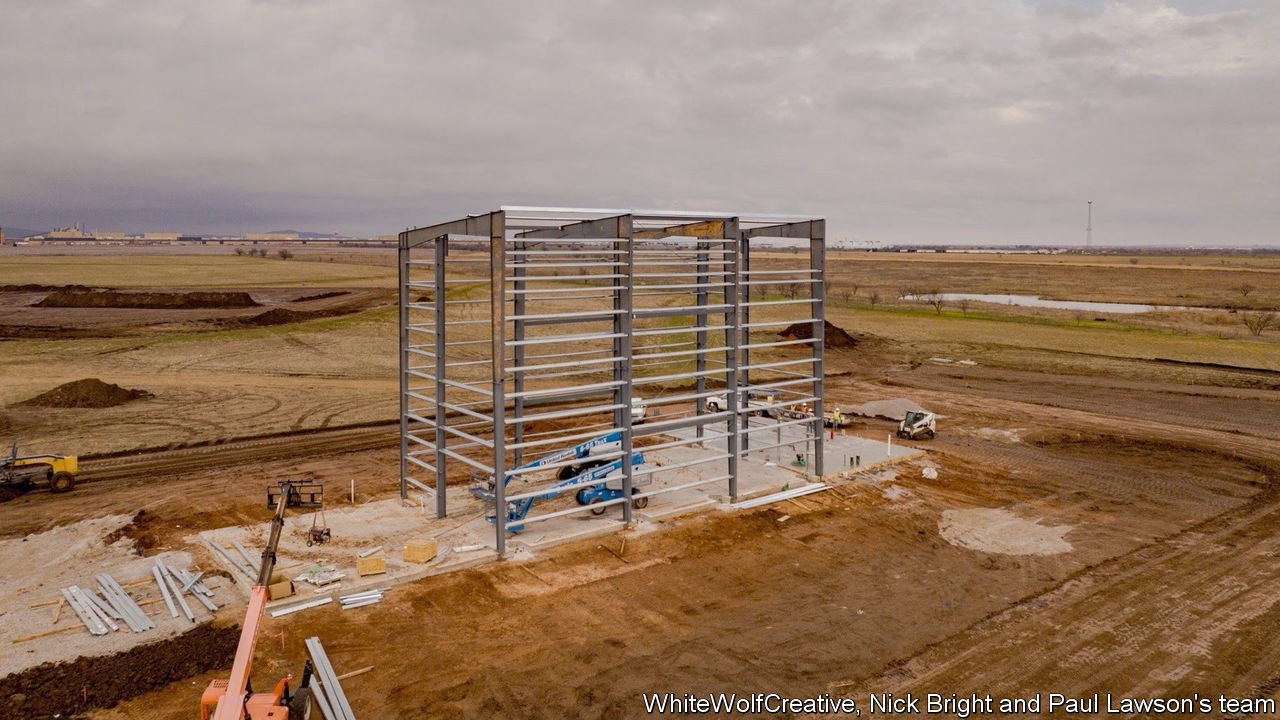

Drive 90 miles south-west of Oklahoma City through fields of cotton and cattle and you will find yourself at the construction site of Westwin’s pilot plant in Lawton. A steel skeleton of the refinery sits on a 40-acre plot framing the Wichita mountain-range; on a February morning engineers buzzed around it in hard hats. By 2030 Westwin plans to produce 64,000 metric tonnes of processed nickel and—if it can find ethical suppliers and sell the refined product without crashing the price—20,000 tonnes of cobalt. According to calculations by Daniel Quiggin of Chatham House, a British think-tank, that would meet roughly half of America’s demand for electric-car batteries. For building the supply chain “projects like this are indispensable,” says Bentley Allan, a professor at Johns Hopkins University.

Blood, sweat and fears

But in leaving Congo for America’s prairies Ms Long finds herself still haunted by ethical problems. By building in Oklahoma she inserted her project in the middle of a bitter row over indigenous rights. Leaders of the Apache, Comanche and Kiowa nations say the plant comes too close to their sovereign land and that the firm’s failure to consult them before building shows the same disrespect as settlers past. They fear that contamination from the refinery will give their babies cancer and dirty their sacred land and air. Having lost countless kin to covid-19 they refuse to back it without a guarantee that it will not make their people sick. Westwin cannot make that promise.

