Economics

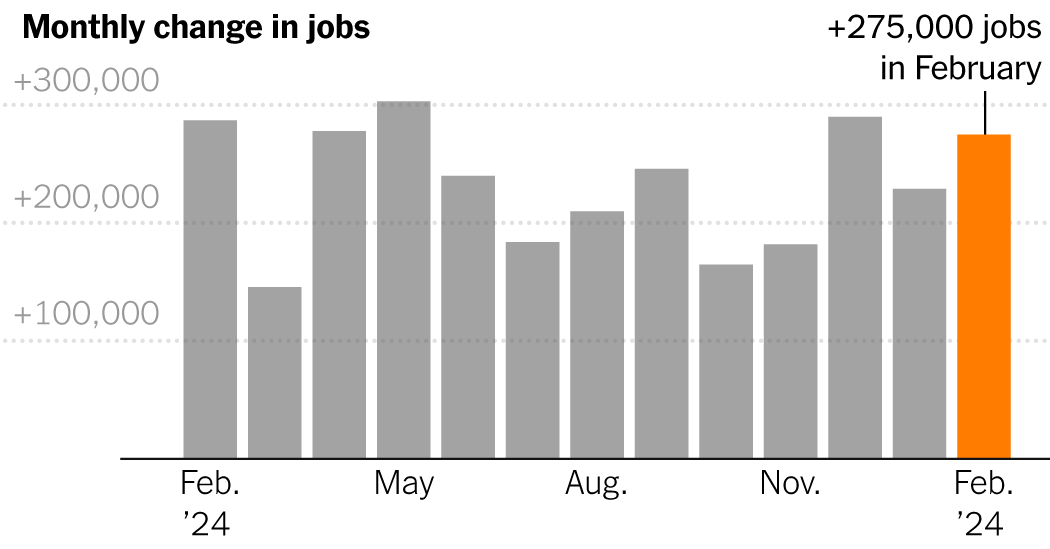

U.S. Employers Add 275,000 Jobs in Another Strong Month

Finance4 hours ago

Tariffs are my only concern, ‘Big Short’ investor Steve Eisman says

Personal Finance5 hours ago

Trump pauses Social Security benefit cuts over defaulted student loans

Accounting6 hours ago

Tax Strategy: Provisions of the House tax bill the Senate is most likely to scrutinize

Accounting1 year ago

New 2023 K-1 instructions stir the CAMT pot for partnerships and corporations

Blog Post7 months ago

The Essential Practice of Bank and Credit Card Statement Reconciliation

Economics1 year ago

Are American progressives making themselves sad?

-

Personal Finance1 week ago

Personal Finance1 week agoHow appealing property taxes can benefit new homeowners

-

Blog Post1 week ago

Blog Post1 week agoHow to Implement Internal Controls to Prevent Business Fraud

-

Economics6 days ago

Economics6 days agoElon Musk says Trump’s spending bill undermines the work DOGE has been doing

-

Economics1 week ago

Economics1 week agoMAGA: protecting the homeland from Canadian bookworms

-

Accounting6 days ago

Accounting6 days agoHighest paid jobs in corporate accounting

-

Personal Finance1 week ago

Personal Finance1 week agoHow to pay college tuition bills with your 529 plan

-

Economics6 days ago

Economics6 days agoHow young voters helped to put Trump in the White House

-

Personal Finance6 days ago

Personal Finance6 days agoHarvard, Trump international enrollment battle affects college applicants