Accounting

Transform accounting’s busy season into an organizational asset

For many accounting and finance teams, the fiscal year-end brings a cycle of intense workloads that can extend into the new year, as accountants and auditors work to close the books, address complex accounting issues, and manage escalating audit demands. This grueling “busy season” can also limit accountants’ ability to provide strategic insights to their organizations.

Rising stakeholder expectations and a growing talent crisis due to seasonal burnout underscores the need for a shift in year-end audit preparations. By embracing forward-thinking practices, CFOs and accounting leaders can alleviate the pressure on their teams and turn busy season into an opportunity for innovation and value creation.

Reframing the year-end “inevitable”

Most companies wait until the fiscal year-end to tackle the more nuanced accounting issues, such as impairment analyses and revenue recognition adjustments, which adds stress to accountants’ already limited resources. Valuations, impairment analyses and documentation for M&A transactions are often squeezed into year-end, resulting in bottlenecks as companies compete for the same specialist resources. This surging demand, coupled with resource constraints at providers, drives up costs as specialists become increasingly scarce during this time period.

The pressure of these time-sensitive requirements is a major contributor to the shortage of accounting professionals. These various pressures also frequently cause a company’s accounting and finance function to be overburdened for the first couple months of the year and unable to shift their focus to strategic annual planning until the first quarter is nearly over. To prevent this reactive cycle, the time to shift to more strategic audit preparation is now.

A successful audit cycle starts with sound project management. Companies should assign a dedicated in-house point person or qualified advisor to oversee the audit process. This person should prioritize the prepared-by-client list from the auditors and critical items such as impairments, recording M&A transactions, going concern analyses and other complex accounting in relation to restructuring debt and equity financing arrangements. Taking a proactive, methodical approach to the audit cycle will help streamline the process during busy season.

Embracing AI and automation for a strategic shift

Implementing new tools and technologies can elevate the abilities of the accounting and finance team during and beyond busy season. Other professions have managed to modernize and streamline their workflows, but the office of the CFO has often been more hesitant to adopt technologies that could alleviate the demands of busy season. The rise of automated and AI-enabled technologies presents new opportunities to streamline the audit cycle. Process improvements and AI-powered tools can potentially manage intensive data-crunching tasks and free up accountants’ time to focus on interpreting results, responding to auditor’s priorities, and building more strategic relationships with their stakeholders.

For example, AI has the potential to identify data anomalies in financial performance before they arise, reducing the last-minute rush and helping accounting teams manage their workflow more effectively. Automation can help ensure audit-related tasks are completed earlier, allowing teams to bring greater focus to more complex issues with greater strategic importance. AI can revolutionize the accounting profession and reduce pressures during busy season by enhancing efficiency and risk mitigation through its automation and real-time insights.

As AI becomes increasingly integral to audit and accounting, however, professionals must navigate and proactively manage the related risks. To mitigate these risks, accounting teams should integrate AI tools thoughtfully, ensuring both human oversight and robust governance. Companies must implement strict policies for AI development, testing and changes, focusing on the financial reporting impacts. Continuous monitoring, audit trails and segregation of duties are crucial to maintaining transparency and preventing errors. For example, AI systems that automate journal entries should have controls in place to verify the accuracy of the entries and detect any anomalies.

Reclaiming value: the accountant as strategic advisor

In the current cyclical model, many accountants spend the first quarter of the new year working solely on the previous year, limiting their ability to provide their organizations with meaningful strategic insights. Alleviating pressure during busy season can allow accountants to play a larger role in providing forward-looking insights that help guide business strategy. This shift would not only elevate the responsibility of the profession but also help address some of the burnout issues that have exacerbated the current talent gap.

Moving away from reactive year-end cycles is essential for the long-term growth of the accounting profession. Embracing automation, ensuring continuous audit readiness, and positioning accountants as strategic advisors can help move busy season from a yearly hurdle to a time for growth and impact. By planning ahead and leveraging new technologies, leaders can strengthen their organization’s future by bringing efficiency and strategic insight to the year-end audit process.

