Accounting

US extends 25% chip tax credit to wafers, including solar

The Biden administration finalized rules for a 25% tax credit for semiconductor manufacturing projects, expanding eligibility for what is likely to be the largest incentive program from the 2022 Chips and Science Act.

The new

The credits also will apply to solar wafers — an unexpected shift that could help spur domestic production of panel components. So far, the U.S. has struggled to foster manufacturing of those parts, despite a surge of investment in U.S. panel-making factories.

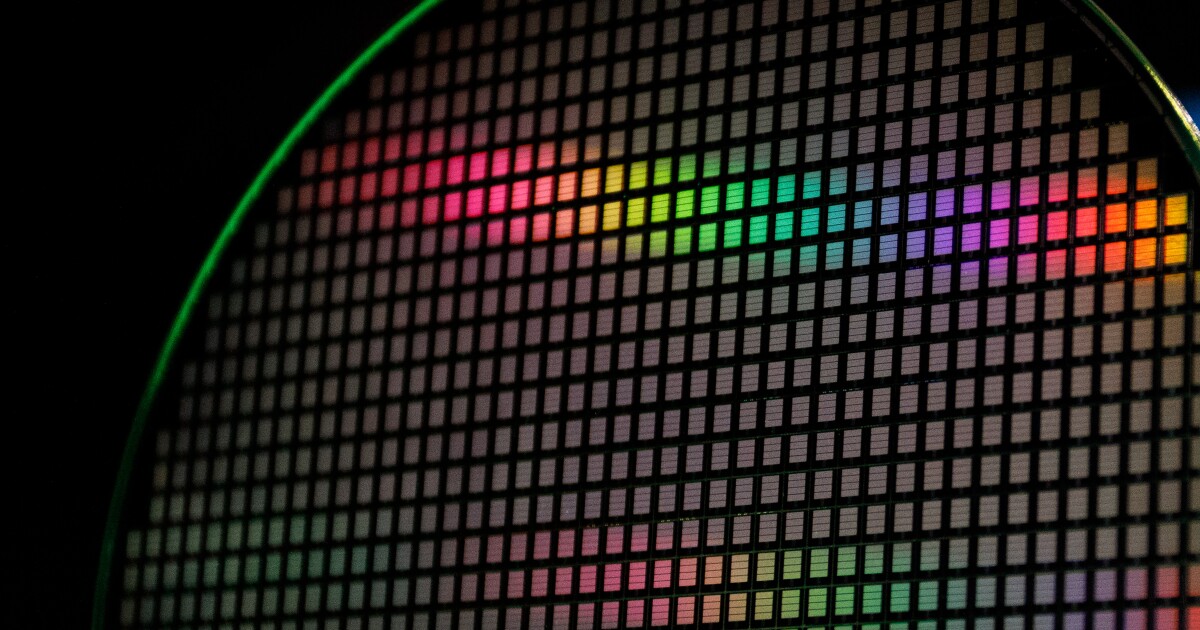

Samsul Said/Bloomberg

But the benefits don’t extend all the way up the supply chain. Still excluded are facilities that produce underlying materials like polysilicon, which is used to make wafers. That approach is consistent with how the original law was written, as well as how the Commerce Department defines semiconductors and equipment as opposed to materials, a Treasury official said.

The tax refunds are one of three main subsidy streams available from the Chips Act, which aims to revitalize the American semiconductor industry after decades of production shifting abroad. The law also set aside $39 billion in grant funding — more than 90% of which has been allocated, though not yet spent — and $75 billion in loans and loan guarantees, of which officials are likely to use less than half.

The latter two incentive categories have garnered the most attention — President Joe Biden has even visited factories to herald the announcements — but it’s the tax credits that could be most meaningful for companies. Proposed grants typically cover 10% to 15% of project costs, compared with 25% for tax credits. The idea is to make it just as cost-effective to build a factory in the U.S. as in Asia.

“Our goal is to give you the minimum amount of money necessary to get you to expand on our shores in a way that advances our economic and national security objectives,” Mike Schmidt, director of the Commerce Department’s chips office, said in an August interview when asked about tax credits. “That means looking at all sources of funding and then figuring out how our funds get you over that hump.”

Some companies argued in negotiations that the tax credits shouldn’t “count against” their other funding, Schmidt said — a line of reasoning that didn’t sway government officials.

Chip companies have announced more than $400 billion in planned U.S. investment over the past several years, including massive factories from leading-edge manufacturers like Taiwan Semiconductor Manufacturing Co. and Intel Corp. There also are efforts underway to make older-generation processors and other supplies.