The protests echo those mounted against the Keystone XL oil pipeline in the Dakotas. At a sweat ceremony on a recent winter evening, between prayers for locked-up loved ones and addicted brothers, native residents pleaded for Westwin to stop construction. As an elder poured water on embers the hut filled with steam and became so hot your correspondent struggled to breathe. In darkness they sang and passed a tobacco pipe between them, the smoke a vehicle to lift their anti-industrial supplications “to the spirits”.

The next day the tribal chairmen met with Westwin executives. Lawton locals who attended had no patience for Ms Long’s tearful tale of child-slaves in the Congolese cobalt mines—indigenous people, she noted, just on a different continent—and no interest in what her project means for American national security.

Because they lack the muscle of richer tribes to the east who lobby more, their objections are probably for naught. But the distress of it all may in the end convince Ms Long not to build the commercial plant in her home state, especially if Texas or Louisiana offer better tax breaks.

The permitting process could be long and litigious in any of those places and the delay may undermine climate goals. As long as domestic refineries are not yet up and running and China’s mineral stash is still on offer, the IRA’s protectionist rules could slow progress towards decarbonisation, says Tom Moerenhout of Columbia University who advises the State Department and White House on energy policy.

Since hawkishness towards China is trendy in both parties, and most of the investments have gone to Republican districts, it is a fair bet that any future president will keep the subsidies in place. That comforts Ms Long, who says she worries about the risks facing her business “almost every day, most of the day”. Though many are cheering her on, Westwin has already shown just how hard it is to bring critical-mineral refining to America, never mind an ethical model for the world. ■

Stay on top of American politics with The US in brief, our daily newsletter with fast analysis of the most important electoral stories, and Checks and Balance, a weekly note from our Lexington columnist that examines the state of American democracy and the issues that matter to voters.

National Economic Council Director Kevin Hassett speaks to reporters at the White House in Washington, D.C., U.S., April 14, 2025.

Kevin Lamarque | Reuters

A top economic advisor to President Donald Trump expressed confidence Thursday that court rulings throwing out aggressive tariffs will be overturned on appeal.

Kevin Hassett, director of the National Economic Council, said in an interview that he fully believes the administration’s efforts to use tariffs to ensure fair trade are perfectly legal and will resume soon.

“We’re right that America has been mishandled by other governments,” Hassett said during a Fox Business interview. “This trade negotiation season has been really, really effective for the American people.”

The comments follow a ruling from judges on the Court of International Trade who said Trump exceeded his authority on tariffs, which are aimed both at combating barriers against American goods abroad and stemming the flow of fentanyl across the U.S. border.

While the Centers for Disease Control and Prevention has said that fentanyl is the primary driver in domestic overdose deaths, the judges ruled that related tariffs “fail because they do not deal with the threats set forth in those orders.”

Hassett bristled at the ruling and said the administration will continue its anti-fentanyl efforts.

“These activist judges are trying to slow down something right in the middle of really important negotiations,” he said. “The idea that the fentanyl crisis in America is not an emergency is so appalling to me that I am sure that when we appeal, this decision will be overturned.”

The administration has multiple options to get around the judges’ ruling, including other sections of trade laws it can utilize. However, Hassett said that’s not the plan at the moment.

“The fact is that there are measures that we can take with different numbers that we can start right now. There are different approaches that would take a couple of months to put these in place,” he said. “We’re not planning to pursue those right now, because we’re very very confident that this ruling is incorrect.”

IN APRIL Todd Lyons, the acting director of Immigration and Customs Enforcement (ICE), lamented that it takes too long to deport illegal immigrants. At the Border Security Expo in Phoenix he told a crowd of startup bosses vying for government contracts that a better deportation system would function more like Amazon, the tech giant whose delivery drivers zigzag the country at record speed. “Like Prime, but with human beings,” he said.

Accounting1 week ago

Accounting1 week ago

Economics1 week ago

Economics1 week ago

Personal Finance1 week ago

Personal Finance1 week ago

Accounting1 week ago

Accounting1 week ago

Finance7 days ago

Finance7 days ago

Economics1 week ago

Economics1 week ago

Economics1 week ago

Economics1 week ago

Economics1 week ago

Economics1 week ago