As CPA firms grow into the $10 million to $100 million revenue range, operational complexity increases, especially during peak periods like tax season. Leadership must prioritize strategies to reduce friction, improve efficiency, and enhance the client and staff experience. Algorithms, defined as systematic processes designed to solve specific problems, are a key enabler in achieving these goals.

By automating repetitive tasks, algorithms can save hundreds of hours during the busiest times, allowing staff to focus on high-value activities and improving client satisfaction.

Four specific examples of areas where algorithms can help firms are described below, but no matter the area, adopting algorithms requires deliberate planning and execution:

1. Identify opportunities

- Assess pain points in tax, audit, scheduling, and advisory workflows.

- Identify routine tasks that consume excessive time during peak periods.

2. Gather and analyze data

- Evaluate the availability of client and internal data to support automation.

- Determine additional data needs and acquisition strategies.

3. Experiment and iterate:

- Pilot small-scale solutions, such as automating a single tax form process or scheduling tool.

- Refine based on results and user feedback.

4. Scale and integrate:

- Implement successful pilots across teams or departments.

- Provide staff training to maximize adoption and effectiveness.

5. Measure and optimize:

- Use key performance indicators such as time savings, error reduction, and client satisfaction to assess the impact.

Quick wins for immediate impact

To build momentum, start with high-impact initiatives:

- Tax workflow automation: Automate the completion, e-signature, and filing of forms like 8879 and 4868, and notify clients of estimated tax payments due via an automated communication system.

- Audit data preparation: Use algorithms to download client data, generate trial balances, and perform risk analysis.

- Scheduling optimization: Implement an algorithm-driven scheduling tool to automate meeting coordination, resource allocation, and deadline tracking.

Conclusion

Algorithms are transformative tools that empower CPA firms to operate more efficiently while delivering enhanced value. By automating routine tasks in tax, audit, scheduling, and advisory services, firms can save significant time, improve accuracy, and foster stronger client relationships. The key to success lies in adopting a strategic roadmap — identifying opportunities, running experiments, and scaling solutions. Mindset is paramount.

For CPA firms navigating the challenges of growth and complexity, algorithms represent a critical investment in operational excellence, enabling staff to focus on what truly matters: delivering exceptional client experiences. Think — plan — grow!