The surge in activity likely means that the Chips Act will be more expensive than anticipated.

The Congressional Budget Office originally

That would exceed the original projected cost of the entire Chips Act, the report said, “resulting in a total cost overrun of nearly 80%.”

Asked whether the Treasury Department has its own cost estimate for the tax credit, an official didn’t provide a specific number. But any overrun could be seen as a win by the Biden administration since it represents additional investments in American manufacturing.

In almost every case, tax credits will account for the greatest share of Chips Act incentives going to any one company. Micron Technology Inc., for example, expects to get around

Texas Instruments Inc. anticipates $6 billion to $8 billion in tax credits — as much as five times the size of its Chips Act

Now that tax season is over, it’s time to refocus on identifying and implementing business strategies that drive your firm’s growth and keep you ahead of the curve in an ever-changing economic environment.

The market is shifting fast, and accounting firms that spot these changes early will come out ahead. According to Intuit QuickBooks’

Here are three small business trends for your accounting firm to keep in mind this year:

1. Accountants may be scarce, but new small businesses continue to increase

It’s no secret that the accounting profession is facing a talent shortage as more experienced accountants retire or leave the industry and fewer young professionals enter the field. The requirements to become a CPA have deterred prospective candidates, leading to a

But at the same time, the number of small businesses is steadily growing, creating a major opportunity for your firm to expand its client base this year. The Entrepreneurship survey found that more than half (54%) of respondents plan to start a new business this year. That’s a wave of new entrepreneurs who will need the right financial guidance, tax planning and compliance support to ensure their first year in business is successful and represents the beginning of long-term success.

Accounting firms can position themselves to take advantage of this demand using technologies like AI to help close the gap. Additionally, for firms looking to grow, targeting the right clients is key. Whether through niche specialization, local networking, or strategic marketing — meeting business owners where they are can help firms build lasting relationships. Investing in outreach now can pay dividends in the form of long-term growth-potential clients and a stronger, more resilient practice.

2. Small businesses are prioritizing technology — and so should your firm

Small business owners are jumping on the tech bandwagon, and they’re not slowing down. From AI-powered bookkeeping to automated invoicing, they’re leaning on new tools to streamline operations, save time, and run their businesses more efficiently and effectively.

Why should your firm take note? Because business owners want more from their accountants than just tax returns and payroll. They’re looking for real-time financial insights, business advice and hands-on support to help them navigate evolving economic challenges like rising costs and higher interest rates.

That’s where technology and human expertise come together. On average, firms planned to invest

3. Errors are common for entrepreneurs who manage their own business taxes

Financial management is not always a small business owner’s expertise. While entrepreneurs need some level of financial literacy to run and grow their businesses, most are learning as they go. One of the biggest areas of concern? Taxes. In fact, 34% of business owners say they’ve made an error when filing business taxes in the past. This includes overpaying or underpaying taxes, filing at the wrong time, or using the wrong forms.

Across the board, business owners cite understanding tax laws and regulations as the most challenging aspect of filing business taxes, followed by keeping track of necessary documentation and maximizing tax credits and incentives. For accountants, this represents a clear opportunity to provide guidance and strategic support, helping clients navigate complex financial requirements while positioning their firms as trusted advisors.

With entrepreneurship on the rise this year, accounting firms have an opportunity to play an important role in small business success. Whether it’s tax season or beyond, keeping these small business trends in mind will help your firm stay competitive and drive long-term growth for both your business and the clients you serve.

Grant Thornton names new CFO; CTCPA installs board of directors; and more news from across the profession.

3 small business trends to position your firm for growth

Trump admin seeks Education Department layoff ban lifted

Jobs report May 2025:

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

The Essential Practice of Bank and Credit Card Statement Reconciliation

Are American progressives making themselves sad?

-

Economics1 week ago

Economics1 week agoHow young voters helped to put Trump in the White House

-

Economics1 week ago

Economics1 week agoElon Musk says Trump’s spending bill undermines the work DOGE has been doing

-

Blog Post6 days ago

Blog Post6 days agoCommon Bookkeeping Challenges and Solutions for Small Businesses

-

Accounting1 week ago

Accounting1 week agoHighest paid jobs in corporate accounting

-

Personal Finance1 week ago

Personal Finance1 week agoHarvard, Trump international enrollment battle affects college applicants

-

Economics7 days ago

Economics7 days agoWhy the president must not be lexicographer-in-chief

-

Personal Finance1 week ago

Personal Finance1 week agoCrypto in 401(k) plans: Trump administration eases rules

-

Accounting1 week ago

Accounting1 week agoTrump to pardon stars of reality show ‘Chrisley Knows Best’