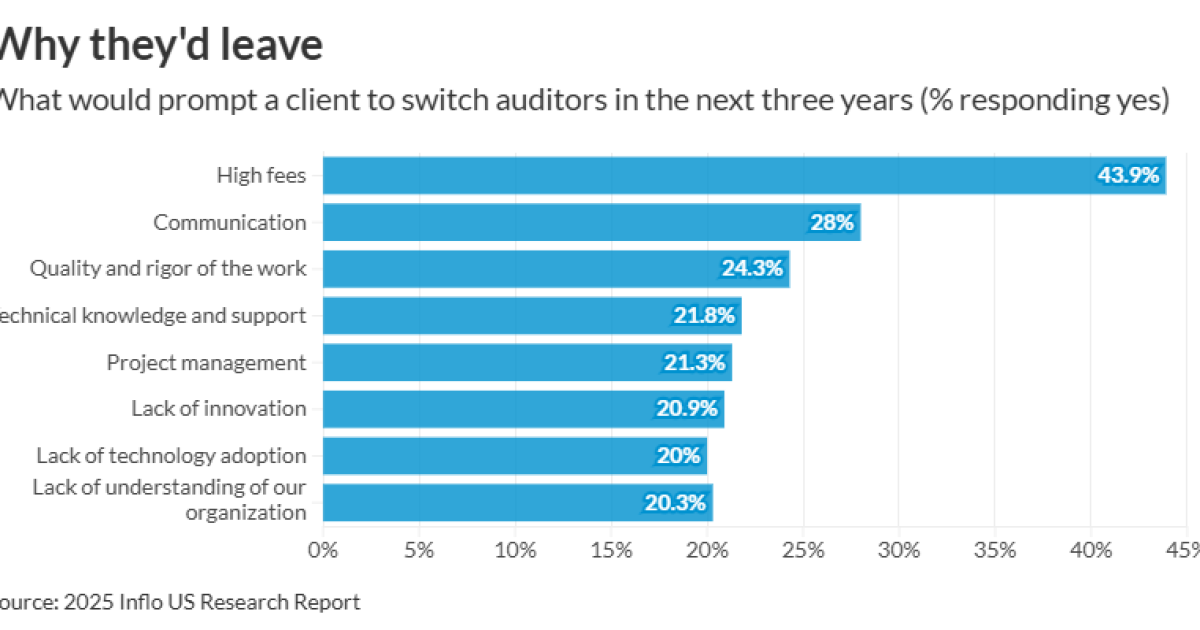

More than two-thirds (70%) of U.S. audit clients are ready to change firms within the next three years, according to a new report.

Inflo’s “Creating a New Audit Experience for U.S. Businesses”

Clients with the most employees (250 employees or more) were the highest to report it was “very likely” they would switch firms. Meanwhile, clients with fewer employees (less than 50 employees) were the highest to report it was “very unlikely” they’d switch firms.

By far the most common reason causing a client to look for a new firm was high fees (44%). When asked how much more clients would be willing to pay for an audit that “gave you more value,” respondents answered 5-10% more (33%), 11-20% (31%) and 21-30% (14%). Five percent of respondents answered “nothing.”

Subsequently, clients said the leading factors influencing their decision to accept or resist fee increases were perceived value and quality of service (42%), relationship with the audit firm (40%), meeting deadlines (39%), level of justifications and transparency regarding an increasing (35%), responsive communication (35%) and the frequency of previous fee increases (34%).

(Read more:

The second most common reason causing a client to switch auditors was communication (28%), followed by quality and rigor of the work (24%), technical knowledge and support (22%), project management (21%), lack of innovation (21%) and lack of technology adoption (20%). Sixteen percent of respondents reported, “We are not experiencing any issues.”

“This research makes one thing clear: U.S. businesses are demanding a better audit experience,” Inflo CEO Mark Edmondson said in a statement. “From high fees based on outdated pricing models to technology that hasn’t changed since the 1990s, the approach of many audit firms is driving business away.”

Additionally, nearly half of respondents (45%) said they’d like auditors to improve on the use of technology to add more value to their audits, followed by the time needed from their team and insights on their organization (38% each).

“The good news is that clients care about their audits. They want them to play a key role in driving operational improvement and consistent business growth,” Edmondson said. “Audit firms that act on the report’s findings will be rewarded with rising fee incomes and a continually growing client base.”

Walmart taps own fintech firm for credit cards after Capital One exit

Remaking the partnership model for young accountants

Boomer’s Blueprint: 4 ways algorithms can improve your accounting firm

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Blog Post1 week ago

Blog Post1 week agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Economics1 week ago

Economics1 week agoWhy the president must not be lexicographer-in-chief

-

Finance1 week ago

Finance1 week agoThis is why Jamie Dimon is so gloomy on the economy

-

Accounting1 week ago

Accounting1 week agoSteinhoff fraud trial moved to South Africa’s high court

-

Personal Finance7 days ago

Personal Finance7 days agoWhat the national debt, deficit mean for your money

-

Personal Finance1 week ago

Personal Finance1 week agoHow to save on summer travel in 2025

-

Personal Finance1 week ago

Personal Finance1 week agoDenmark raises retirement age to 70; U.S. might follow

-

Finance1 week ago

Finance1 week agoWhy JPMorgan hired NOAA’s Sarah Kapnick as chief climate scientist